It’s been a volatile few days. Let’s recap:

The Federal Reserve:

I continue to believe the market is overestimating the impact Fed Chair nominee, Warsh, could have on the economy and the markets. Last week, there was reasonable fear that Warsh would be hawkish (favoring higher interest rates). I’m skeptical of that take, despite the fact that it’s been the dominant market narrative since last Thursday.

First, Warsh isn’t the ultra-hawk many portfolio managers fear. He’s said publicly that he’s in favor of lower rates. I’m also certain he’s relayed that intention in private. He had a meeting with President Trump, who is in favor of much lower rates. There’s no possible way he relayed an intention to raise the fed funds rate to the President and still got the nomination. That tells me his public and private remarks are consistent with each other. Yet, the market is assuming he’s going to act in contradiction to his publicly (and extremely likely privately) stated remarks.

Second, if confirmed, Warsh would be the Chairman of the Federal Reserve and be a voting member of the Open Market Committee. That’s the same group of people who have voted for 175bp of cuts to the fed funds rate over the past 16 months despite inflation that’s both understated and above the 2% target. Even if Warsh favored rate hikes, he can’t outvote the entire committee. I can’t remember a situation where a dissenting vote was cast by a Chairman, but given that many of the Fed Governors are political operators acting in a political institution, that’s a possible outcome. (I’ve written out lists of political interference at the Fed going back more than 100 years. It’s never been independent.) I don’t think Warsh is a hawk, but even if he were, he can’t outvote everyone on his own.

Third, there’s a lot of fear regarding Warsh’s belief that the Fed balance sheet is too large. I agree with him and think the Fed should reduce the balance sheet now. But even if they were to do that in 1-2 years, it would pull a maximum of $3T or so out of the system. Congress is overspending by $3T – $4T a year, and that’s just on balance sheet. Add in the off-balance sheet liabilities, and that figure goes even higher. So, even if Warsh sells assets, the best he can do at this point is neutralize one year of Congressional overspending. Long-term, the debasement of the currency will continue.

Finally, there’s a limit to how much the Fed can accomplish. Right now, long-term yields are not responding positively to reductions in the fed funds rate. That’s because bond market participants know that a permissive Fed plus Congressional overspending means future inflation. That’s not going to stop. Current Chairman, Powell, keeps saying policy is restrictive, but the real rate (fed funds less the CPI) has been consistently under 2% and that’s with an understated CPI. Policy is not restrictive.

Your TL;DR version: Warsh isn’t a hawk, and even if he were, he’s not going to be able to lower long-term rates.

Gold and Silver:

Gold and silver had a great January even including the price collapse at the end of the month. Prices have also bounced hard off the bottom which occurred about 24 hours ago. There’s been a lot of talk about Chinese manipulation of the market causing prices to fall. I’m skeptical about that. The only way it could happen (or at least the only way I can see it) is if Chinese buyers sold paper metal in the west or sold actual bullion. I don’t see how that could help them. We’re seeing a $20 – $50 premium per ounce of silver in China over US prices depending on the day. The US still has a large paper market. In China, they want to take physical delivery. That demand is unchanged and Chinese buyers are and will pay a big premium to ensure supply.

There have also been rumors that the recent price decreases related to market manipulation here in the US. I find those rumors to be more credible. I’ve read that because customers wanted exposure to metals, large US banks wrote contracts to sell to their customers. This paper silver (payment could be received in fiat rather than metal) was leveraged as well. When silver rose past $120, these banks were sitting on massive losses. To help them, the exchanges raised margin requirements which forced leveraged players to sell paper silver to raise cash in order to meet the new requirements. That forced selling pressured prices down which caused another reflexive round of margin-based selling. Once the price dropped into the $70s, the banks were able to exit without business-crushing losses. (At least that’s the story. I don’t have insight into the inner workings of the metals exchanges, or the risk-control departments at the big banks.)

I find this explanation to be more credible. The paper market is huge and big banks that had served as counter-parties to offset client risk had an incentive to see prices drop. They had already sold and needed to buy back those assets. I don’t think the Fed had a way to move the price of precious metals right now, and I don’t think Chinese buyers had a mechanism to lower prices for themselves. Higher margin requirements to save the banks does fit both incentives and actions.

Despite all of that, I don’t see any change to the drivers of metals prices. Central banks (China and India in particular) are still buying tons of physical gold at any price in order to reduce reliance on the dollar. China is debasing its own currency, but has been smart enough to use some of that depreciating fiat to buy hard assets like gold. I just read that the deficit of silver production to use over the past five years has been a billion ounces. Silver is desirable not just as a store of value; but also, for production of renewable energy components, semiconductor manufacturing, and weapons manufacturing. That demand is increasing, and unlike the gigantic paper silver market, needs to be supplied with actual metal from now-empty stockpiles.

Your TL;DR version: Gold and silver prices are down for the past few days, but long-term demand drivers are unchanged.

OpenAI, Oracle, Nvidia, and AI:

There’s been increasing attention on OpenAI’s attempts to raise capital and comments from Nvidia that it might not put up the $100B it previously said it was going to invest. Let’s unpack the implications.

First, the $100B deal looked a lot like the Cisco financing deals from the dot com boom a quarter of a century ago. Nvidia was going to provide OpenAI with a huge amount of money that OpenAI would use to buy Nvidia AI accelerators. Nvidia was effectively going to record revenue with its own money. While legal, these kinds of deals reasonably cause concern.

Second, OpenAI has made $1.4T of purchase commitments and doesn’t even have enough cash on hand to fund its projection of more than $100B of operating losses over the next few years. Without a massive infusion of capital much greater than the size of any discussed IPO, OpenAI either needs to suddenly find a very profitable business model, or it will have to default on commitments. In that event, Oracle is going to be on the hook for the cost of massive data centers its already building, and Nvidia is going to see a slowing revenue growth rate. These will cause revisions to multiples in the semiconductor space and will take down even uninvolved stocks like Intel and AMD. This real risk is one reason I’m still carrying a material market hedge despite an overspending Congress and an accommodative Federal Reserve.

Laptop Prices:

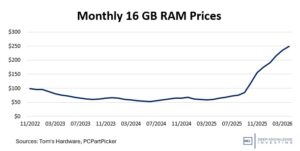

There has been a concern that higher DRAM prices will lead to increases in laptop and desktop prices which will lead to higher consumer prices. In turn, this could cause consumers to hold on to their existing technology longer and delay upgrading. That’s not good for Intel’s consumer division which needs new computer sales to move their Core I and Core Ultra lines of CPUs.

Just a couple of weeks ago, I reported that I was seeing no change in actual laptop prices. At the end of last week, I decided to buy a high-end Lenovo laptop with an Intel Core Ultra 7 processor, 32GB of RAM, and an Nvidia 5060 GPU on sale for $1,300. That laptop had previously been priced at $1,800. Best Buy showed it out of stock for a few days and it’s now available for purchase again at an increased price of $1,900. A comparable unit with a Core Ultra 9 processor and an Nvidia 5070ti GPU had been selling for $1,800 last week. It’s now listed for just under $2,400. Prices have risen significantly in just the past week.

These supply issues always get resolved with increases in production, but that’s going to take some time. Expect higher consumer prices at least for the next few quarters. People who need new computers will still need them and not everyone will be able to wait. Some will pay higher prices while others look for units with reduced specs. If they downgrade the CPU, that’s a negative for Intel. If they simply stick with the units that have just 16GB of RAM, that’s not going to be as bad for the chipmakers. Fortunately, Intel already gave weak 1Q guidance not because of a lack of demand; but rather, due to difficulty sourcing components. Difficulty sourcing components is another way of saying component prices are rising due to high demand. This issue has been reflected in the stock price already.

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.