The Disaster Edition!

Sorry for the clickbait headline. We don’t have an actual disaster right now; just a few potential ones. If you’ve been sleeping too well at night, then keep reading. We’ll tell you the things that should be worrying you. Don’t want to worry too much? No problem – Just subscribe to DKI and we’ll handle the worrying for you.

Seriously, given that the market close has had no correlation with the overnight futures or even the open, I have no idea why I check the futures at 3am every night. It’s the most pointless thing I do all day (night). If you can tell me why I’m doing this, I’ll give you a free month of DKI premium (but then you have to do the worrying for me).

On the positive side, we just got a fantastic earnings report from DKI Stock Pick, Las Vegas Sands ($LVS). DKI subscribers made 23% in a month and a half in 2020 the first time we recommended it. We recommended it a second time, and the stock is up 43% this time (so far). If that’s interesting to you, feel free to reach out at IR@DeepKnowledgeInvesting.com.

1) The Bank Walk and Corporate Earnings

Jim Bianco of Bianco Research has been writing about a bank walk (as opposed to a bank run). His excellent point is that with some Treasurys and deposit accounts paying 4% – 5%, bank depositors have an incentive to pull funds from banks paying close to zero. Those outflows, plus money that will be paid to the IRS this month could lead to a reduction of funds in the banking system. This would cause banks, which have already tightened credit standards, to reduce lending further. Full DKI analysis on the situation is here.

DKI warned about too high earnings estimates in June of ’22.

DKI Takeaway: Tighter credit and reduced funds availability would slow the economy and lead to further reductions in earnings. In last month’s minutes, the Federal Reserve even explained that problems with bank credit could have the same effect as further rate increases. (DKI analysis here.) Banks pulling back from lending would be a positive for DKI stock pick Enova International ($ENVA) which makes loans to small and medium businesses.

2) A “Credit Event” is Coming:

Michael Gayed has warned of a coming “credit event”. Many companies took advantage of near-zero interest rates in recent years to take on additional low-cost debt. The fed funds rate has gone up from around zero to 5% in the last five quarters. As previous credit lines expire or low-rate bonds mature, these companies are going to need to refinance at much higher rates which will affect earnings negatively.

The fed funds rate isn’t high by historic standards, but that sharp upwards slope in the line at the end is going to cause future problems for some companies.

DKI Takeaway: When companies refinance later this year, it’s going to be at higher interest rates and earnings at those companies will come down. In some cases, we could see a reverse of the big stock buybacks we’ve seen in recent years. Neither scenario is positive for stock prices. If you want to hear more about Gayed’s thinking, I did an in-depth interview with him here.

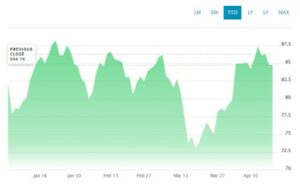

3) China GDP Growth Could Raise the Price of Oil:

China surprised with a higher than expected 4.5% GDP growth in the first quarter. While all economic statistics coming out of China should be treated with skepticism, there is a sense that the country is exiting its Covid shell and getting back to both work and spending. (DKI has also been continuously critical of inaccurate economic statistics in the US for more than a year.) One reason for the decline in the price of oil over the past year has been global fears of a recession. Growth in China would create incremental demand for oil which could cause prices to rise again.

Graph of Brent Crude prices this year comes from NASDAQ.

DKI Takeaway: Our philosophy at DKI is always to find ways to make money even from events which we may not like. While no one wants to pay higher gas prices, you might as well sell the gas to yourself and book the profits. DKI has a large energy portfolio that would benefit from higher oil prices available to subscribers.

4) LVS Earnings – Wow:

This one doesn’t fit the week’s disaster theme. Las Vegas Sands ($LVS) had a fantastic first quarter. Mass gaming in Singapore hit an all-time high, and occupancy at the Marina Bay Sands was 98% with room rates just under $600 a night. Property EBITDA there hit levels that would be considered a good quarter pre-pandemic. All this happened with Singapore air traffic 20% below 2019 levels. With the lifting of Covid-related travel restrictions, Macau is now solidly profitable. The world’s largest gaming market is almost to 50% of 2019 levels and that’s with one in three rooms out of service due to lack of staffing. LVS is going to need to start hiring and fast.

It’s morning again in Singapore

DKI Takeaway: We were early on this name, but have now received confirmation of our positive thesis. $LVS got the Macau re-tender approved in December, and gaming is rapidly approaching healthy profitable levels now that restrictions have been lifted. Want to know what we’re doing with the stock? The Current Recommendations page on the DKI site is available to subscribers.

5) Conflict Between the US Government and Taiwan Semiconductor:

Taiwan Semiconductor ($TSM) is the best chip manufacturer in the world. Given the amount of US military hardware that uses TSM chips, access to its products is a national security issue. With China making clear its intention to retake Taiwan and ramping up its military capability to do so, the US Government set aside about $50 billion dollars to incentivize companies to build fabrication plants in the US. The Wall Street Journal reports that Taiwan Semiconductor had planned to build 2 plants in the US for $40 billion and get about $8 billion of tax credits. That deal may now break due to the US asking for a share of “excess profits”.

Intel is great. Samsung is fantastic. Qualcomm for mobile. But TSMC is the best in the world right now.

DKI Takeaway: DKI has always stood for free markets and free people. However, the US gets most of its pharmaceuticals from China and its best semiconductors from a company that may soon be controlled by China. Having alternative sources is crucial especially since it seems that China is determined to take Taiwan and the US is determined to go to war to stop that. None of us want to be in a position where conflict with China stops the US from receiving legal pharmaceuticals and computer chips. I’m shocked to be saying this, but the US needs to make a deal to get a private company to invest here.

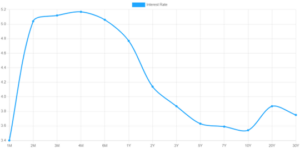

6) Treasury Market Pricing in Possible Default:

Every few years, the US approaches its debt limit. Since neither party is ever willing to consider spending less, we end up with regularly scheduled theater regarding raising the debt ceiling. Each political party blames the other. The President blames Congress which then blames the President. We have a vicious political fight until they get a deal done at the last minute. The overhang is that without a deal, eventually, the US Treasury will run out of accounting gimmicks, and the US would default on its debt. Now, take a look at this chart:

This is the US Treasury Yield Curve. Note the change from 1 month to 2 months.

The DKI Takeaway: The market is buying the 1-month Treasury down to a 3.4% yield and selling the 2-month Treasury up to a 5.0% yield. These debt ceiling fights are frequent and contentious, and the US has never defaulted. The most likely outcome here is a last-minute deal between Congress and the White House that ensures the overspending continues. But this is the disaster edition, and this is the big thing keeping people up at night now. If events cooperate, we’ll have a more positive “5 Things” for you next week.

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.