Quick announcement: I’ll be in Bangkok, Thailand for the next 1 – 2 weeks before returning to New York briefly. While I’m here, I’m open to a small number of in-person conversations. If you’re based locally, or know someone here you think it would be worthwhile for me to meet, feel free to reach out privately at IR@DeepKnowledgeInvesting.com.

The Fed met and kept the fed funds rate unchanged. However, a more hawkish dot plot has Treasury yields rising and gold prices falling. Can the Fed do anything about this? No – no they can’t. The SEC is considering allowing companies to report earnings twice a year. I have mixed feelings about this, but suspect they’ll be irrelevant as most companies have an incentive to report more often. Tesla is building a new fab plant in Texas with plans to produce 100B – 200B chips a year. That’s a huge number. Lots of chip-making capacity being added in the US now. We’re pleased to see that. Private credit investors are starting to worry that their low-vol (read: not marked to market) investments aren’t doing well. Investment managers are throwing down the gates and not allowing full redemptions. Finally, do you ever struggle with negative feelings when your portfolio isn’t doing well? Of course you do – we all experience that. We address how to deal with that and avoid bad decisions in this week’s educational topic.

This week, we’ll address the following topics:

- Gold falls this week as US Treasury rates rise and the Fed dot plot looks more hawkish. Is there anything the Fed can do?

- The SEC is considering allowing companies to report earnings twice a year instead of quarterly. I have mixed feelings about this.

- Tesla is building a new fab plant in Texas. It will cost $25B and will produce 100B – 200B AI chips per year. US semiconductor manufacturing is experiencing a renaissance.

- Private credit investors are starting to show concern regarding the black boxes they own. They’re coming to terms with the fact that not marking the book to market doesn’t mean low volatility and private means gated exits.

- In this week’s educational topic, we’re going to address the crucial topic of how to handle negative emotions when investing. We all experience them. Let’s not allow them to push us into bad decisions.

Excellent work by DKI’s interns, Cashen Crowe, Samaksh Jain, and Kunal Arora this week. As always, they do much of the heavy lifting for each week’s 5 Things.

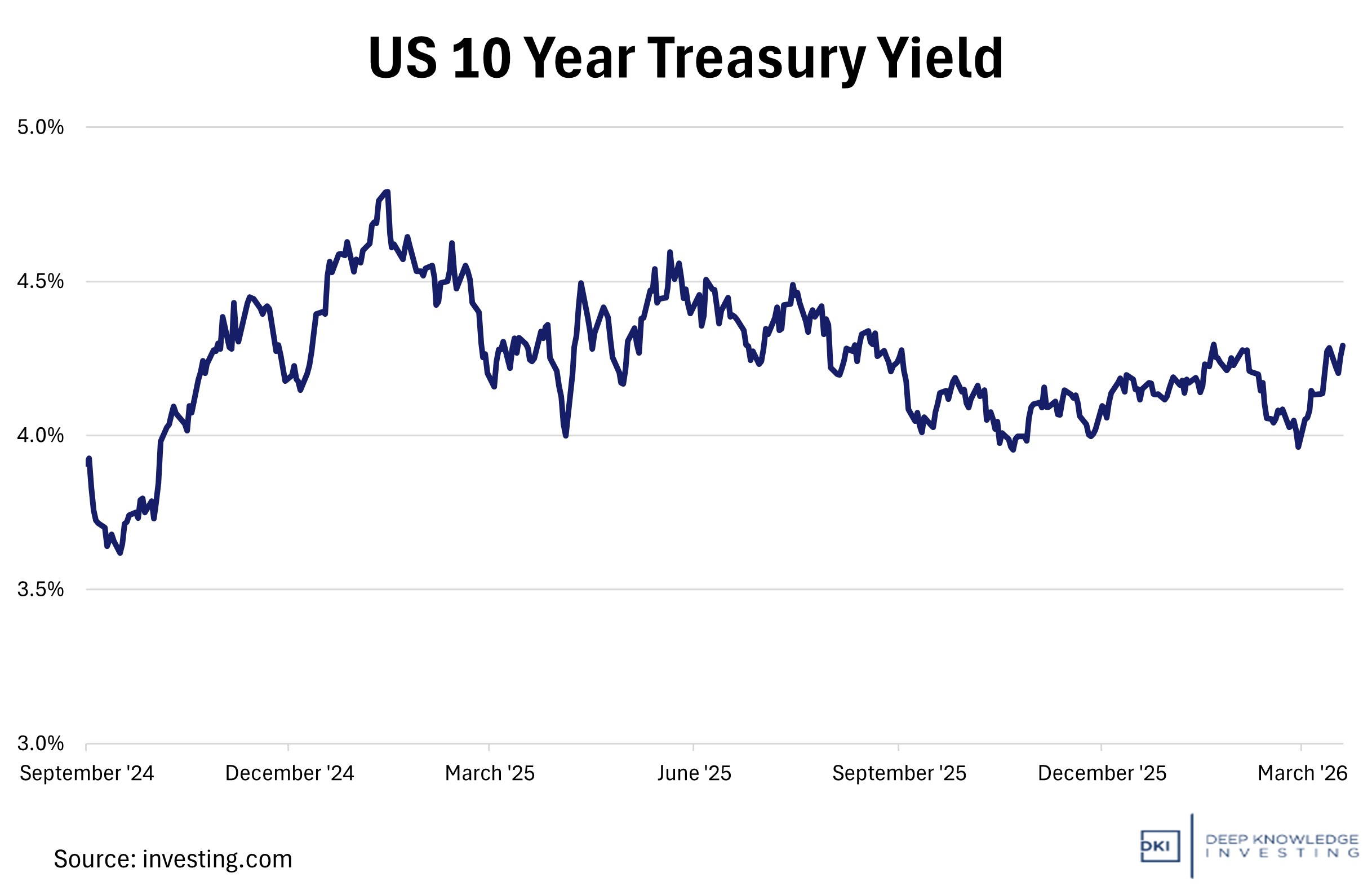

1) US Treasury Yields are Back on the Rise – The Fed Can’t Help:

Treasury yields have been climbing this past month due to stubborn inflation data and geopolitical pressure. The 10-year Treasury rose from 3.97% in late February to 4.39% as of this writing. Surging oil prices, sticky inflation, and concerns about additional war-related debt are all culprits. The February PPI rose 0.7% vs last month which annualizes to 8.7%. Some are blaming a newly hawkish Federal Reserve. The Fed held the fed funds rate unchanged and revised its inflation projections higher. Does this matter?

Six quarters after the Fed started cutting has led to HIGHER 10-year yields.

DKI Takeaway: There is nothing the Fed can do. There is a misconception that the Federal Reserve controls interest rates. They control the overnight rate with the bond market pricing the rest of the yield curve. If the Fed were to cut, the bond market would price in higher long-term inflation and the yield on the 5-year (used to price corporate debt) and the 10-year (used to price mortgages) Treasuries would rise. This is exactly what DKI predicted in the summer of 2024 and exactly what happened when the Fed started cutting that September. There is also a misconception that the Fed can get you lower housing costs. As above, a cut in the fed funds rate is likely to lead to higher mortgage rates. In addition, lower mortgage rates don’t change the monthly payments new home buyers pay. It just shifts the balance from interest to principal due to higher asset prices. Low interest rates = higher prices for hard assets like real estate. It’s going to take spending cuts out of Congress to get us lower long-term inflation and interest rates. That’s not going to happen.

2) SEC Eyes Shift to Semiannual Reporting:

The US Securities and Exchange Commission (SEC) is exploring a shift from mandatory quarterly earnings reporting to companies having the option to report twice a year. Companies would be allowed to continue quarterly reporting, but could choose reduced frequency. The rationale centers on reducing compliance costs and potentially alleviating the pressure on management teams to prioritize short-term earnings over long-term value creation. Quarterly reporting has long been criticized for encouraging “earnings management” and fostering a market environment overly focused on near-term results. By extending these reporting intervals, the SEC aims to give companies more flexibility to invest in longer-term initiatives without the constant scrutiny of quarterly benchmarks.

An option to report twice a year.

DKI Takeaway: I have mixed feelings about this. It’s common for companies to manage short-term earnings at the expense of long-term value creation. (I used to invest in thrifts and mutual thrift conversions where reserves were raided or added each quarter to ensure the company beat earnings estimates by $.01.) There are also fewer publicly-traded companies because the regulatory and reporting costs are so high. Given that management teams are no longer able to provide any detailed information to investors on private calls, there is a danger to reduced reporting. If companies are going to head this route, I’d like to see them at least provide some financial information every three months. For some companies, that might be sales or bookings. For others, it could be free cash flow or the cash balance. I suspect that if this proposal were to be approved, few companies would take advantage of the reduced requirement because doing so would be a negative signal to investors and would lead to allegations that management is hiding information.

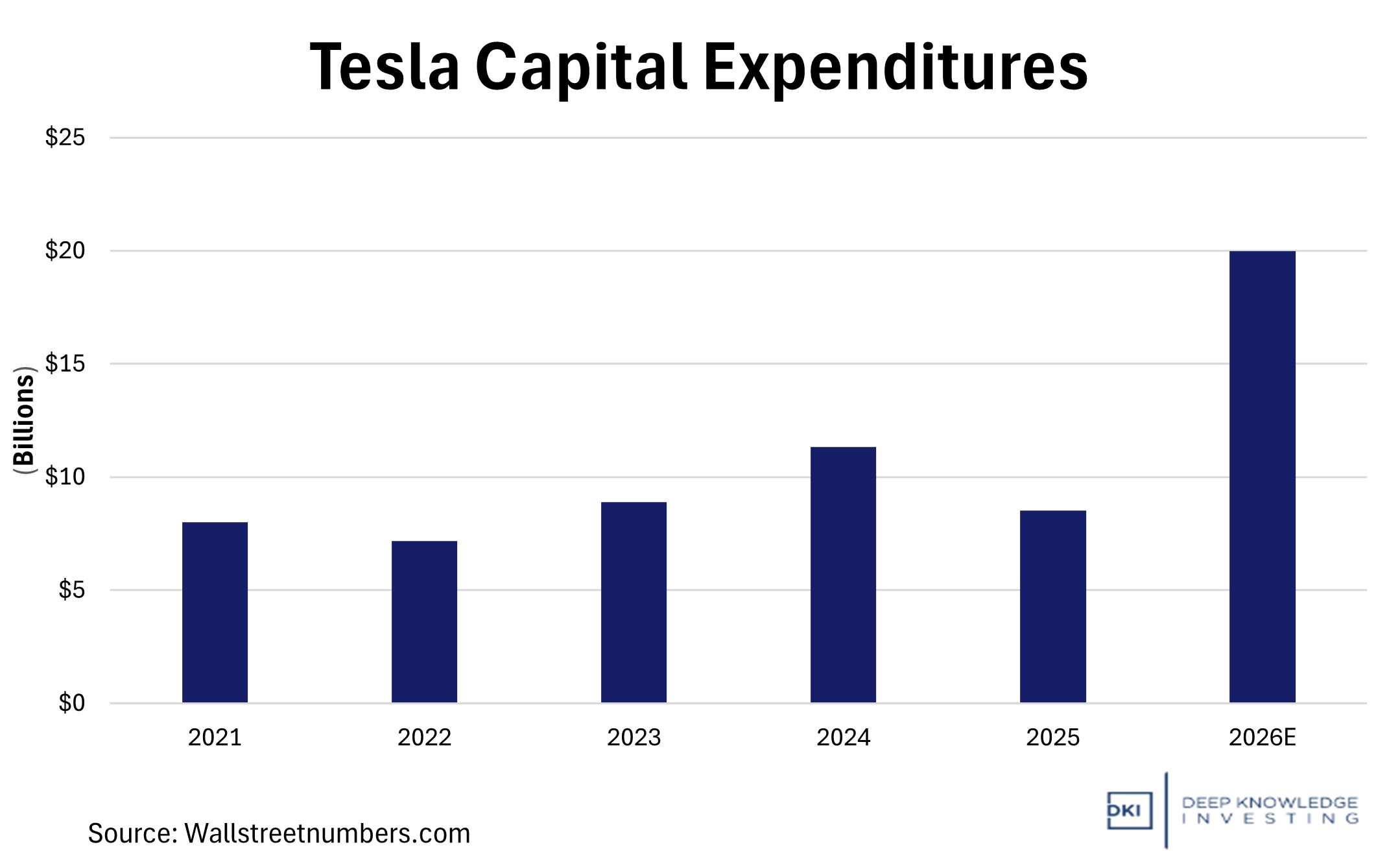

3) Tesla Announces Project Terafab:

Elon Musk announced that Tesla’s Terafab Project is set to launch this week. It’s a plan to build what he envisions as the world’s largest semiconductor fabrication plant. Tesla disclosed Terafab in its last earnings call, where Musk told investors the company needs to build a chip fabrication facility to avoid a supply constraint projected to materialize within three to four years. The project is intended to produce 100 to 200 billion AI and memory chips every year, costing between $25-35 billion to complete. (I was about to criticize the interns thinking it had to be 100MM – 200MM chips. That number is both crazy and correct.) Among the first products the factory is set to produce is the Tesla AI5 chip, designed to advance self-driving technology, the Cybercab robotaxi program, and the Optimus humanoid robot line.

To produce at that scale, the cap-x budget is going to have to rise.

DKI Takeaway: Samsung, Micron, and TSM are Tesla’s main chip suppliers, and according to Elon Musk, they won’t be able to meet Tesla’s chip demand within the next 3-4 years. Tesla’s Terafab Project marks a significant shift in the company’s strategy as well, moving beyond its normal market as an automaker and beginning vertical integration of chip manufacturing. This doesn’t come without concerns. Tesla’s Capex guidance for this year was over $20 billion, and that doesn’t include this project, which would require tens of billions more to complete. The company has enough cash on hand, but free cash flow will suffer. Still, the old adage “Never bet against Elon” exists for a reason. The new plant will be located in Texas. Between this, new TSM fab plants under construction in the US and Intel’s 18A US-based plant off to a good start, the domestic chip-building business is showing signs of life.

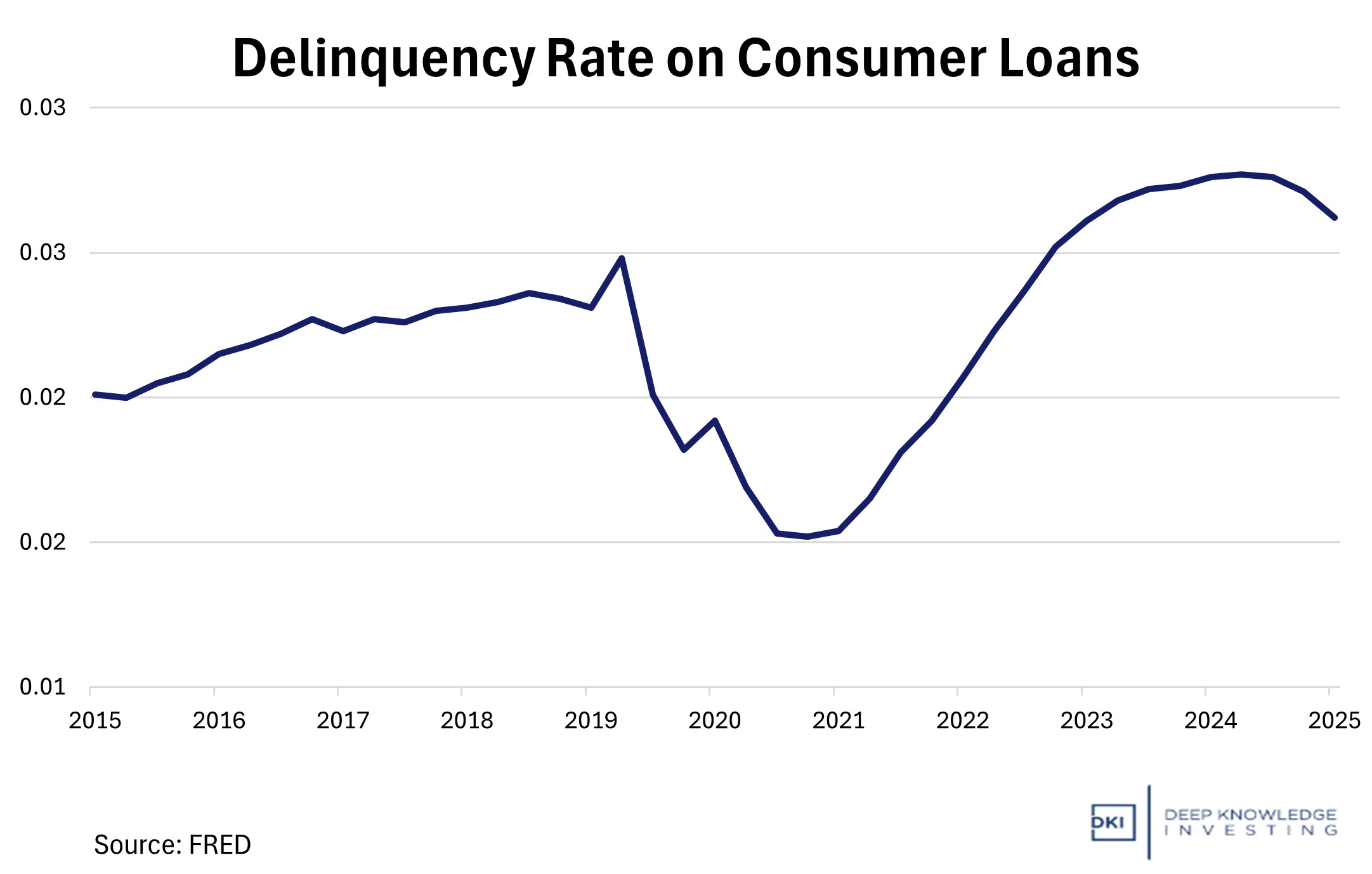

4) Private Credit’s Liquidity Test Spreads from Corporate Lending to Consumer Loans:

A recent private credit exodus has spread to consumer loans, highlighting a shift in the private credit market: investor redemptions are no longer confined to corporate direct lending funds and are now spreading into consumer loan portfolios. Funds that had expanded aggressively into buy-now-pay-later (BNPL) and personal loans are facing rising withdrawal requests from investors. Because these funds typically hold illiquid loans, it’s often difficult to meet redemption demands, forcing gating and delayed payouts. This is creating a mismatch between investor expectations and the illiquid nature of private credit assets.

One of the core selling points of private credit over the past decade has been high returns with limited volatility. Concerns around credit quality are increasing, particularly in consumer lending, which is more sensitive to economic slowdowns and inflation pressures. In many cases, the lack of volatility in private investment returns is nothing more than not marking the book to market on a regular basis.

It’s a low delinquency rate, but investors are reasonably concerned about an increase.

DKI Takeaway: Borrowers that rely on private credit, especially fintech lenders and nonbank consumer platforms, could face tighter funding conditions and higher borrowing costs. It is possible that this could lead to reduced loan origination volumes and stricter underwriting standards. (The later would be a sign of credit markets operating in a sensible manner.) This represents a stress test for the private credit ecosystem. The asset class has grown rapidly, benefiting from low defaults and strong investor demand. Some of these markets are testing liquidity and some funds are not honoring redemptions as fast as investors would like.

5) Educational Topic: Emotional Detachment:

It’s normal to experience negative emotions when our portfolio isn’t doing well. Many people think professional investors don’t experience the same feelings that amateurs do. I can assure you that for the vast majority of us, that isn’t true. Losing money is horrible. When my portfolio isn’t doing well, I often feel awful. That’s compounded by the fact that when I’m not doing well, that means DKI’s subscribers probably aren’t either. Having a hand in the losses of others can feel even worse than losing my own money.

Negative feelings don’t need to determine our actions.

DKI Takeaway: When I have these feelings, I do the following: First, identify the emotion. We can’t control ourselves if we can’t figure out what we’re experiencing. It can be as simple as “I feel worried that today’s loss will make it harder for me to make a downpayment on a house.” Second, accept the feeling. “It’s normal and reasonable to feel worried or anxious during a period of negative performance.” Third, put those feelings aside and use reason and research to examine your positions and portfolio. Is your investment thesis still valid or has something changed? Accept short-term volatility and uncertainty. Investing success comes from using a consistent process to identify under-valued opportunities. That’s a probability bet and not a sure thing. If you want to read more about how I approach these situations, check out DKI’s recent article, “Finance and our Feelings – A Three Step Plan to Avoid Bad Decisions”.

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.

The point about private credit investors facing redemption gates really stood out — that’s a quiet storm brewing beneath the surface of a seemingly calm market. It reminds me of the 2020 bond fund freeze-ups, where the lack of daily pricing masked real damage until it was too late. These structures feel fine until everyone tries to leave at once.

Hi ColorMe. Sorry for the late response. This got sent to spam incorrectly. I agree with you. There is a sense when investing that liquidity will be better than actual experience. And the lack of daily mark-to-market is an incredible marketing trick. These funds keep touting low-volatility. But if you never mark your book, then it’s always worth the same amount! Thanks for commenting.