The Sovereign Debt Explosion Issue

This was the most fascinating week I’ve seen in the sovereign debt market in decades. Sovereign debt is just a fancy name for government bonds. Are we looking at the beginning of a multi-country sovereign debt disaster? Plus, the Saudis extend an oil production cut, a government bailout still leads to bankruptcy, and an update on employment that Jerome Powell is watching. In this week’s 5 Things:

- US Treasuries downgraded for only the second time. Top rating gone.

- Bank of Japan capitulates again. Japanese government bonds plummeting.

- S&P 500 earnings beats are manufactured lies.

- Saudi message to the White House, “drop dead”.

- Yellow – A massive corporate bankruptcy. Is the media blaming the wrong people?

- Despite widespread economic issues, the employment situation remains strong.

DKI premium subscribers receive the full 5 Things on Monday morning and have already seen our analysis on both big sovereign debt problems. If you want to understand these market moving events better and stay updated on how to protect your portfolio from them, we welcome you to subscribe.

Astute readers will notice this week’s version of the “5 Things” goes to 6. Either we’re delivering 20% more value, or we can’t count. You decide. Very astute readers will notice we used the same line last week to which we respond, “thanks for reading every week”.

1) Fitch Downgrades US Debt:

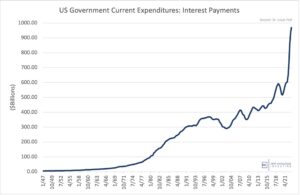

Fitch took down its rating on US debt from AAA to AA+. The last downgrade of US debt took place more than a decade ago. Fitch made some comments about the recent debt ceiling drama, but the real issue can be seen in the chart below:

Once higher rates work through the system, interest expense will be > $1T/year.

DKI Takeaway: Several government officials squawked in protest, but here are the facts: Debt will expand from $31T to $35T in under two years. Off-balance sheet liabilities are over $200T. Total liabilities are almost a quarter of a quadrillion dollars which is unpayable and a coming disaster. The government now has to print dollars to pay interest on the extra debt which is the definition of a Ponzi scheme. There will be a stealth default where the US will pay what’s owed in debased dollars which will have little value. Of course Fitch downgraded! If you need help protecting your portfolio from this, reach out at IR@DeepKnowledgeInvesting.com. We’re helping our subscribers deal with this issue now.

2) Japan is in Trouble:

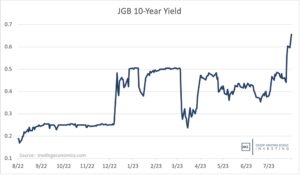

DKI has been following Japan because with massive debt, low growth, and too-low interest rates for too long, they are the model the US has been following. This week, the Bank of Japan capitulated and decided to allow the 10-year bond to trade above 50bp. Japan desperately needs higher bond yields to strengthen the yen which has fallen from 115 to the dollar last year down to 142 this year.

You can see where the BoJ capitulated in December and again last week.

DKI Takeaway: The Bank of Japan owns most of its own government debt and is often the only buyer in the market. This is a manipulated market. The BoJ was blowing through foreign exchange reserves to defend the yen which is not sustainable. As Japanese bond yields rise, that will pull money out of US Treasuries and stocks. If you want to understand this important issue better, we recommend our blog posts “Japanese Debt – We’re Taking a Victory Lap” (free) and “Japan is Looking for an Exit That Doesn’t Exist” (paywalled).

3) Are 2Q Earnings Beats Lies?:

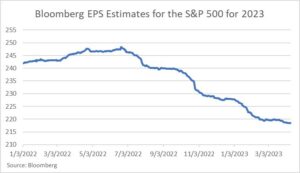

We keep seeing reports that the vast majority of S&P 500 companies are beating analyst estimates for the second quarter. Many of these companies aren’t seeing a rise in their stock prices. Let’s look at why:

This graph is a few months old. Current estimate is down to $215 – $218 depending on source.

DKI Takeaway: DKI warned a year ago when the ’23 number was almost $250 that estimates were too high and needed to be reduced. Sell-side analysts take guidance from the companies which like to lower the bar for themselves. The analysts want to maintain good relationships with the companies they cover to get investment banking business. As a result, they lower estimates, but keep their target prices slightly above the current price in order to maintain their “buy” rating. This encourages the companies to purchase investment banking services. The price target moves up and down with the stock price meaning the sell-side is more like a newspaper telling you what happened yesterday than doing the job of analysts who help you invest based on what happens next. This is not the way people with integrity conduct business.

4) White House Won’t Refill SPR – Saudis Cut Production:

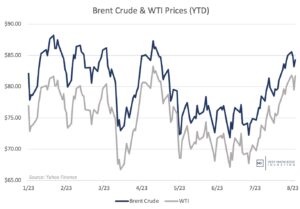

Last year, the White House released hundreds of millions of barrels of oil from the strategic petroleum reserve (SPR) in order to get gas prices down ahead of the midterm elections. Shortly afterwards, they announced they’d refill the SPR when oil prices reached $70 a barrel. When the White House declined to refill the SPR which was down to 40-year lows, Saudi Arabia announced a production cut of 1MM barrels a day. That production cut got extended from July into August. With the White House still refusing to refill the SPR, the Saudis extended the cut through September with Russia cutting exports by an additional 300k barrels a day.

The White House had its chance to declare victory and passed.

DKI Takeaway: All politicians take advantage of everything they can to stay in office, but we’d prefer that certain national security assets like the SPR be left out of the usual partisan gamesmanship. The US is now rolling into hurricane season with limited energy reserves, and any purchase delays can be more than matched by Saudi (and now Russian) production cuts. DKI is long-term bullish on energy had has specific tickers on the subscribers’ Current Recommendations page.

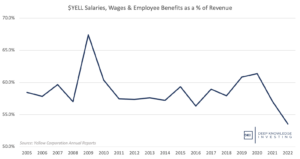

5) Yellow Bankruptcy – Are We Blaming the Right People?:

This week Yellow ($YELL), the huge shipping company, announced they’d declare bankruptcy. The narrative was that threats by the unions to strike caused companies to immediately shift to other shippers which then caused an immediate cash flow problem at $YELL. The instant abandonment by customers led to the bankruptcy announcement.

Definitely a strategic error by the union, but is it really all their fault?

DKI Takeaway: There’s no question that threatening to strike was a terrible strategic move by the union which led to the loss of tens of thousands of union jobs. However, it’s clear that union wages were not out of line by historical standards. Plus, the government provided $YELL with a $700MM bailout in 2020. DKI’s conclusion: Everyone is at fault. Our suggestion: Government should stop picking winners and losers. No more taxpayer-funded bailouts. Management should do a better job running the company. Unions should avoid threats that lead the entire company to fail and ensure everyone loses their jobs.

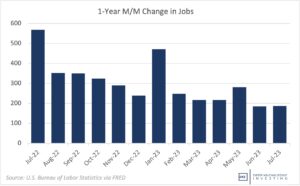

6) US Job Growth and Wages:

Friday’s employment report shows nonfarm growth of 187k jobs which was slightly below expectations of 200k. The unemployment rate fell to 3.5%. Wage growth was 4.4%.

Jerome Powell is definitely watching this.

DKI Takeaway: The employment market remains strong and growing. We’re a bit concerned about slowing job growth combined with a lower unemployment rate. When people exit the labor market and go on welfare, they’re considered out of the labor market which lowers the unemployment rate. 4.4% wage growth indicates that employers are still struggling to fill existing positions. We’ve been saying for months that Powell is more concerned about the employment market and services inflation than the CPI. More data like this increases the probability of more rate hikes by the Fed. You all know the line: “higher for longer”.

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.