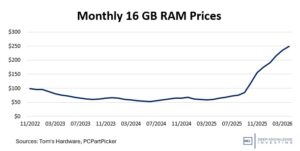

The December CPI was announced yesterday. Normally, I do an immediate detailed analysis. That made sense when wildly fluctuating inflation metrics had a real impact on what the Fed was going to do. I see the data as less valuable and timely right now. The December CPI was 2.7% with the Core CPI at 2.6%. These were roughly in line with expectations and have meant the CPI has been locked in the mid/high 2% range for months (mostly). Despite this continued elevated level of official inflation, the Fed has cut 175bp. Despite the cuts to the fed funds rate, the yield on the 10-year Treasury has risen, something DKI warned about before the Fed started its cutting cycle in September of 2024. A few notes on the report:

Food inflation has risen to 3.1% with the monthly change a huge 0.7%. DKI has been warning about unrealistically-low food inflation for years.

Despite higher electric prices partly driven by data center demand, the energy portion of the CPI was up only 2.3%. That’s due to lower gasoline prices.

Vehicle prices were barely above flat. In general, goods prices have not risen, and I have not seen the mea culpas from the fiat economists who predicted tariff Armageddon nine months ago.

To his credit, Wolf Richter pointed out some egregious anomalies in the shelter and health insurance data. Shelter prices were officially up 3.2%, but he notes a huge unexplained dip a few months ago that got carried forward a month due to the government shutdown. OER (owners equivalent rent) means that the shelter portion of the CPI is always understated, and I agree with Wolf that the current version is likely understating housing costs by even more than usual.

A few years ago, I wrote about the massive downward revision in the health insurance index. Wolf illustrates the insane level of the current adjustment. According to the Bureau of Labor Statistics, health insurance is now more than 30% LESS expensive than it was in September of 2022 and at the same level it was at in February of 2019. Do any of you believe that insurance costs haven’t risen in the past seven years?! I don’t either.

Conclusion: The CPI remains elevated over the 2% target (which is 2% too high). The Fed doesn’t care and neither the White House nor Congress understands. In addition, the CPI “data” seems more skewed than usual and the prices actually being paid by American consumers probably reflect a much higher inflation rate.

One final note: During the previous White House Administration, I frequently noted that employment and CPI reports seemed designed to help the Democrats in power at the time. Over the past year, we have seen similar patterns of bad employment data and an understated CPI continuing during the Trump Administration. I retract my previous claim that the bureaucracy was favoring team blue over team red. I now just think they’re bad at their jobs and have neither the inclination nor the capacity to produce accurate data.

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.