Spirit Airlines filed for Chapter 7 leading X to try to assign political blame. Elizabeth Warren was wrong to brag about blocking the Jet Blue deal and crowing that it was a win for the Biden Administration, but was there something else going on as well? We provide a completely different view free from partisan bickering. Most of the big tech firms reported great quarters, but investors are finally focused on whether the hyperscalers can earn a return on massive and growing AI spending. DKI agrees with that approach. GameStop bids for eBay, a company 5x $GME’s size. The deal requires tens of billions of dollars of additional funding. DKI’s Interns ask some good questions about the motivations here. Regis Resources and Vault Minerals announce a $7.7B deal. It will create Australia’s third largest publicly traded gold mining company. The good news for our gold position is it doesn’t increase the production capacity of the industry. In this week’s educational topic, we discuss the benefits and risks of vertical integration. Don’t know what that is? No worries – we explain that as well.

This week, we’ll address the following topics:

- Did Elizabeth Warren and the Biden Administration kill Spirit Airlines? Was it President Trump and the cost of oil? Want to know the real culprit? Read on!

- Most of the Magnificent 7 reported great quarters, something necessary at multi-trillion-dollar valuations. The market now wants to see revenue attached to AI capital expenditure spending.

- GameStop makes an unfunded bid for eBay, a company 5x its size. DKI Interns have thoughtful questions about the motivation.

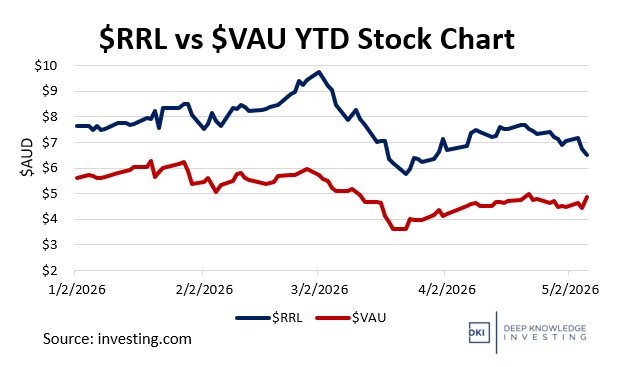

- Regis Resources and Vault Minerals announce $7.7B merger to create the third largest publicly traded gold mining company in Australia.

- What are the benefits and risks of vertical integration? We walk you through the subject in this week’s educational topic.

In their first week in charge, new Interns, Kunal Arora and Elijah Killorin, handled everything with ease. I gave them work to do over the weekend and they both finished early. Facing final exams this week, they simply turned in the first draft of this week’s 5 Things a full day early. No complaining – just execution. With a work ethic like that, a consistently positive attitude, and active minds, does anyone else think they’re both going to be successful? I do!

Ready to find out who really killed Spirit Airlines in the conservatory with the lead pipe? Let’s dive in:

1) What Really Killed Spirit Airlines:

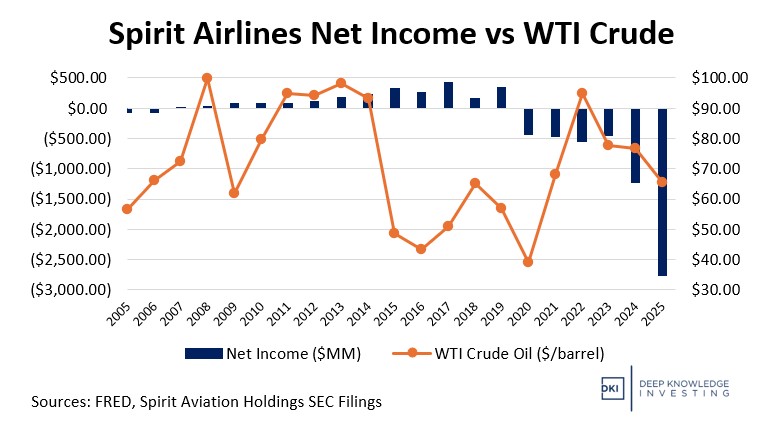

Last week, Spirit Airlines declared Chapter 7 resulting in the closure and liquidation of the business. X accounts immediately began assigning political blame. The people who lean Republican pointed to Senator Elizabeth Warren bragging that she had been warning that an acquisition of Spirit by Jet Blue would lead to “fewer flights and higher fares”. When the DoJ succeeded in blocking the merger, Warren claimed that “This is a Biden win for flyers”. The people who lean Democrat claimed that President Trump is at fault because the war in Iran has led to higher oil prices. They say the increase in the price of crude led to losses at Spirit that caused the bankruptcy. Higher oil prices are never a positive for airlines, but I think the people claiming oil is the reason for the bankruptcies are missing something. Let’s look at the data first. (Afterwards, we can point fingers at politicians.)

No correlation in early years. Negative correlation in last three years.

What if the real cause was poor management.

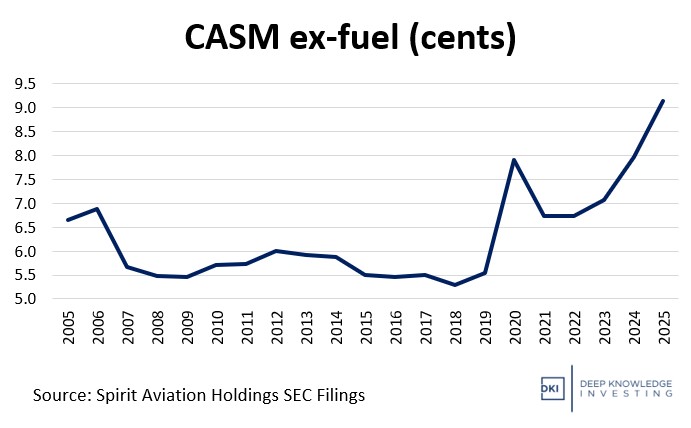

DKI Takeaway: Please look at the first graph above. Spirit’s profitability generally rose from 2005 through 2017 despite fluctuating oil prices. Net income turned negative in 2020 due to Covid-related travel fears and restrictions. As “revenge travel” exploded in 2022 combined with inflation caused by money-printing, oil prices spiked leading to greater losses. Again, look at the first chart above. As oil prices came down from ’23 to ‘25, Spirit’s losses increased. Clearly, the problem wasn’t the cost of oil. Now, look at the second chart. CASM stands for Cost per Available Seat Mile. It’s a measure of operating efficiency that measures how much it costs an airline to fly one seat for one mile. Spirit used to be a low cost / low ticket price airline, but in the past few years, it’s run an expense structure that’s closer to that of the full-price major airlines. Elizabeth Warren and the Biden Administration made a mistake blocking the Jet Blue merger. Spirit management made a bigger mistake by not controlling costs. My full analysis here.

2) Big Tech Earnings are Strong – So is Cap-X:

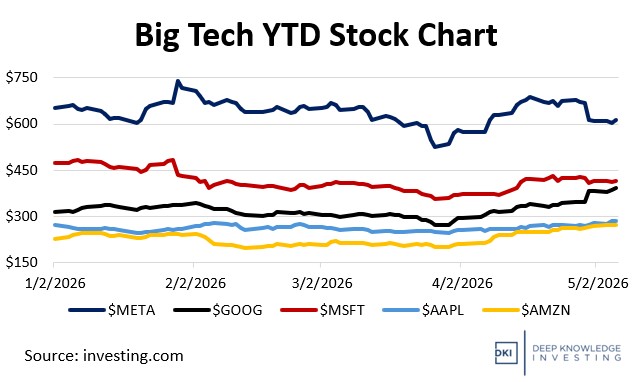

Alphabet, Microsoft, Meta, and Amazon reported earnings within hours of each other on April 29, with Apple following on April 30. Alphabet led with $109.9B in revenue, up 22%, with Google Cloud surging 63% to $20B, and net income rising 81%. Meta posted $56.3B in revenue, up 33%, with net income climbing 61% to $26.8B. Amazon grew net sales 17% to $181.5B, with AWS expanding 28% to $37.6 billion. Microsoft reported strong AI-driven cloud results, with its AI annualized revenue run rate surpassing $37.0B. Apple, reporting its fiscal Q2 ended March 28, posted $111.2B in revenue, up 17%. The iPhone achieved a 2Q record of $57.0B while Services reached an all-time high of $31B. The market focused on AI Capex, with the four hyperscalers projecting $725B in AI infrastructure spending for 2026. Apple also projected a 33% increase in R&D citing AI as the key driver.

Wall Street loves AI growth. It’s concerned about AI spending.

DKI Takeaway: The AI trade is still driving markets. Valuations may be high, but these companies are generating outstanding revenue and profit growth in their core businesses. Analysts were too conservative. They projected 18% revenue growth this quarter for Mag7 ex-Nvidia according to Bloomberg Intelligence. These companies are now on track to grow revenue 57%. The one negative for the stocks is the market is starting to show concern about AI capital expenditures. Investors are rewarding companies where AI spend is leading to revenue (Alphabet’s 63% cloud surge and the increase in growth at Amazon Web Services). Investors are less happy with companies where the AI return on investment is unclear. Meta’s stock dropped 8.6% despite a great quarter because it raised its 2026 capex guidance to $125B – $145B spooking investors worried about the return timeline. The market is telling these companies that it will support AI infrastructure spending if it comes with evidence that there’s attached revenue.

One additional note here: I saw a political operative complaining that it was horrible that these companies all report within minutes of each other because Wall Street analysts need to have opinions immediately and don’t have the time to look at multiple sets of reports before they have to respond. To me, it seems obvious that the big tech firms all report at the same time to create this kind of confusion. It’s easier to write a piece lauding big revenue growth than it is to go through the results and figure out where the problems are with cap-x and depreciation. For your benefit (which is the only thing I care about here), please remember that sell-side “research” is not intended to help you make money. It is a marketing expense designed to help the big banks win investment banking business from the companies they cover. The issue isn’t that the sell-side doesn’t have time. They could take more time if they cared about the quality of their recommendations. The real issue is you are not intended to be the beneficiary of their efforts.

3) GameStop Offers $56B for eBay:

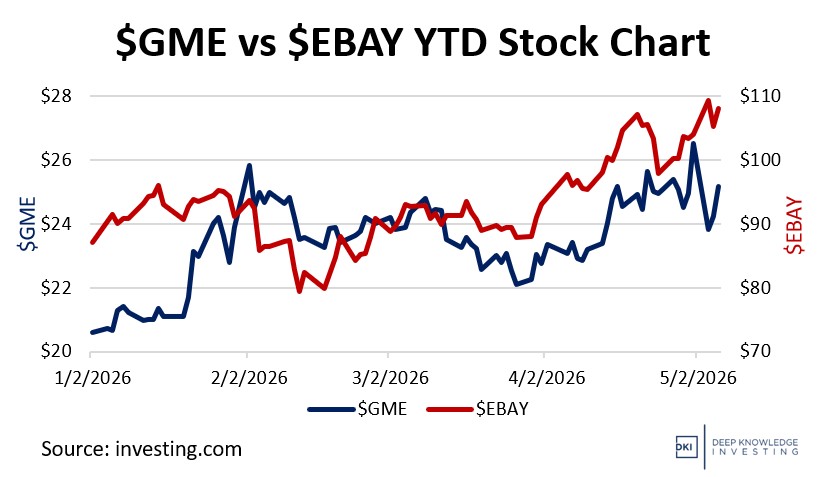

GameStop offered to acquire eBay for $125/share or $56B. The offer is half cash and half stock. Before announcing the bid, GameStop acquired a 5% stake in eBay. GameStop has about $9B in cash so needs to raise almost $20B more to finance the deal. GameStop management says it can cut $2B in costs by targeting product development and administration. CEO, Ryan Cohen, has stated that this acquisition could turn eBay into a rival to Amazon and other large e-commerce platforms.

eBay stock barely moved b/c the market is skeptical $GME can complete the deal.

DKI Takeaway: This is an unconventional deal. GameStop has a market cap of $11B, roughly one-fifth the size of the eBay offer. The structure of the deal requires significant external financing and issuance of more than 100% of $GME’s equity which creates meaningful dilution for the existing GameStop shareholders. The size difference between the two companies plus financing concerns makes a deal challenging. DKI Interns suggest the bid functions as more of an attention-seeking move than an acquisition attempt. I admire and applaud their critical cynicism!

4) Regis Resources and Vault Minerals Announce $7.7B Merger:

Regis Resources and Vault Minerals announced a merger with a combined value of $7.7B. Each Vault share will be converted into 0.6947 Regis shares, an 11% premium to the pre-deal price. Regis shareholders will own 51% of the combined company and Vault shareholders will own 49%. The deal creates Australia’s third-largest ASX-listed gold producer, with five Western Australian operating mines, annual production above 700,000 ounces, and a 20.5MM ounce reserve. Both boards unanimously approved the transaction, which is expected to deliver hundreds of millions in corporate tax benefits. The deal should close this summer subject to shareholder and regulatory approvals.

Almost a merger of equals.

DKI Takeaway: This merger turns the combined company into a globally relevant producer. Regis Resources’ total production capacity will go from 373,000 ounces to over 700,000 under the new entity. The combined company will have almost $2B in cash on the balance sheet which provides a path for new potential acquisitions. The deal also diversifies operational risk across five hubs in Australia and nine processing plants. Total milling capacity would reach 22 million tonnes/year creating an infrastructure moat. DKI has owned gold since it was $1,500 and we remain long-term bullish.

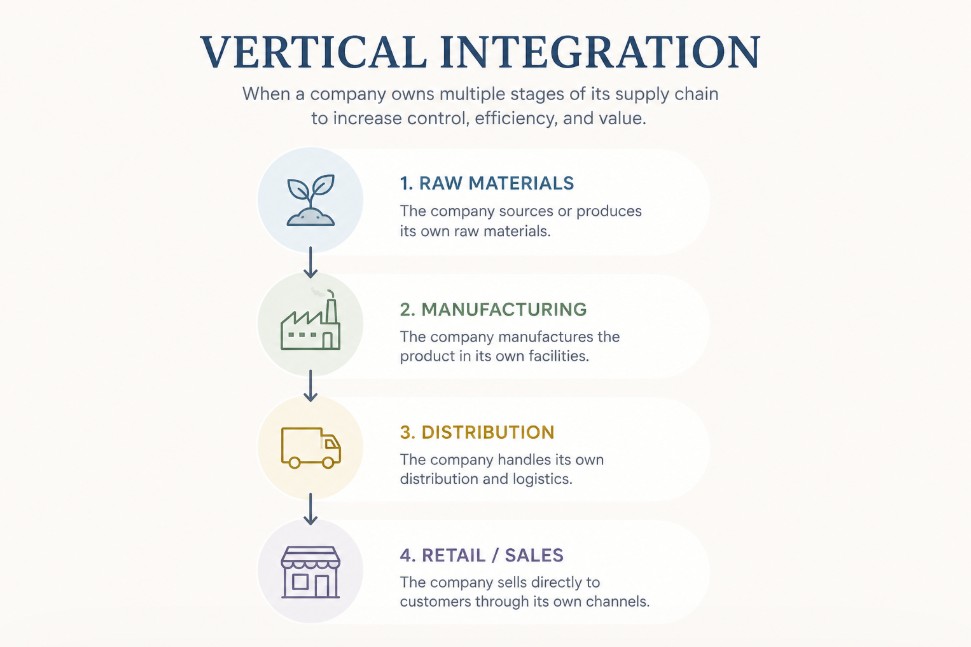

5) Educational Topic: Vertical Integration:

Vertical integration is a strategy where a company takes ownership of multiple stages of its supply chain rather than relying on outside suppliers or distributors. A company can integrate “backward” by acquiring its input suppliers, or “forward” by taking control of distribution and retail. The goal of doing so is eliminating middlemen in order to reduce costs, improve margins, and give the company greater control over quality and pricing. An example is Apple, which designs its own chips, builds its own operating system, and sells directly to consumers through its own stores. This captures value at every step of the process. The tradeoff is that vertical integration can require additional spending and lead to a loss of focus. If it’s done well, it can create a competitive advantage. If it’s not, it can cause inefficient operations that an outside supplier could have handled at lower cost.

It all comes down to whether you are you better off owning or buying capability.

DKI Takeaway: Vertical integration is one of the clearest indicators of a company’s long-term competitive positioning. Companies that control their supply chain tend to have stronger and more predictable financial positioning. This is also something that competitors and suppliers need to watch, as it presents risk for them. This is relevant today as even the biggest AI player in the world, Nvidia, faces a very real threat to its positioning. The big hyperscalers are designing and manufacturing their own chips for their own data centers.

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.

{kind=link}