The Surprisingly Weak Macro Issue

As we approach the tail-end of 2Q company earnings, the market turned back to focusing on more macro issues, and was immediately “rewarded” by lots of not-so-good news. In this week’s 5 Things, we’ll cover:

- CPI rose and Core CPI remains sticky. Will the index continue to rise?

- PPI wasn’t bad, but came in above expectations.

- Ratings agencies starting to downgrade banks.

- China exports down 14.5% (that’s huge!).

- FedEx reducing staffing even after the Yellow Corp bankruptcy.

- Are we in recession already? What should you look for to understand?

A fond farewell and a round of applause to DKI Intern, Tristan Navarino. This is Tristan’s last week at DKI as he returns to finish his degree in the excellent finance program at the College of Charleston. Great job, Tristan. DKI and our readers benefitted from your high-quality work all summer!

Astute readers will notice this week’s version of the “5 Things” goes to 6. Either we’re delivering 20% more value, or we can’t count. You decide. Very astute readers will notice we used the same line last week to which we respond, “thanks for reading every week”.

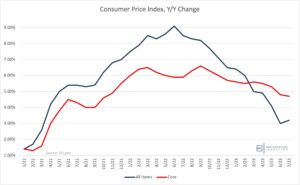

1) Consumer Price Index Rises?!:

The Consumer Price Index (CPI) rose from 3.0% last month to 3.2% which was slightly better than expectations of 3.3%. The Core CPI which excludes food and energy was up a stubborn 4.7% which was right in line with last month’s 4.8%.

Core is coming down but slowly.

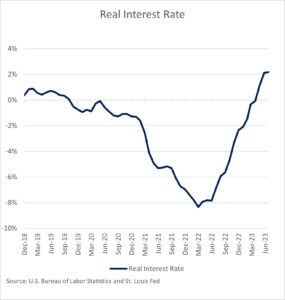

Real interest rates remain around 2%.

DKI Takeaway: The last few months, people have been excited about disinflation (a reduction in the rate of inflation). Here’s what’s coming: comparisons with a lower CPI base for the rest of the year, a massive one-time adjustment to health insurance expenses that’s been keeping the CPI low expires in two months, higher food prices, and reduced oil production from Saudi Arabia and Russia that may lead to higher energy prices. It’s going to be difficult to get the CPI down from here in the next few months.

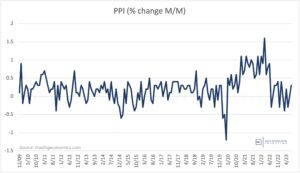

2) PPI – Bit of a Mixed Story Here:

The Producer Price Index (PPI) was up .8% for the last 12 months. While that’s a good number on an absolute basis, the monthly change was .3% which was the highest reading since last January. The PPI less food, energy, and trade was up .2% for the month and 2.7% for the last 12 months.

July was another up month.

DKI Takeaway: This one is a bit of a mix in terms of the conclusions we can draw. On the positive side, the annual numbers are definitely getting into a more comfortable range for the Fed. The negative is that the still-sticky services inflation number was up .5% for the month which annualizes into something well-above the Fed’s target. The other negative is the lower PPI may be indicating reduced demand for goods, something we’ll address later in this version of the 5 Things.

3) Moody’s Downgrades 10 Banks (as a Start):

This week, Moody’s downgraded 10 US banks. They focused on the small and medium sized firms rather than the too-big-to-fail institutions which are still operating under an implied government guarantee. Moody’s is looking at downgrading additional banks and citied the obvious and correct risks of deposit flight for higher-yielding Treasuries, and the likely deterioration in value of the bonds these banks are holding on their balance sheet.

The downgrades are reasonable. We wonder why it took so long.

DKI Takeaway: The situation may get worse for banks. In a webinar for DKI subscribers, Board Member, Mish Shedlock, opined that the US was already in a recession. Howard Freedland, another DKI Board Member, noted that a huge number of commercial property loans made in 2018 were going to reprice at unaffordable rates this year. He noted that this would likely cause pressure on the banks. This is the “credit event” that Michael Gayed has warned about for the last year. The video from the webinar will be made public on August 15th.

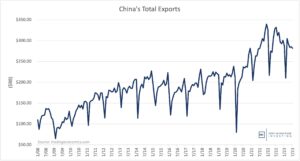

4) China Exports Down 14.5%!:

China’s economy is heavily dependent on exports, and those were down 14.5% in July. That’s a massive decline. It wasn’t just China either. South Korean exports were down 16.5%. The Wall Street Journal wrote that “the manufacturing sectors in five out of seven Asian countries, including China and Vietnam, were in contraction last month, pointing to weak underlying demand from the West.”

There’s definitely some seasonality here, but a 14% y/y decline is huge.

DKI Takeaway: One reason the US economy hasn’t fallen into recession has been enthusiastic consumer spending (supplemented by trillions of dollars of excess government spending). Double digit manufacturing contractions in the countries that export to the US may indicate a coming consumer slowdown. Also, while US companies are trying to reduce reliance on China, that wouldn’t explain the declines in places like South Korea and Vietnam.

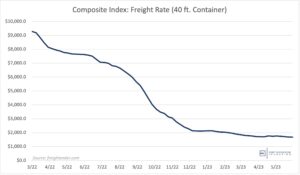

5) Weak Shipping News:

Yellow Corp ($YELL) declared bankruptcy last week when union threats to go on strike scared customers into using other carriers. (It’s clear that this situation was not 100% the fault of Teamsters’ leaders and that company management should bear their share of blame as well.) FedEx ($FDX) is still proceeding with furloughs and layoffs announced last year some of which take effect this month. And there’s a decline in container shipping rates.

Much of this decline is a normalization from Covid-related supply line issues, but it’s still big.

DKI Takeaway: The reason many investors pay attention to shipping companies is because they have a good sense of demand for goods all over the country. It’s true that the FedEx layoffs were announced months ago, that the Yellow bankruptcy is just pushing business to other carriers, and much of the shipping rate declines are related to post-Covid normalization. Still, seeing all of this in the same week makes me think there are concerns regarding demand for goods.

6) Are We in a Recession Already?:

The argument against recession and for “soft-landing” is based on a strong job market, positive GDP growth, and continued consumer spending. The thinking is the Fed may be able to reduce rates at just the right time and keep the economy growing (if slowly).

Gross Domestic Income indication contraction. Chart from MishTalk.

DKI Takeaway: The soft-landing arguments are all valid. On the other side of this one is gross domestic income shrinking even in a strong employment market, the possibility of a credit event impacting corporate income statements and in particular, commercial real estate borrowers and lenders, shrinking demand for bank loans, and the weak shipping and export news discussed in earlier “Things”. If a recession has already stated, this is what it would look like. For more information on this, check out the DKI blog post “Are We in a Recession Already”.

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.