It was a busy news week so we’re going with 6 Things this edition. Intel reports a fantastic quarter sending the stock up more than 20% in the aftermarket. DKI subscribers earn 130% in five months. Sysco is acquiring Jetro for $29B. The world’s largest food distributor will now have physical locations. Texas Pacific Land has been a DKI position for four years. We’ve traded it well making more than 100% returns on multiple occasions. We recently sold some at $540 and bought it back below $400 before making more than 10% in two weeks. Sounds great, but the circumstances were terrible. Our condolences to the Stahl family and to the team at Horizon Kinetics. The SEC is changing tender rules to speed up cash deals. That works to the advantage of acquirors. Under some circumstances, it’s good for investors, but it might limit competitive bidding. The White House is using tariffs to increase domestic pharmaceutical manufacturing. I’m generally against government interference in the private economy, but do we really want control of the US drug supply in the hands of China? Ever wonder what the yield curve is, or what an inverted yield curve means? What role does the Fed play in setting the curve? We explain in this week’s educational topic.

This week, we’ll address the following topics:

- Intel reports earnings of $.29 vs analyst estimates of $.01. Sales would have been higher, but the company can’t meet growing demand. DKI has made 130% in five months in the name.

- Sysco is acquiring Jetro for $29B. The merger will create an omnichannel model with wholesale and delivery options. Sysco remains the largest food distributor in the world.

- DKI has traded $TPL volatility profitably for the past four years. The last time was due to the untimely death of legendary investor Murray Stahl.

- The SEC is changing rules for tender offers to the advantage of acquirors. Want to know the implications? Read on!

- The White House is incentivizing pharma companies to build domestic manufacturing and getting allies to start paying more of the drug discovery bills previously shouldered by Americans.

- We hear a lot about the yield curve. If you’ve ever wondered what it is and what role the Federal Reserve plays, then check out this week’s educational topic.

DKI interns, Samaksh Jain, Kunal Arora, and Elijah Killorin do their usual fantastic job on this week’s 5 Things. Please extend to them a mental round of applause for much of what you’re about to read. Their capacity for high-level finance work far exceeds my own at their age.

Ready for a week of fantastic Intel earnings and DKI profits? Let’s dive in:

1) Intel Crushes the Quarter:

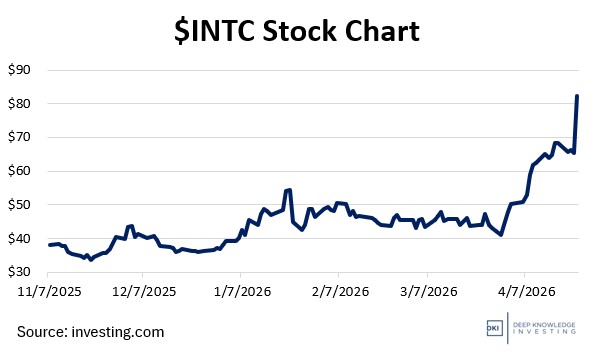

Intel announced earnings on Thursday and the stock was up 22% in the aftermarket. Revenue of $13.6B was far above analyst estimates of $12.4B. EPS of $.29 more than doubled last year’s $.13 and crushed analyst estimates of $.01. Revenue and earnings guidance for 2Q were also well-above estimates. For the second quarter in a row, Intel didn’t have enough supply to keep up with demand. As far as problems go, that’s a good one to have. The CFO said that lack of supply limited revenue by more than $1B and that they expected the situation to improve this year. Commentary on the 18A plant was positive with yields ahead of expectations. I did a huge number of research calls on this topic, and success with 18A was a key part of DKI’s positive thesis on the stock. Management talked extensively about the shift in AI from training to inference leading to datacenter computing share moving from GPUs to CPUs, another key part of our thesis.

Another fantastic quarter for DKI stock pick, Intel.

DKI Takeaway: Intel reiterated that Google had agreed to a multi-year deal to buy Xeon processors for its AI datacenter servers. Sales of the Core Ultra Series 3 chip represent the fastest sales ramp the company has seen in five years. (I use and like the Core Ultra line in my laptops.) There was also positive commentary about the new deal with Elon Musk to partner with him at the new Terafab plant on AI chips for xAI, SpaceX, and Tesla. If you want to produce high-end silicon outside of Taiwan, Intel is the obvious partner. DKI started buying the stock in the $34 – $37 range five months ago. Since then, it’s up 130%. If that’s interesting to you, you’re welcome to subscribe.

2) Sysco Announces $29.1 Billion Acquisition of Jetro:

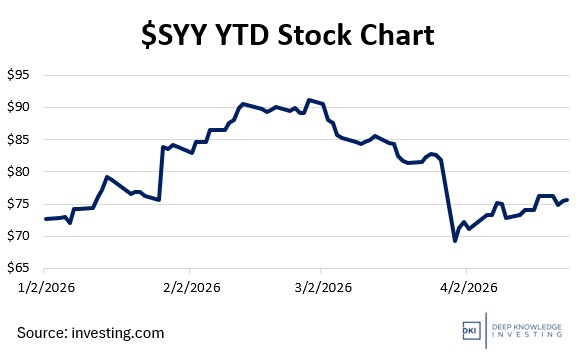

At the end of March, Sysco announced that it would be acquiring Jetro Restaurant Depot, the premier Cash & Carry food wholesaler in the nation, for $29.1 billion. Jetro shareholders will receive $21.6 billion in cash along with an additional 91.5 million Sysco shares. The total valuation is based on a Sysco stock price of $81.80. Jetro serves as a supplier of food to independent restaurants and businesses, operating 166 large-format warehouses across the nation, combined with over 725,000 independent operators.

The stock fell due to concerns about the debt load.

DKI Takeaway: Sysco’s business model is based around last-mile delivery to customers. They serve high-volume clients like large restaurant chains, hospitals, and stadiums. They’re the largest foodservice distributor in the world and operate as an intermediary between food makers and businesses. Jetro’s operations require individuals and businesses to come to their stores in-person. The combination creates an ideal omnichannel model of operations, allowing the company to capture the full range of food service, from in-person wholesale to on-demand delivery. It also represents a fundamental shift for Sysco as it enters a new industry segment, broadening its total addressable market. Sysco’s revenue should increase by 20% and free cash flow is expected to increase 55%. The company will be taking on a large debt load as it completes the largest acquisition in food-service history. The stock fell on the announcement because Sysco is financing the entire $21B cash portion. The company is focused on decreasing its debt-to-EBITDA to 1.0x in the next two years.

3) $TPL and the Anatomy of a Trade:

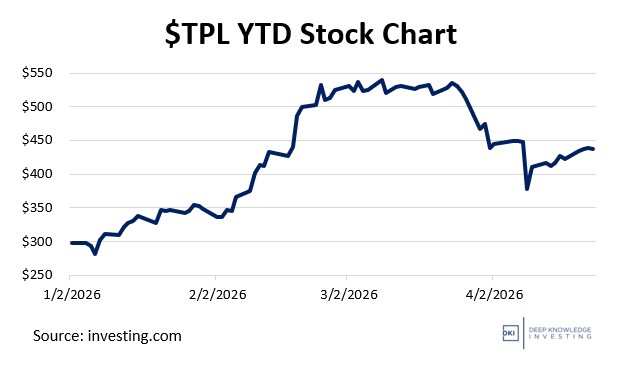

My investing focus is finding a limited number of situations where we can earn a very high return over a long time-frame. On occasion, a volatile stock can produce multiple opportunities to earn much higher returns. DKI started buying Texas Pacific Land ($TPL) in 2022 at $121. Nine months later, we sold most of that position for $295. In 2023, we started buying again at $150 and sold most of that position in 2024 for prices ranging from $250 to $460. $TPL is a remarkable company. It owns land in the Permian Basin and companies pay it royalties to produce oil and to access water rights. Soon, there will be AI datacenters on the land with access to electricity. It’s a fantastic long-term holding where routine volatility creates the opportunity to improve investing returns. What we’ve done is to hold a long-term position, add and be overweight when the stock falls, then sell some and be underweight when it rises.

2026 Volatility has been both profitable and tragic.

DKI Takeaway: $TPL stock rose from the low-$270s in December, 2025 to $540 by March. At that point, it had doubled in a few months and become a 15% position. I sold some (disclosed on the DKI premium blog) at $540 purely for risk-control. We got the timing right and $TPL started to fall on fears that the big hyperscalers aren’t earning a return on massive AI spending leading to datacenter demand concerns. The stock then fell further due to fears that war-related higher oil prices would reduce demand for AI datacenters. Two weeks ago, the stock plummeted on the unfortunate death of Murray Stahl. Murray was the CEO of Horizon Kinetics, the largest shareholder of Texas Pacific. He was also a legendary investor and a brilliant detailed-oriented stock analyst. The stock plummeted that day on incorrect fears that there would be forced selling of $TPL stock. We bought back our entire position in the high $390s. The stock is up 11% in the two weeks since then. This is a strange job sometimes. On many occasions during my career, I’ve found myself experiencing negative emotions due to a tragedy. That doesn’t change the responsibility we have to do the best we can for our investors and subscribers every day; even when the circumstances are terrible. DKI wishes to express our sincere condolences to the Stahl family and everyone at Horizon Kinetics.

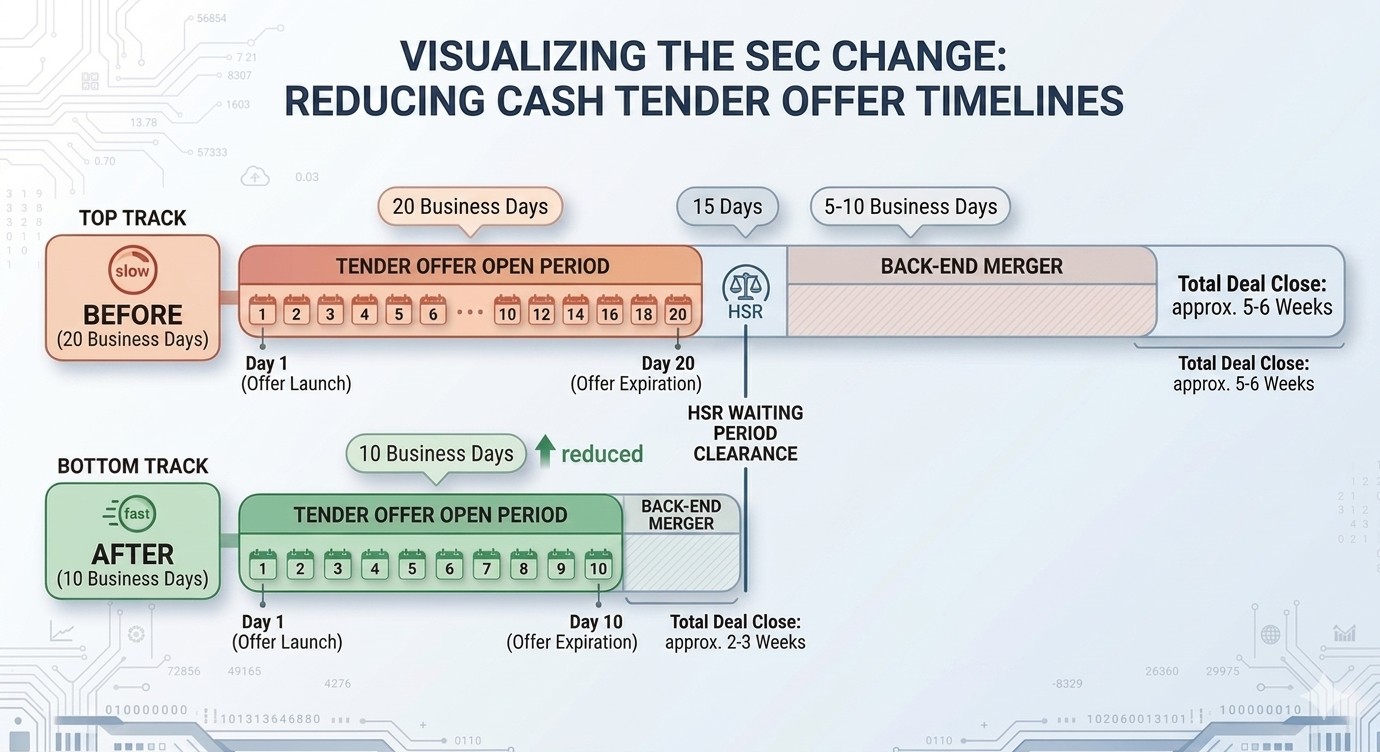

4) SEC Halves Tender Offer Timeline, Accelerating M&A Execution:

The US Securities and Exchange Commission has issued new exemptive relief cutting the minimum tender offer period for certain all-cash equity deals from 20 business days to 10. The change applies to fixed-price, cash-only offers, including many negotiated acquisitions and issuer self-tenders, and is designed to address market inefficiencies and reflect faster information circulation in modern markets. By compressing the required timeline, the rule can reduce the gap between deal announcement and completion to as little as two to three weeks in well-structured transactions. While certain transactions, such as take-private deals or competing bids, remain subject to longer timelines, the shift lowers a key procedural barrier that has historically slowed deal execution.

HSR review still exists. It’s 15 calendar days & runs concurrent with the 10-business day waiting period. Not shown above because it can only cause a 1-day delay.

DKI Takeaway: This is a structural tailwind for M&A activity. Shorter tender windows reduce execution risk by limiting exposure to market volatility and competing bids, thereby increasing deal certainty for acquirers. At the same time, faster timelines can tilt the balance of power toward buyers, especially when boards have less time to evaluate alternatives or mount defenses. That dynamic raises the probability of more opportunistic or hostile approaches, particularly in cash-heavy sectors. For investors, the implication is a more active deal environment with tighter spreads and quicker arbitrage cycles, but also a higher risk that deals will move before the opportunity for full price discovery.

5) White House is Pressing for More Domestic Pharma Manufacturing:

The White House imposed a 100% tariff on imported patented drugs and active pharmaceutical ingredients. This policy targets branded medications listed in the FDA Orange and Purple books because the government views relying solely on foreign manufacturing as a national security risk. (I agree and have been writing this for years.) While the baseline rate is 100%, countries with trade agreements like Japan and the EU face a lower 15% rate. Companies can also reduce their specific rates to between 0% and 20% if they commit to onshoring plans or price matching. The tariffs will begin for 17 large manufacturers on July 31, 2026.

More domestic supply. The tariffs are working as intended.

DKI Takeaway: This acts as a reset for the global drug supply chain. The government is giving Big Pharma a choice to either invest in American production or accept lower margins. This pressure has already incentivized the 17 largest pharmaceutical companies to enter negotiations to discuss deals that lock in lower tariff rates. In exchange for these lower rates, companies are committing hundreds of billions of dollars to increasing domestic production. The administration is also using these deals to force price concessions and match the lowest global rates. This has led to a recent UK pharmaceutical partnership. This deal grants the UK 0% tariffs in exchange for the British government doubling its spending on new medicines. By increasing the price they pay for treatments, the UK is helping subsidize global R&D costs. This takes some of the financial pressure off the U.S. market, which has historically paid the highest prices to fund drug development. I’ve always been against government interference in the private economy. In this case, it’s dangerous to hand so much control of our drug supply to the Chinese and unfair to have American citizens subsidizing drug development costs for first-world allies.

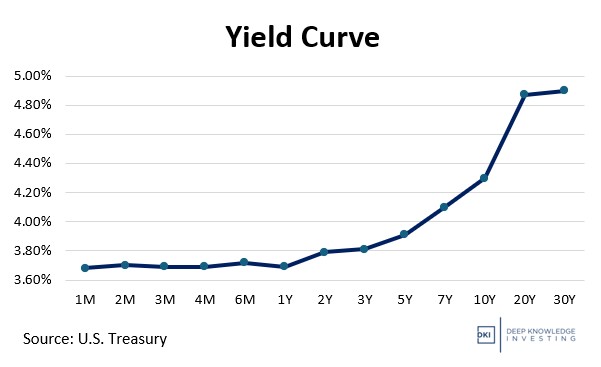

6) Educational Topic: Yield Curve:

The yield curve is a graph which represents the relationship between market interest rates and the time to maturity. The vertical axis represents the annual yield of Treasuries while the horizontal axis shows the time to expiration. A normal yield curve is upward sloping because investors demand a higher return as compensation for the risk that comes from a longer time-frame. An inverted curve is when short-term interest rates are higher than long-term rates. It is also a good recession indicator as it means bond investors are expecting future rate cuts due to weakening economic conditions.

Today’s yield curve is “normal”. Investors get paid more for longer-dated Treasuries.

DKI Takeaway: There is a common misperception that the Federal Reserve sets interest rates. This is not true. The Fed only sets the overnight rate. The rest of the curve is set by the bond market. Right now, we see a steepening of the curve starting at the 5-year mark because the bond market is correctly pricing in higher long-term inflation. A higher inflation rate means the value of dollars many years in the future will have reduced purchasing power. Many refer to US Treasuries as “risk free”. That’s true to the extent that the government will print more dollars to pay you what you are owed. However, those dollars will have reduced purchasing power ensuring that you lose value despite having no repayment risk.

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.