After a year-long travel adventure, I’ve returned from Tokyo to New York. I expect to be in the NYC/CT area for the next month or so. I intend to re-rent out my house and then depart for another year of living and working in different countries. This life suits me. I’ll publish an update at some point detailing where I’ve been and some of the incredible things I’ve seen and experienced. In the meantime, for those of you in the area who want to meet, please reach out while I’m here. IR@DeepKnowledgeInvesting.com.

It was another busy news week so we’re going with 6 Things again this edition. I wrote a piece on the DKI blog called the Strait of Hormuz Reverse Uno Card and then posted it to X where it went viral. Almost 600k views later, former White House officials liked it while the IRGC reposted it and called me a “retard”. OpenAI missed its revenue and user targets. The maker of ChatGPT is losing share, and has already cut its spending plans by around $800B. Further cuts are likely. Making things worse, OpenAI and Microsoft ended their exclusive agreement and Microsoft will no longer pay them a share of revenue. USA Rare Earth is acquiring Serra Verde Group. This gives the US a source of rare earth element supply and refining; an important step in decoupling from China. Google is investing between $10B and $40B in Anthropic. Anthropic is buying TPUs and services from Google. Looks like a good deal for Google, but we have concerns about these kinds of circular revenue deals. In this week’s educational topic, we explain the basics of leveraged buyouts. And yes, we do engage in appropriate criticism of PE firms that destroy the companies they acquire.

This week, we’ll address the following topics:

- My post on President Trump’s blockade goes viral and is re-posted by hedge fund managers, macro analysts, former White House officials, and the IRGC.

- OpenAI misses its revenue and user targets creating massive risk for the highly valued AI hardware makers that have entered into sales agreements with the company.

- Think things are bad for OpenAI? It gains the right to distribute ChatGPT on other cloud platforms while Microsoft no longer will pay a share of revenue to OpenAI.

- USA Rare Earth is acquiring Serra Verde Group for $2.8B. This should alleviate the need to rely on China for elements necessary for US weapons and auto manufacturing.

- Google is investing up to $40B in Anthropic at a $350B valuation. Anthropic is buying TPUs and services from Google. Yes – it’s another circular revenue deal.

- You’ve heard the term Leveraged Buyout (LBO). If you want to know what that is and how they work, check out this week’s educational topic.

DKI interns, Samaksh Jain, Kunal Arora, and Elijah Killorin do their usual fantastic job on this week’s 5 Things. All three of them have been incredibly helpful and reliable while I’ve been in challenging time zones. This week, we wish Samaksh well as he moves on to other opportunities. He’s been an outstanding contributor for the past year, and he leaves with our appreciation and a standing invitation to return. With Cashen and Samaksh gone, I have complete confidence that Kunal and Elijah will maintain the expected high standard.

Ready for a week of viral social media posts and name-calling? Let’s dive in:

1) Analyzing President Trump’s Blockade:

Last week, I wrote a post on the DKI blog, The Strait of Hormuz Reverse Uno Card, that I also posted to X. It went viral with over half a million views and re-posts from prominent hedge fund managers, macro analysts, former White House officials, and the IRGC who called me a “retard”. I will happily wear with pride the distain of the world’s leading State sponsor of terrorism. The post encourages analysis more thoughtful than “they’re stupid” when considering someone’s motives. In this case, many have criticized President Trump claiming he didn’t know Iran could and would close the Strait of Hormuz when attacked. I’ve known about Iran’s capability and intention to do this for decades, and can assure you that it was known to the White House and the President. Almost a quarter of a century ago, the US Navy conducted the Millennium Games which demonstrated US limitations in the area. The outcome of those games has been well-publicized. When Iran started letting oil tankers through the Strait for $2MM/ship, President Trump blockaded the Strait, eliminating that source of revenue for the IRGC. With Iranian oil storage filling, they will soon need to start spilling oil or to close the wells which can cause damage. Either way, President Trump has turned Iran’s biggest strategic advantage into a weakness.

The IRGC didn’t like my piece, yet they reposted it increasing its reach. Thanks!

DKI Takeaway: Besides the expected name-calling, there were some thoughtful objections. Some pointed out that instead of shutting the wells, Iran could start spilling oil into the Gulf creating an environmental disaster. In that situation, the US could start destroying Iran’s oil infrastructure. That’s something the military has avoided so far, but is being considered. Some claimed that a few ships have successfully evaded the Naval blockade. Others thought that closing producing wells wouldn’t cause permanent damage; but rather, just a temporary disruption with some cost to re-start production. While there was widespread disagreement on the last two points, even the best-case scenario for the Iranian regime wouldn’t solve their financial problem. They need police and the military to suppress the local population, and I question how many of them will take on that work without pay.

2) OpenAI Misses its Own Revenue and User Targets:

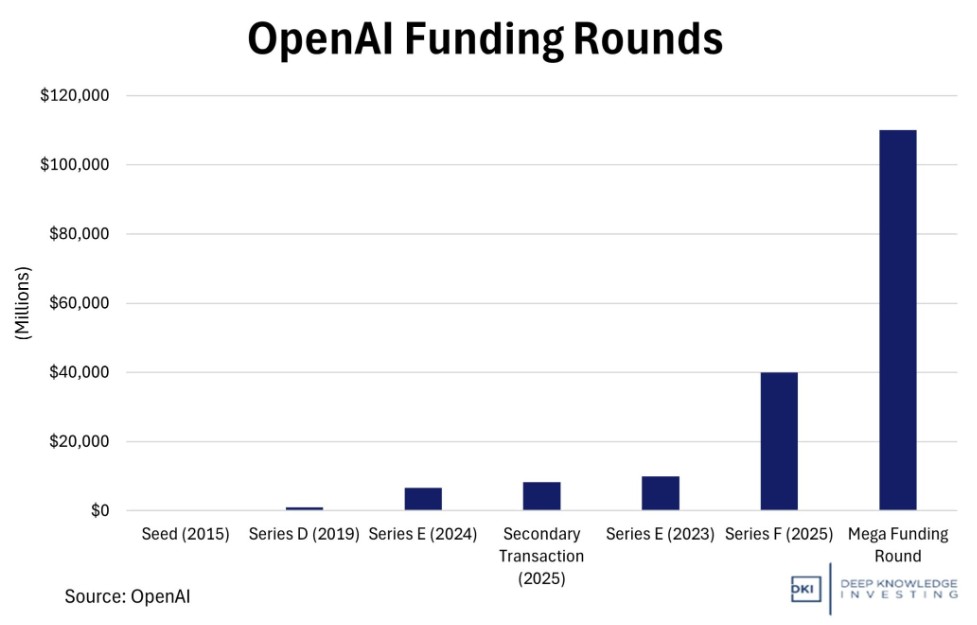

OpenAI missed its own internal targets for both revenue and user growth, raising questions about whether the company can support its massive infrastructure commitments. The company failed to reach its goal of one billion weekly active ChatGPT users by the end of 2025 and missed multiple monthly revenue targets earlier this year. Company execs have warned internally that if revenue doesn’t accelerate, the company may struggle to fund future data center contracts and about $600 billion in compute spending commitments through 2030. (Even this represents a huge decrease from the previous $1.4B target.) The competitive pressure compounds the problem as Google’s Gemini took consumer market share throughout 2025 while Anthropic’s gains in coding and enterprise pushed it past OpenAI in annualized revenue for the first time. To justify its $852 billion valuation from March’s record $122 billion funding round, OpenAI needs to reach its target of $280 billion in revenue by 2030, a more than 10x increase from where it sits today.

DKI has been warning about a cascading revenue miss for two years.

DKI Takeaway: DKI has spent the past two years warning that OpenAI didn’t have a revenue model that had any possibility of supporting its massive spending obligations. Even with spending plans slashed, the company will need a huge IPO to meet the scaled-back commitments, and the market may be less inclined to support this given the enormous coming offerings from Anthropic and SpaceX. This won’t be a problem just for OpenAI as reducing spending further will impact growth rates at some of the AI companies with the highest valuations. Oracle has already started building out capacity for the company and may be left with a bill, or have to sell that capacity at discounted rates in the future.

I’ve been using ChatGPT extensively for the past year, and think it’s terrible. It’s confidently inaccurate, offers to do things it’s not capable of doing, ignores parameters I’ve set multiple times, and regularly gives insulting and horribly racist responses. The LLM rose to prominence as the first big model that passed the Turing Test while delighting early users with funny pictures and poems. But it’s too inaccurate and unreliable to be useful for real work. The DKI interns are smarter, more reliable, and faster for some tasks like image editing.

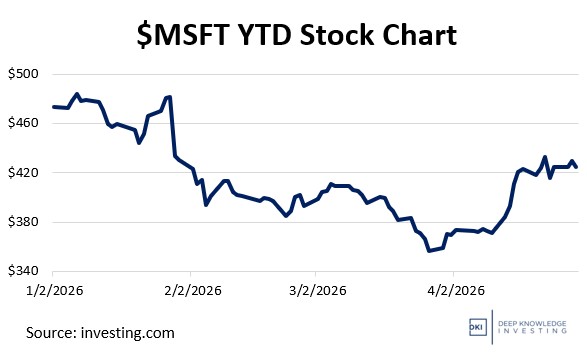

3) Microsoft and OpenAI Rewrite Partnership, Ending Exclusivity:

Microsoft and OpenAI announced a major revision to their long-term agreement, removing Microsoft’s exclusive rights to OpenAI’s models and allowing OpenAI to distribute its technology across competing cloud platforms, including Amazon Web Services and Google Cloud. Microsoft will retain a non-exclusive license to OpenAI’s models through 2032 and remain its primary cloud partner, but OpenAI now has full flexibility to pursue external partnerships and expand its enterprise distribution. The financial structure also shifted since Microsoft will no longer pay a share of revenue to OpenAI, while OpenAI will continue making capped payments to Microsoft through 2030. The changes follow rising tension between the companies, and reflects OpenAI’s push to position itself for future capital raises, while Microsoft continues to diversify its AI stack and reduce reliance on a single model provider.

The stock market did not care that OpenAI will put ChatGPT on other cloud providers.

DKI Takeaway: With this change, OpenAI gains distribution leverage and the ability to maximize demand across multiple ecosystems. If successful, it will lead to faster scaling and stronger pricing power over time. Microsoft gains margin control by eliminating outbound revenue sharing. This may improve profitability in products like Copilot, but $MSFT loses exclusivity over what used to be the premier LLM (large language model). The result is a more balanced but less defensible partnership. For investors, the key implication is that AI is moving toward a multi-model, multi-platform market structure, where no single player controls both distribution and model access. That raises pressure on software incumbents to build proprietary capabilities or risk margin compression as model providers expand across competing platforms.

Multiple research calls by DKI have indicated that industry execs view the reliance on ChatGPT as a negative for Microsoft’s Copilot. The combination piled corporate guardrails on top of corporate guardrails resulting in a product so neutered that many didn’t find it useful. There’s a reason share is shifting to other models and that Copilot is used by only a fraction of those who have access to it.

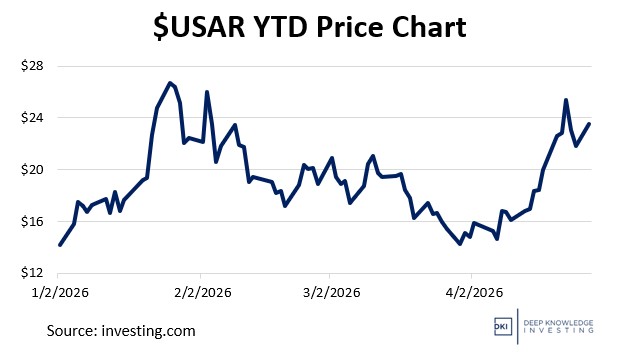

4) USA Rare Earth to Acquire Serra Verde Group for $2.8B:

USA Rare Earth announced a $2.8B agreement to acquire Serra Verde Group, the owner of a Pela Ema rare earth mine and processing plant in Brazil. The deal will consist of $300MM in cash and 126 million shares of $USAR common stock. The Pela Ema mine is the only producer outside Asia capable of supplying all four magnetic rare earth minerals at scale. The acquisition is expected to deliver $550MM – $650MM in additional EBITDA by 2027 with a total of $1.8B projected by 2030.

With the US eager for non-Chinese sources, there will be a buyer for product.

DKI Takeaway: Ever since China cut off some of its mineral exports for foreign use, the rest of the world has been scrambling to find a solution. Since China has 90% of the world’s processing capacity, as well as some of the best refining technology, it has forced companies and governments to adapt and find their own ways of processing rare earth elements. This acquisition helps to combat the problem by providing USA Rare Earth access to a mine containing all four magnetic rare earths as well as adding more processing capacity. It makes the combined entity the leading global rare earth platform due to full supply chain control and operating capacity. The combined company will have mining, processing, separating, and manufacturing expertise in an area vital to national security. There is also a 15-year agreement with a US government special purpose vehicle which creates explicit price floors for all four elements. The deal establishes Western capability to compete against China’s rare earth dominance, something necessary to avoid relying on Chinese suppliers for US weapons and auto manufacturing.

5) Google to Invest up to $40B in Anthropic:

Google has pledged to invest up to $40B in Anthropic, the maker of the Claude LLM. The initial investment will be $10B with an additional $30B available based on performance milestones. The deal implies a $350B valuation for Anthropic. Given the likely size of coming AI IPOs, that might be below expectations. Google is providing Anthropic with 5-gigawatts of power and access to one million TPUs (Tensor Processing Units). With the Claude Code agent gaining share, Anthropic just achieved a $30 billion revenue run-rate. While all the details are not available right now, this looks like another circular revenue deal where Google invests in Anthropic and Anthropic buys chips and services from Google.

Looks like a good deal for Google.

DKI Takeaway: This deal highlights how much of a necessity infrastructure is in the AI race. Google is able to capitalize on this by locking Anthropic into its hardware including its own proprietary silicon. By making its infrastructure the backbone for Claude, Google can benefit from both Anthropic’s success as well as that of its own Gemini LLM. So far, the big money-makers in the AI space have been hardware makers like Nvidia. It will be interesting to see which LLM, if any, becomes profitable first.

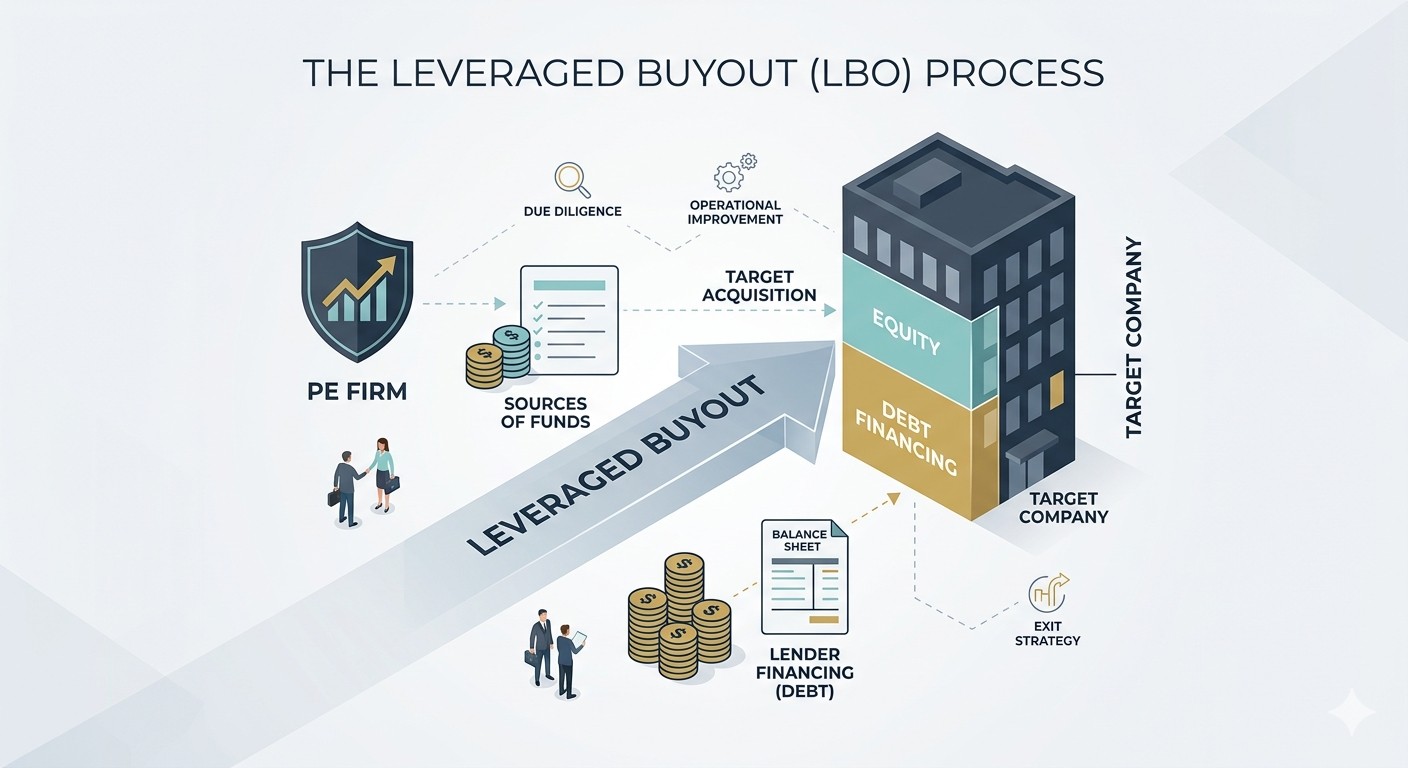

6) Educational Topic: Leveraged Buyouts:

A Leveraged Buyout (LBO) is when an entity, like a Private Equity (PE) firm, acquires a company using a large amount of leverage (debt). This debt accounts for most of the purchase price with the remaining balance covered by equity or cash provided by the acquiror. During the hold period, often five to seven years, the firm focuses on aggressive improvements (like cost cutting, revenue expansion, etc.) in an effort to increase the EBITDA of the acquired company. This allows the PE firm to reduce debt, pay itself large fees, and improve the future sale price of the company. The strategy succeeds when a combination of both EBITDA growth and deleveraging is used. As debt is reduced, a greater percentage of the value of the company accrues to the equity of the PE firm.

This would be the “good” version.

DKI Takeaway: The real benefit of an LBO is in the use of the acquired company’s own profit to fund a transformation where it pays for its own acquisition. For the investor, the key is that you don’t need the company’s total value to triple to see a tripled return on the equity investment. By the time the PE firm exits, the combination of a higher EBITDA multiple and a much smaller debt load can create a larger return. In recent years, there has been valid criticism of the model. It’s increasingly common for PE firms to pay themselves huge fees, reduce the quality of products and services, and to keep reducing equity by taking on higher debt loads. Too many recent LBOs have resulted in profits to the PE firm as well as the eventual bankruptcy of the acquired company.

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.