IBM pays $11B for Confluent and brings its real-time data streaming in-house. They’re aiming to integrate the AI cloud ecosystem across devices. Nvidia thinks it has a way to turn AI datacenters from something that stresses the grid to something that stabilizes it. This is the solution we’ve seen from many Bitcoin miners. Let’s hope it works. DoorDash is expanding its apparel options. The biggest shopping days of the year are just before big holidays so they’re betting there’s a market for same-day delivery. Private credit gates are closing and investor redemptions are being partially filled. Marketers highlighted the low volatility of these investments. DKI points out that not marking the book to market doesn’t reduce volatility; just the perception of it. OpenAI offers PE firms a financial incentive to use its AI solutions across portfolio companies. We note that the product has been failing, is plagued by inaccurate and inappropriate results, and doesn’t have a business model to earn a return on massive investments. In this week’s educational topic, we explain what ROE is, why some use it, and why I don’t.

This week, we’ll address the following topics:

- IBM pays $11B for Confluent. They’re bringing real-time data streaming across platforms in-house. The idea is to integrate the AI cloud ecosystem.

- Nvidia collaborates with multiple power producers to transform AI datacenters from something that stresses the grid to a stabilizing force. This is the Bitcoin miner play.

- DoorDash is expanding its apparel options. Seems crazy until you notice that all big shopping days are just before holidays and people want help – not a trip to the mall.

- Private credit gates are coming down as investors who want redemptions are rejected. DKI warns that not marking the book to market isn’t the same as low vol.

- OpenAI offers PE firms a financial incentive to use its AI solutions in portfolio companies. Still no viable business model out of the money-losing LLM parent.

- Ever wonder what return on equity (ROE) is and why it matters? Check out this week’s educational topic and we’ll explain.

DKI’s star interns, Cashen Crowe, Samaksh Jain, and Kunal Arora deliver again. They pitched all the ideas for this week’s 5 Things, prepared the images, and did the heavy lifting on the research and writing. Really impressive work for anyone let alone college underclassmen.

Ready for another week of balancing the electric grid? Let’s dive in:

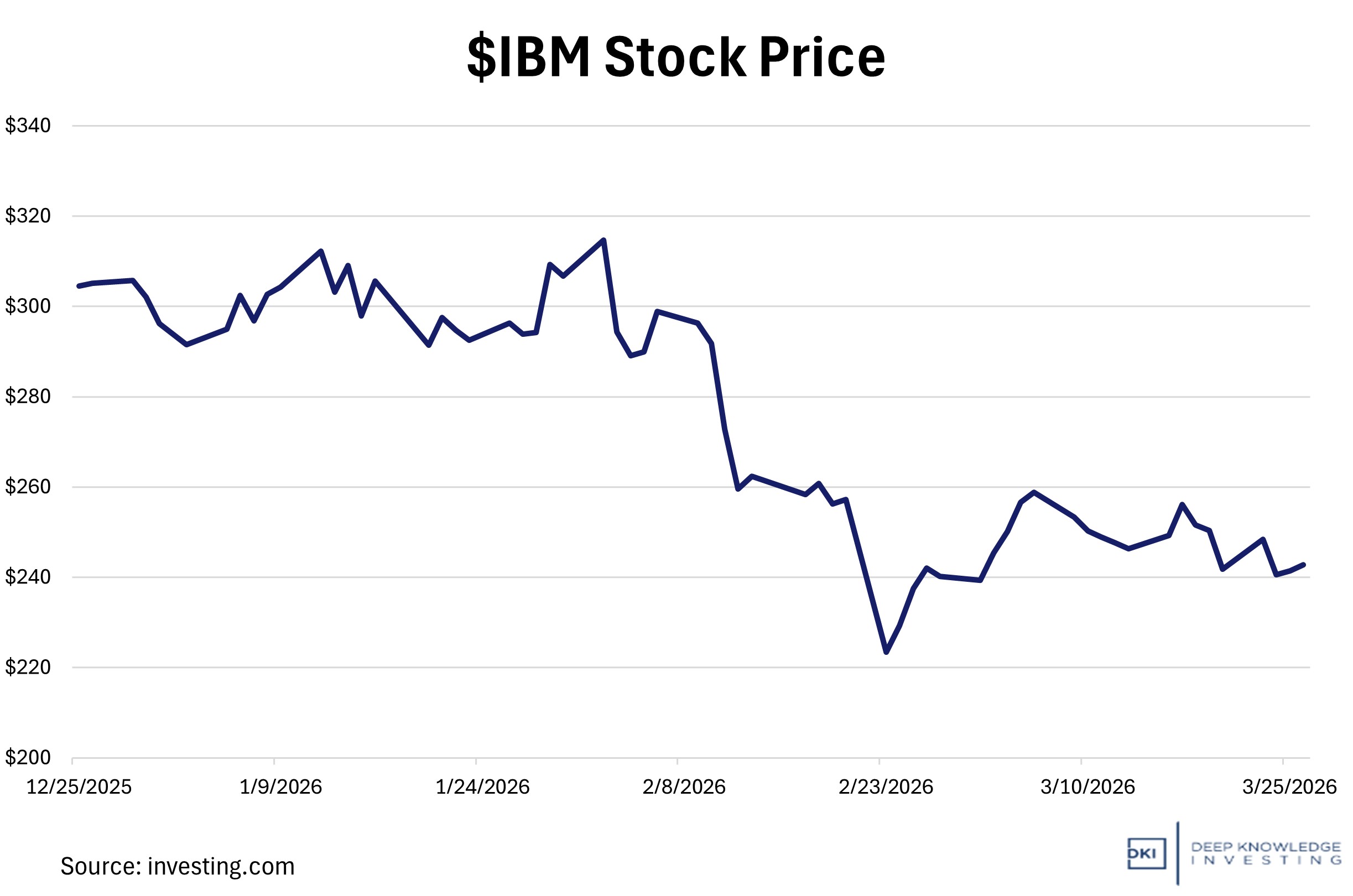

1) IBM Completes $11B Acquisition of Confluent to Strengthen Data Infrastructure:

IBM completed an $11B all-cash acquisition of Confluent which enables enterprises to move and process data continuously across applications, systems, and cloud environments. This brings IBM’s real-time data streaming platform fully in-house. IBM has plans to integrate Confluent into its broader AI and hybrid cloud ecosystem. This transaction is not just about traditional software expansion, but more about owning a critical layer of AI infrastructure. We are seeing a lot of companies find ways to vertically integrate their AI and data capability. Since AI systems, especially the emerging agentic models, require constant access to real-time data streams, IBM will use Confluent’s ability to act as the “connective tissue” between enterprise systems.

It’s been a rough year for the big tech companies in the stock market.

DKI Takeaway: The acquisition is expected to be dilutive to earnings due to the massive upfront cost and integration expenses, but the long-term thesis positioned around data integration will move in tandem with AI adoption. As AI adoption increases, control over high-value infrastructure layers could command large amounts of revenue and even stronger pricing power than we are seeing right now. This deal highlights the repeated idea that competitive advantage is moving towards those who can control how data is both generated and moved in real time.

2) Nvidia and Emerald AI Announce Partnership with Energy Sector to Launch Power Flexible AI Factories:

At CERAWeek in Houston, Nvidia and Emerald AI announced a collaboration with AES, Constellation Energy, Invenergy, NextEra Energy, Nscale Energy & Power, and Vistra to design power-flexible AI factories/data centers across the United States. These facilities will be built using NVIDIA’s Vera Rubin chips, which offer up to 10x greater power efficiency than prior generations. The factories are also designed to adjust electricity consumption in response to grid conditions, functioning as both AI computing centers and grid assets. The partnership aims to unlock up to 100 gigawatts of flexible U.S. grid capacity. This isn’t from adding new supply; but rather, by making AI facilities responsive to real-time grid conditions and turning these massive electricity consumers into more controllable assets. A commercial launch is planned for later in 2026 at NVIDIA’s Virginia AI Factory Research Center, with Nvidia already piloting this across five commercial data centers worldwide, suggesting the technology is past the proof-of-concept stage.

The stock market didn’t react, but reduced grid strain is a huge benefit.

DKI Takeaway: Data centers have become a threat to grid stability in recent years, drawing substantial amounts of power with little flexibility, and even risking blackouts during stress events like heat waves. This partnership could help change that dynamic. Through Nvidia’s DSX Flex software and Vera Rubin architecture, these new AI factories would be able to manage their own power draw in real-time. Instead of acting as a liability, they’d function as active grid assets that can shed power or tap into onsite reserves to stabilize the system when it’s stressed. This means they would be able to send power back into the grid as needed, which is a significant shift as the industry races to meet the surge in AI-driven electricity demand. If successful, this would take AI datacenters from something that destabilizes the grid to an asset that can change power needs quickly and stabilize the grid. Many Bitcoin miners have made use of this strategy to get preferred access or reduced electricity rates.

3) DoorDash Strikes Multiple Apparel Partnerships:

DoorDash announced that it is partnering with multiple fashion brands such as Urban Outfitters, Dolce Vita, Rally House, and Steve Madden. All four brands are expected to have a formal launch this spring, allowing customers to order clothing, footwear, and other accessories with same-day delivery. DoorDash reiterates that the top 5 apparel order days were all either on or just before major holidays (including Christmas Eve, Halloween, New Year’s Eve, etc.), meaning there’s high demand for last-minute apparel purchases. DoorDash started in this business line with Foot Locker and is now expanding.

The stock price says people are worried about drone delivery and self-driving cars.

DKI Takeaway: This partnership represents a step forward for DoorDash, helping them get closer to becoming an all-encompassing app. Success will come from helping consumers with last-minute holiday shopping and delivery, putting the company in competition with Amazon’s growing 1-hour delivery offers. Combining this with their Foot Locker partnership and same-day delivery structure gives DoorDash a compelling case against the alternatives, whether that’s driving to a store, ordering from a brand’s website, or shopping on Amazon. That type of attraction could help turn last-minute buyers into habitual retail spenders, which may drive more partnerships in the future. (This reminds me a bit of Uber’s recent acquisition of a parking app company which expanded its target market and could bring millions more onto Uber’s platform.)

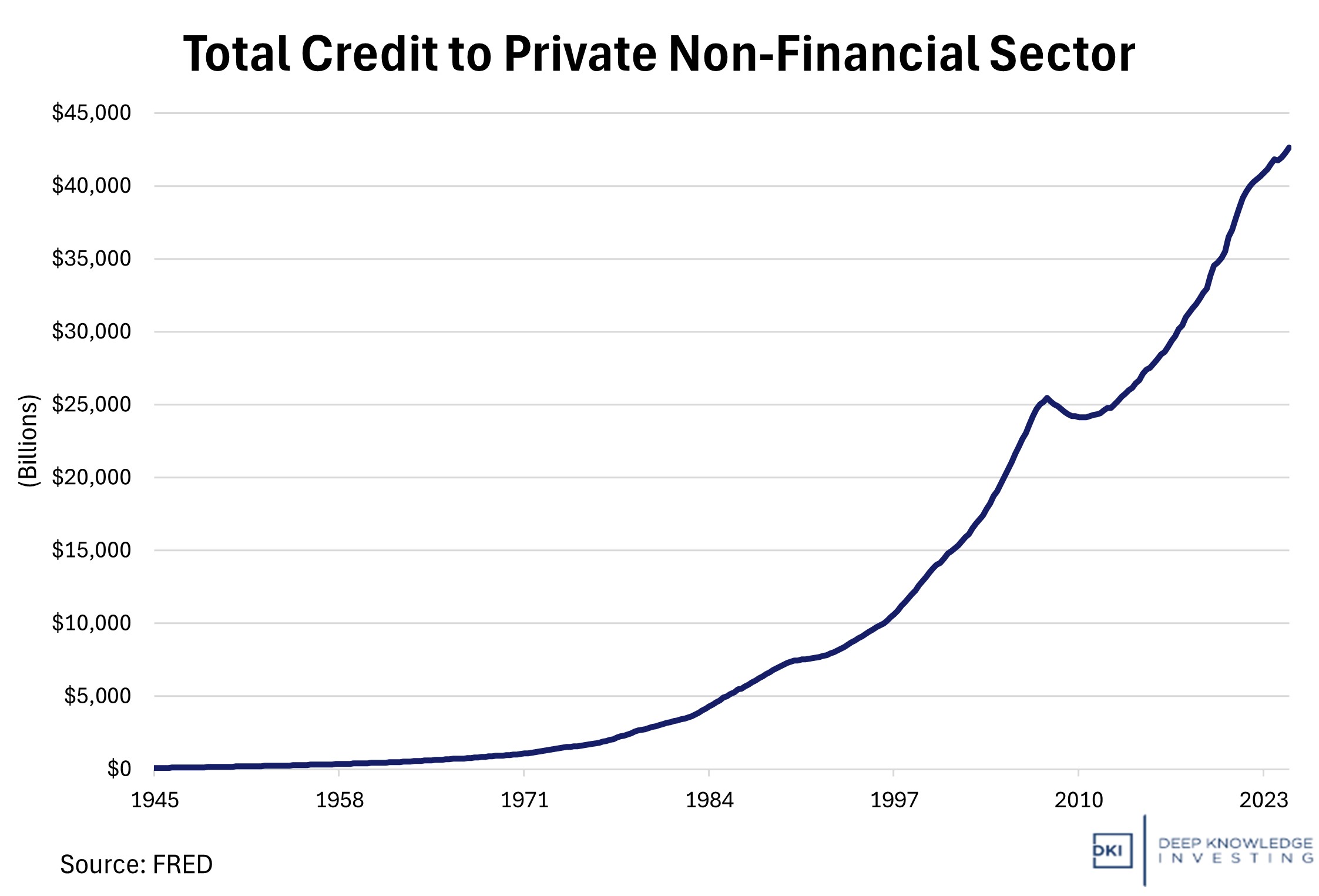

4) Private Credit Faces Mounting Pressure from Downgrades and Liquidity Constraints:

The private credit market, now approaching $2 trillion in size, is under strain as a mix of tighter investor rules and credit concerns is beginning to surface. Moody’s Ratings downgraded FS KKR Capital Corp. to junk status, citing deteriorating asset quality, rising non-accrual loans (about 5.5% of investments), and weaker earnings. This is a rare downgrade in a sector long (and incorrectly) viewed as stable. Several large private credit funds, including those managed by Ares, BlackRock, and Apollo, have capped investor redemptions at around 5% per quarter, even as withdrawal requests surged above 10% of assets. These limits reflect the core structural issue in private credit: funds invest in illiquid loans but offer semi-liquid access to investors, creating tension during periods of stress when people most want liquidity. Market signals have begun to reflect this shift, with widening credit spreads and falling valuations across publicly traded vehicles tied to the space.

The sector is growing and not as safe as many think.

DKI Takeaway: The recent developments suggest that private credit is entering its first real stress test after years of rapid growth. The model worked in a low-rate, high-liquidity environment, but rising defaults and redemption pressure exposed a mismatch between illiquid assets and investors’ expectations for capital access. The downgrade from Moody’s Ratings signals that credit risk is no longer isolated but spreading across portfolios, while redemption caps show that liquidity is conditional, not guaranteed. For investors, the focus should shift from headline returns to underwriting quality, leverage, and liquidity structure, as weaker funds may face valuation pressure and higher borrowing costs. For those of you considering such investments, please note that one of the selling points is often “safety” which is incorrectly defined as low volatility. These assets display low vol because they are rarely marked to market. Not recognizing changes in valuation based on changing market conditions masks volatility instead of reducing it.

5) OpenAI Offers 17.5% Returns to Win Enterprise AI:

Recent headlines suggested OpenAI is “guaranteeing” investors a 17.5% return, but the reality is a little more nuanced. OpenAI isn’t offering public investors a fixed return; but rather, pitching private equity firms to invest in joint ventures that deploy AI tools across the PE firms’ portfolio companies. These deals include preferred equity structures with a targeted minimum return of around 17.5%, designed to incentivize participation. This is a distribution effort. Private equity firms control massive networks of companies across all industries, and partnering with them would allow OpenAI to rapidly scale adoption of its technology and allowing OpenAI to embed its AI tools into hundreds of portfolio companies at once.

I still have concerns about the business model and funding.

DKI Takeaway: While large language model developers are still seeking to build the most advanced models, the biggest players are showing that securing real-world usage is what is most important right now. Distribution is becoming as important as innovation. OpenAI’s willingness to offer structured returns suggests that gaining enterprise adoption quickly is a top priority, even if it requires financial incentives. I have concerns about OpenAI’s business model. Right now, the company has no visible path to earn a return on the hundreds of billions of dollars it has spent nor to secure the nearly $1T of capital required to meet its purchase obligations. Finally, between hallucinations, inappropriate and hidden corporate guardrails, consistently inaccurate analysis, and killing the personalities of carefully curated GPTs, the underlying LLM is losing share.

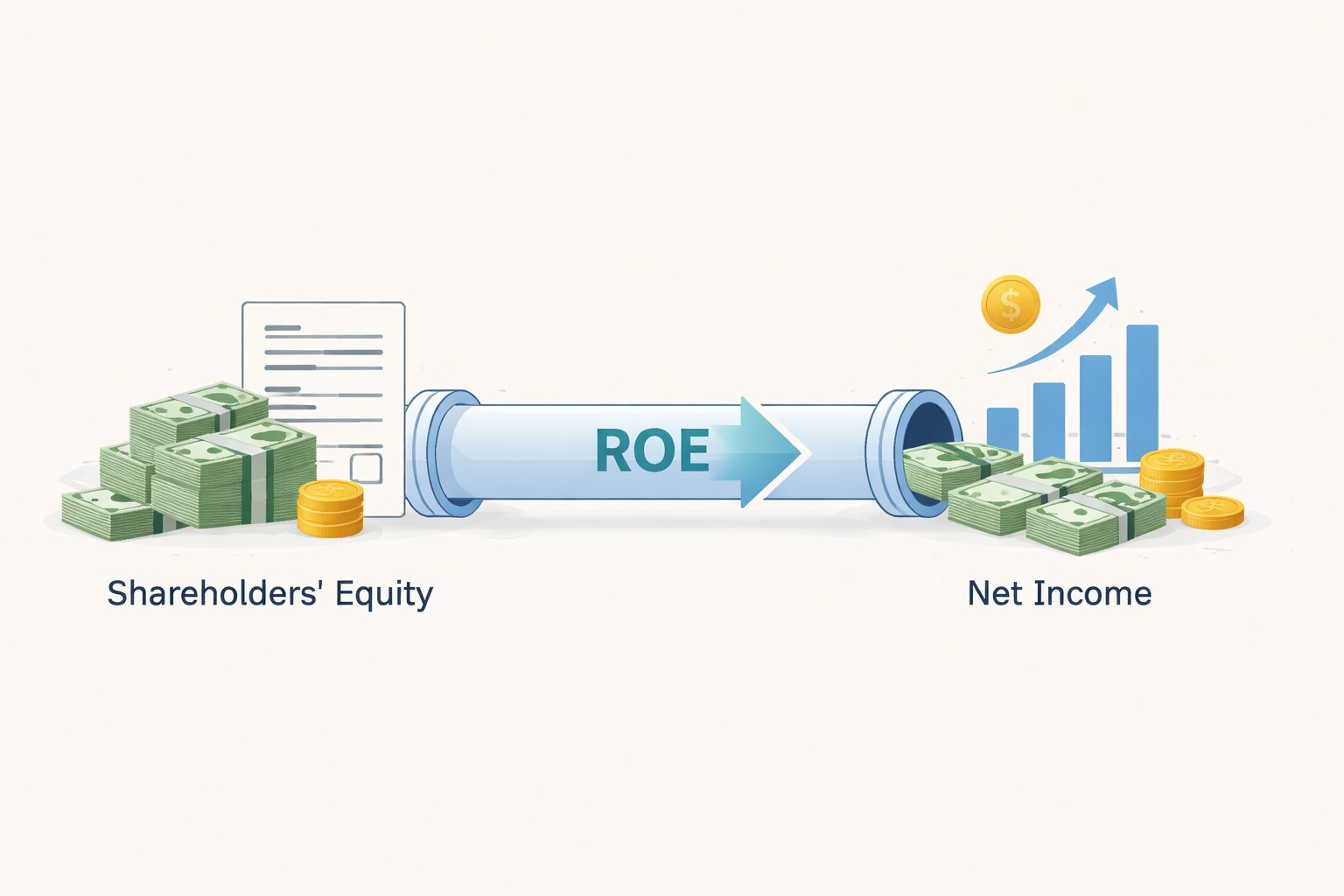

6) Educational Topic: Explaining Return on Equity (ROE):

Return on Equity (ROE) is a profitability metric that measures how effectively a company generates profits from shareholders’ equity. It tells investors how much net income a company produces for each dollar of capital invested by its owners. It is calculated by dividing net income by shareholders’ equity. Shareholders’ equity represents the residual book value of the company after liabilities are subtracted from assets. For example, if a company generates $100 million in net income and has $500 million in equity, its ROE would be 20%, meaning it earns $0.20 for every dollar of book equity. Investors pay attention to ROE because it can provide insight into management’s ability to allocate capital efficiently.

Net income divided by book equity. No need to complicate anything.

DKI Takeaway: A company can boost ROE through higher profitability, efficient use of assets, increased leverage, or by writing down its equity account. Two companies with the same ROE may have different risk profiles if one relies heavily on debt while the other achieves returns through strong margins and efficient operations. Analyzing ROE among other metrics such as profit margins, asset turnover, and leverage tends to paint a fuller picture. While many analysts use ROE in making investment decisions, I tend not to use it because I view book equity as an accumulated measure of historical profitability rather than something predictive. My preference is to focus on free cash flow divided by the market equity value.

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.