The incredible volatility in gold, silver, and Bitcoin continued for most of this week. We give you a quick update along with links for those of you who want a better understanding of what’s really happening. Anthropic announces that its Claude AI can take over functions currently being handled by expensive monthly software subscriptions. SaaS stocks shed $300B in valuation in a day. The lesson: Monopoly business practices are great until you can be replaced. Then, you might wish you had treated your customers better. SpaceX buys xAI. Elon Musk wants to build datacenters in space and deliver the components himself. I wouldn’t bet against him. Undaunted by not earning a return on hundreds of billions of dollars of AI-related cap-x, Google and Amazon are targeting nearly half a trillion dollars of spending in 2026 alone. Here at DKI, we’ve spent years explaining the CPI (consumer price index) to readers and have focused on how it systematically understates inflation. The big metrics are all-items and Core. If you’ve ever wondered what those are and why people care, read on. We explain in simple language.

This week, we’ll address the following topics:

- Volatility continues in gold, silver, and Bitcoin. We explain and provide links. Let me know if you agree or disagree. Either way, you’ll understand the issue better.

- AI threatens the SaaS business and the stock market shaves $300B off of valuations in a day. Customers want an exit to abusive business models.

- SpaceX buys xAI. Elon Musk is envisioning solar powered AI datacenters in space. Does anyone want to bet against him?

- Google and Amazon announce plans to increase capital expenditures, but it’s still not clear how they get users to pay enough to justify the spending.

- Ever wonder what the difference is between the all-items CPI and the Core CPI? Check out our educational topic where we explain.

I’d like to relay to you what it’s like working with DKI’s young interns. Cashen Crowe flew to Charlotte, landed a fantastic internship offer for the summer of ’27, was delayed on the way back due to a flat tire, and still delivered a well-organized version of this week’s 5 Things. Samaksh Jain was also an excellent contributor to this piece and is working with me on some complicated financial analysis. He let me know he had exams and would be able to deliver in two days. These young men have an incredible work ethic, strong intellectual capacity, and admirable attitudes. I’m proud of both of them (and of the former DKI interns who graduated and are off to excellent starts to their careers).

Ready for another week of AI and Federal Reserve-related volatility? Let’s dive in:

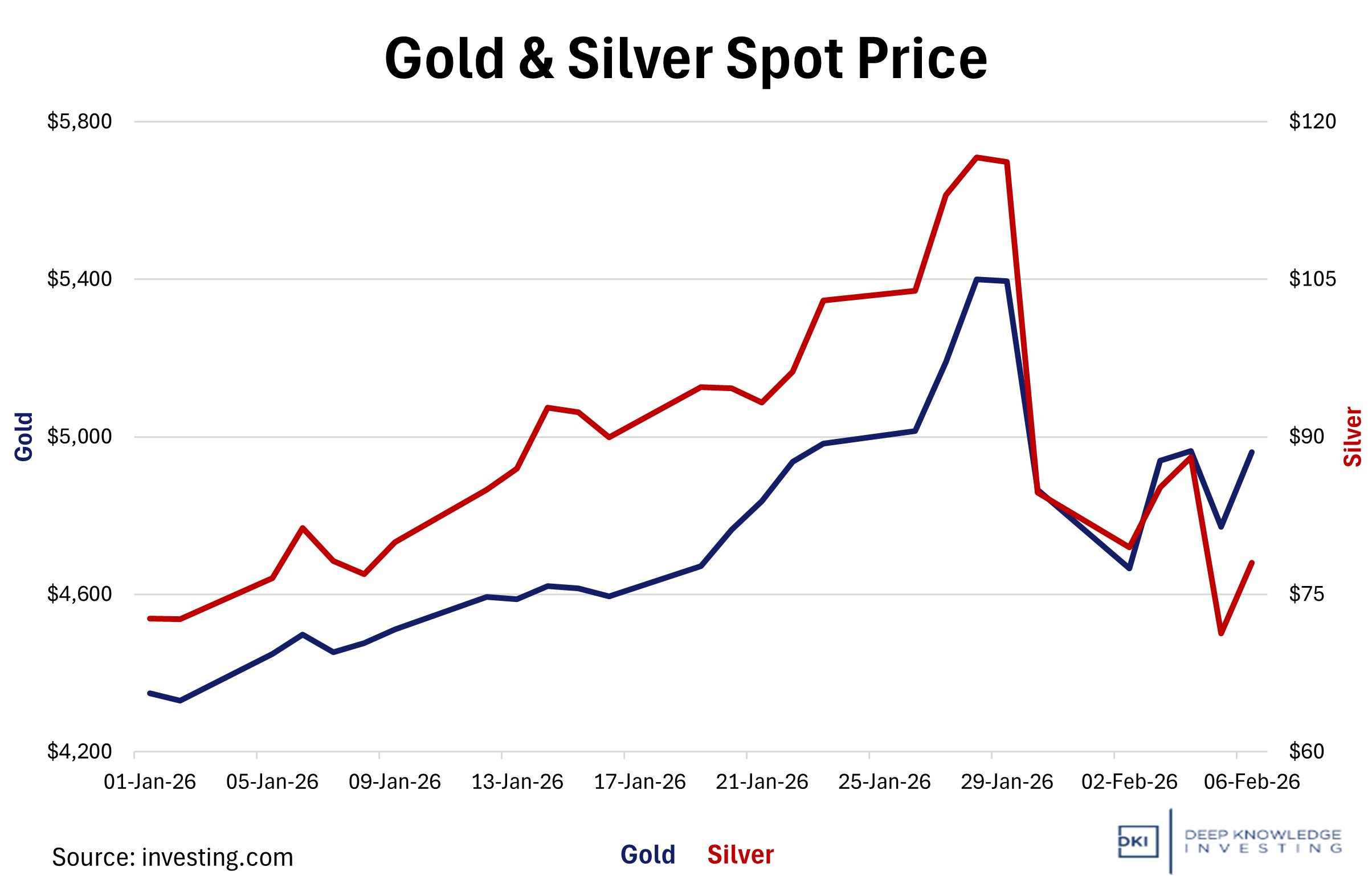

1) Gold, Silver, and Bitcoin Volatility Continues:

Let’s start with what I think happened. Zero-yield hard assets like gold, silver, and Bitcoin started declining a week ago right as President Trump announced Kevin Warsh as the nominee to succeed Jerome Powel as Fed Chairman. The market believed Warsh would favor higher interest rates so bought dollars and sold the zero yield assets which became relatively less attractive. That selling led to margin calls on leveraged accounts, a trend that was exacerbated in the silver market where the main US exchange raised margin requirements. Margin calls lead to non-discretionary selling where market participants need to reduce risk and to raise cash regardless of whether they’d like to buy or sell at the current price. That forced selling drove prices lower which led to another round of deleveraging. This is what George Soros called reflexivity which is the tendency of financial markets to amplify existing trends. Was this the right call?

Are gold and silver really down? Zoom out just a bit and you can see both are up YTD.

DKI Takeaway: First, I disagree that Warsh is a hawk (one who favors higher rates). He’s said publicly that he wants lower rates and this week, President Trump told NBC News that he made the nomination because Warsh said in private that he favors lower rates. This was something I suggested in last week’s 5 Things. Second, the Federal Reserve can want lower long-term rates, but until Congress stops overspending by trillions of dollars a year, the debasement trade will continue. (This is also why I’m unconcerned about potential QT. It can absorb a maximum of one year’s currency creation due to overspending.) Finally, Warsh has only one vote on the Federal Reserve Open Market Committee. Even if he were a hawk, he can’t outvote a dovish group of Governors. Some have pointed to his desire to reduce the size of the Fed balance sheet as something that could crash markets, but Powell’s Fed has reduced the balance sheet by trillions over the past couple of years when the stock market, precious metals, and Bitcoin rose in price (mostly). I think the market has this one wrong. For more detailed analysis on the subject please see these non-paywalled posts: Thoughts on Bitcoin, Looking at the Downside, and Here’s What Just Happened in Gold, Silver, and Bitcoin. You might agree or disagree, but I promise you’ll understand the volatile situation better. Think I got something wrong? Reach out at IR@DeepKnowledgeInvesting.com and let me know.

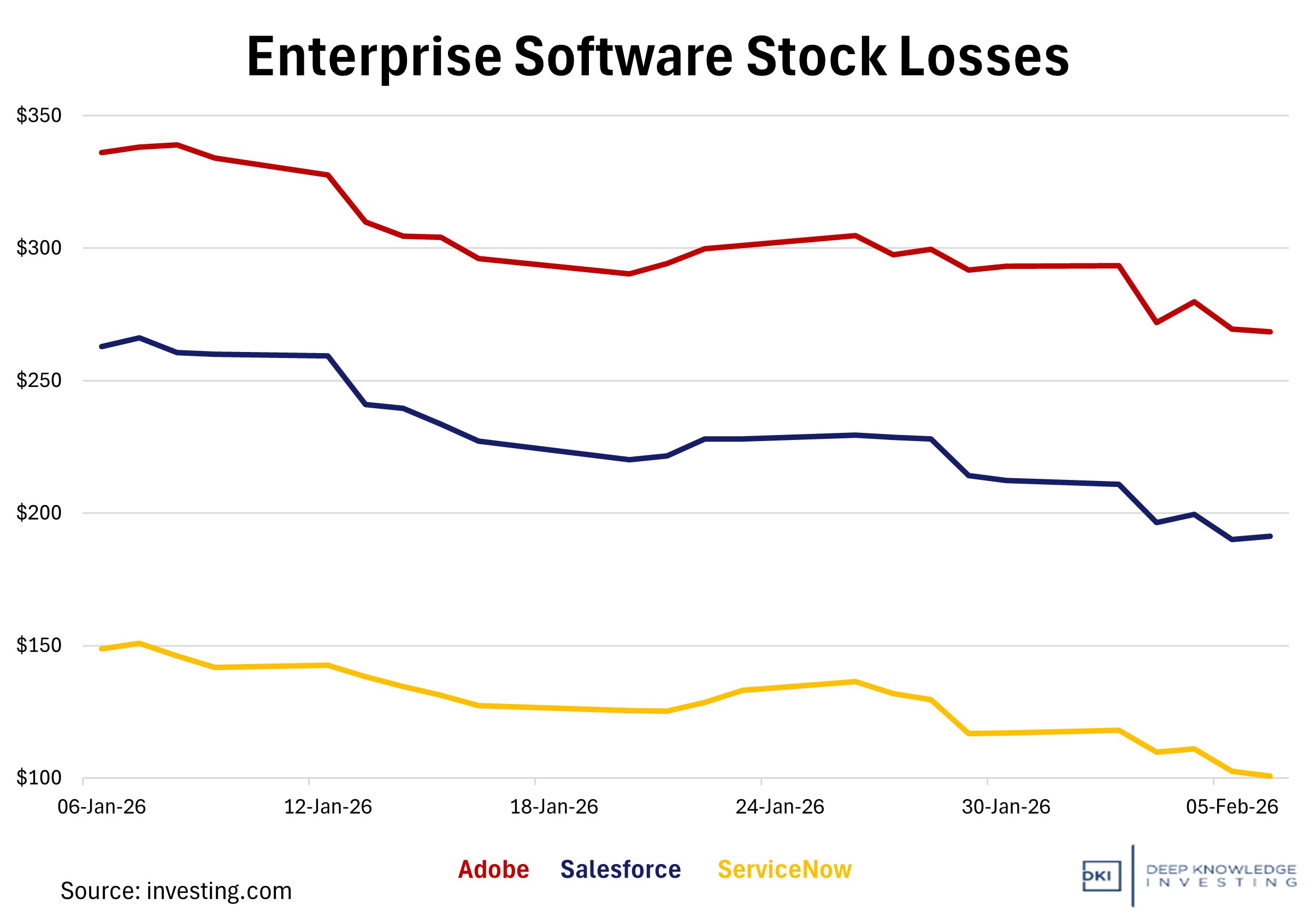

2) Software Stocks Shed Roughly $300 B in One Day on AI Disruption Fears:

On Tuesday, US equity markets experienced a sharp sell-off, with roughly $300 billion in market value evaporating from software and data stocks. Investors repriced risk amid intensifying fears that AI will disrupt traditional software business models. New capabilities rolled out by Anthropic’s Claude model caused the sell-off in stocks including Salesforce, Adobe, SAP, ServiceNow, Intuit, and other enterprise SaaS providers. The fear is that Claude could reduce demand for legacy software licenses and weaken long-term growth trajectories. The S&P 500 software and services index fell 3.8%, extending a broader tech pullback, while the tech-heavy Nasdaq Composite also slid sharply as risk-off sentiment spread. Analysts pointed to valuation compression, worries about subscription erosion, and the fear that AI could supplant large swaths of software workflows as catalysts driving the sell-off. Traders also rotated into value and defensive sectors, reflecting an abrupt shift in investor psychology from unbridled AI optimism to reassessment of durable revenue streams.

Fear that AI will change the SaaS model arrived before last week.

DKI Takeaway: This sell-off represents a major recalibration in how markets are pricing AI’s impact: from boosterism that viewed future disruption as inevitable to a more skeptical view that AI could destroy recurring-revenue moats rather than merely augment them. That doesn’t mean the software sector is obsolete; rather, it underscores that AI is evolving from a productivity enhancer into a structural substitute for traditional software functions in areas such as CRM, legal automation, and financial operations. Some of these companies are also at risk due to business models that eroded trust with their fans and customers. Adobe went from software that could be purchased for a reasonable price and owned for a lifetime to subscription models with high recurring fees. There’s an old expression that on Wall Street that bulls make money, bears make money, pigs get slaughtered. It’s easier for customers to opt out of paying a high monthly fee than to exit legacy software that’s already owned.

3) SpaceX Acquires xAI to Create Vertically Integrated AI and Space Powerhouse:

SpaceX announced on February 2, 2026, that it had acquired Elon Musk’s artificial-intelligence startup xAI in a blockbuster merger that values the combined company at approximately $1.25 trillion, roughly $1 trillion for SpaceX and $250 billion for xAI. Under the terms, xAI shareholders will receive SpaceX stock in exchange for their xAI shares, with some executives having the option to take cash instead. The combined entity, bringing together SpaceX’s launch and Starlink network with xAI’s AI models, such as Grok, and the social platform X, is being positioned as a vertically integrated engine for aerospace, connectivity, AI development, and future compute infrastructure. Musk has publicly framed the move as part of a long-term push to build orbital data centers powered by solar energy and launched via Starship rockets, aiming to solve terrestrial power and cooling constraints for advanced AI compute. The deal also edges SpaceX closer to a planned IPO potentially later in 2026, with valuations discussed above $1.5 trillion in some scenarios and index-inclusion efforts already underway.

Musk may be turning 2001, A Space Odyssey into reality. Or possibly Space Invaders.

DKI Takeaway: SpaceX’s acquisition of xAI is more than headline-grabbing M&A; it’s a structural play that internalizes both compute demand and the means to deliver it. By folding an AI developer into a launch-and-infrastructure platform, Musk is signaling a belief that future AI scaling will be constrained not by models but by power, cooling, and physical compute capacity, challenges where he believes space offers a solution. This reinforces an emerging theme we saw last year with OpenAI’s AMD deal: AI circularity, where companies invest in their own supply chains, is deepening, and that deepening increases systemic risk if internal demand replaces open-market validation. If AI datacenters move to space where cooling isn’t required and solar energy runs the GPUs, that would alleviate a lot of terrestrial power demand and reduce one of the claimed threats against Bitcoin.

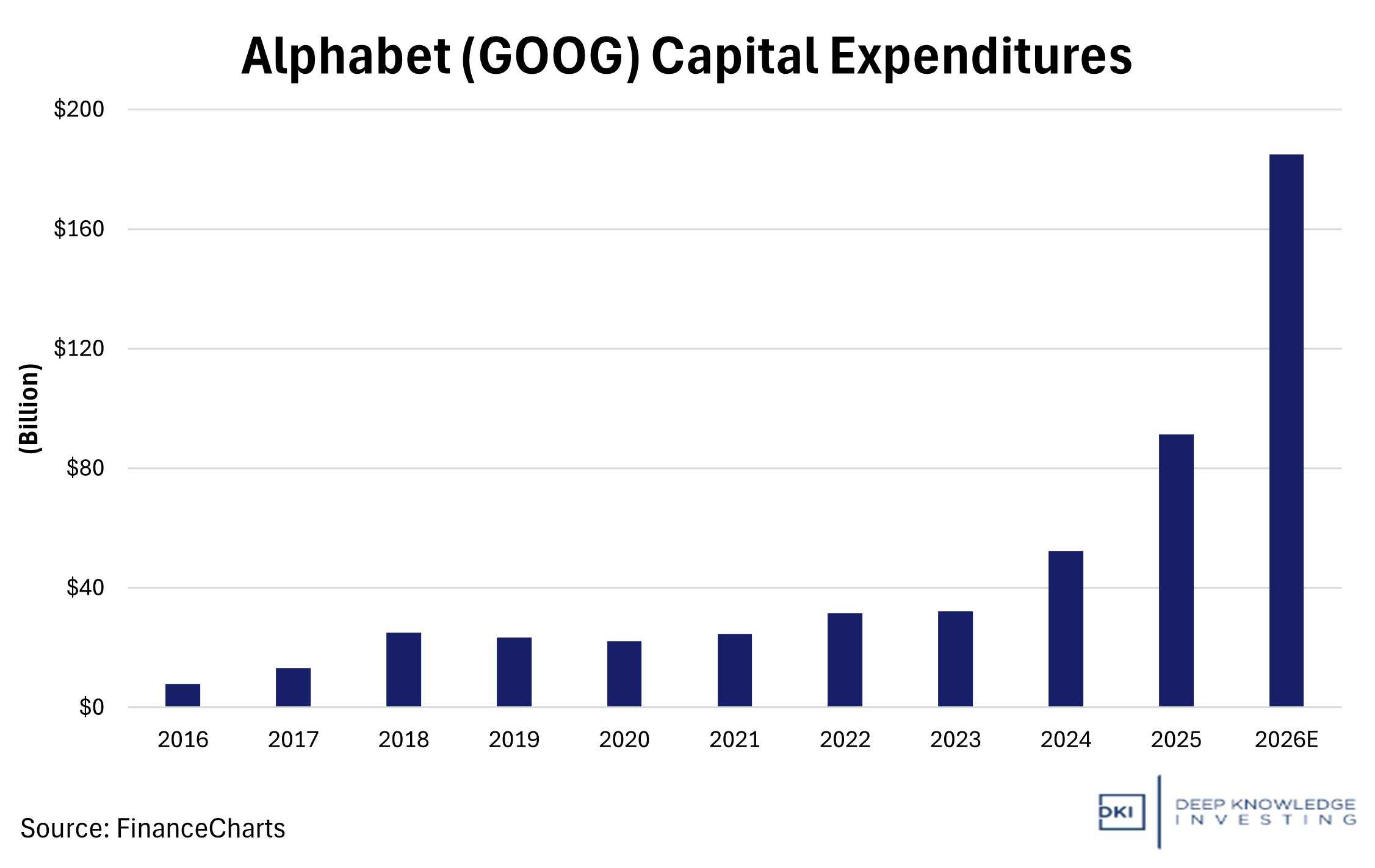

4) Alphabet’s Plan to Nearly Double Capex in 2026:

In Alphabet’s (Google) February 4th earnings update, they guided to $175-$185 billion of capital expenditures in 2026. This is roughly double the $91.4 billion it spent in 2025. At a moment when investors are scrutinizing whether AI infrastructure spending will earn attractive returns, Alphabet’s plan creates concern. They even mentioned that the planed capex expansion will reduce company profitability. Not to be outdone, Amazon announced plans to increase cap-x from $132 billion to $200 billion.

Do they have a plan to earn a return on this spending?

DKI Takeaway: There is evidence that AI workloads are translating into cloud demand: Alphabet’s revenue grew 48% YoY and its cloud backlog reached $240 billion. Alphabet also said that just over half of 2026 machine-learning compute is expected to go to cloud, signaling a shift towards the idea that AI infrastructure build out is being prioritized for external monetization instead of only internal R&D. For the past couple of years, we’ve been wondering how these companies would earn a return on the hundreds of billions of dollars they’re spending on AI. As of now, no one has a business model that’s working and consumers are showing a willingness to shift models as capabilities change. These companies need to keep spending to avoid falling behind, but still have to figure out how to get users to pay for that spending.

5) Educational Topic: Core vs. Headline Inflation:

Headline inflation and core inflation are two closely related measures of price growth in the economy, but they differ in what they include and how they are used to interpret economic conditions. Headline inflation measures the total change in prices across the entire consumer basket. It captures all categories, including food and energy. This is the most cited figure in news releases because it reflects the full cost of living. (Or at least the government’s report on the cost of living. Your mileage will vary.) In contrast, Core inflation excludes food and energy prices. These two components tend to be highly volatile due to short term factors and thus are removed to provide a clearer view of persistent, underlying inflation trends.

These distinctions matter because policymakers and investors both are trying to determine whether inflation pressures are temporary or structural. Central banks such as the Fed place significant weight on core measures when setting monetary policy, and if headline inflation rises due to a short-lived surge in energy prices, policymakers may look through the increase.

Your comprehensive list of approved inflation indexes.

DKI Takeaway: Some are even trying to tout a new measure called super core which excludes food, energy, and shelter. I’m not a fan of all of these additional measures. People have to spend money each month at the grocery store, for utilities and gas, and for housing. Not only is the consumer price index dishonest and inaccurate, these alternative measures just create noise. Remember that if you exclude all items, you end up with an inflation rate that’s consistently zero.

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.