The Fed press release just came out. I’m getting you my quick bullet points now. Powell press conference in 15 minutes. I’ll update if he says anything that changes my conclusions.

– Fed lowers 25bp (.25%) as expected. This is what the market and DKI thought would happen.

– There was one dissent. Miran, the new addition by President Trump, wanted a 50bp reduction. Lisa Cook voted with the majority for the 25bp reduction.

– Press release cites downside risk to employment as the reason for the cut. This conclusion is reasonable given the data (to the extent that the data is accurate).

– The dot plot was 25bp more dovish. The June dot plot indicated a plurality of Fed Governors wanted to be between 3.75% – 4.00% by year end with a large number of Governors wanting no decreases. The current dot plot is 25bp more dovish – indicating a plurality of Fed Governors expect to reduce the fed funds rate by an additional 50bp from here. That would be a total of 75bp in cuts for the year including today’s cut. One dot was at 5 additional 25bp cuts (total of 6 including today). That was almost certainly Miran.

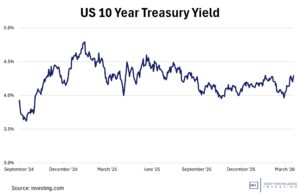

– Markets are down a little post announcement, but equity indexes tend to swing wildly up and down during Powell’s speeches and when he answers questions.

– GDP projections are up a tiny bit and PCE inflation expectations are unchanged.

All of this is consistent with market’s and DKI’s expectations. No change in outlook from this week’s big macro report which is available and not paywalled on the blog here.

Information contained in this report, and in each of its reports, is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied. DKI makes no representation as to the completeness, timeliness, accuracy or soundness of the information and opinions contained therein or regarding any results that may be obtained from their use. The information and opinions contained in this report and in each of our reports and all other DKI Services shall not obligate DKI to provide updated or similar information in the future, except to the extent it is required by law to do so.

The information we provide in this and in each of our reports, is publicly available. This report and each of our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion in this and in each of our reports are precisely that. Our opinions are subject to change, which DKI may not convey. DKI, affiliates of DKI or its principal or others associated with DKI may have, taken or sold, or may in the future take or sell positions in securities of companies about which we write, without disclosing any such transactions.

None of the information we provide or the opinions we express, including those in this report, or in any of our reports, are advice of any kind, including, without limitation, advice that investment in a company’s securities is prudent or suitable for any investor. In making any investment decision, each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable, based on this or any of its reports, or on any information or opinions DKI expresses or provides for any losses or damages of any kind or nature including, without limitation, costs, liabilities, trading losses, expenses (including, without limitation, attorneys’ fees), direct, indirect, punitive, incidental, special or consequential damages.