Is the Strait of Hormuz closed? There have been rumors of ships on fire and Iranian success in adding mines. Some of these rumors were lies and later became true, but as long as captains and ship owners think there’s danger, then the Strait is effectively closed. We saw intra-day oil price moves of 20% – 30% this week based on press releases and social media posts. If you’re feeling overwhelmed and whipsawed, check out DKI’s post on managing your feelings during record volatility. The CPI was flat with last month, but with higher March energy prices on the way, no one cared much about the February results. The PCE has started rising again so the Fed doves will need to wait for a while. AI power demands have gotten so extreme that private equity is now buying power companies because additional financing is required. The US is going to build its first new refinery in half a century. Let’s hope construction starts and that the project isn’t delayed by decades of regulatory overkill. Finally, it was poor risk management and the challenging timing of the dreaded margin call that killed several hedge funds during the GameStop situation a few years ago. If you’ve ever wondered what a margin call is or why it can be dangerous to your portfolio, read on. We’ll explain.

This week, we’ll address the following topics:

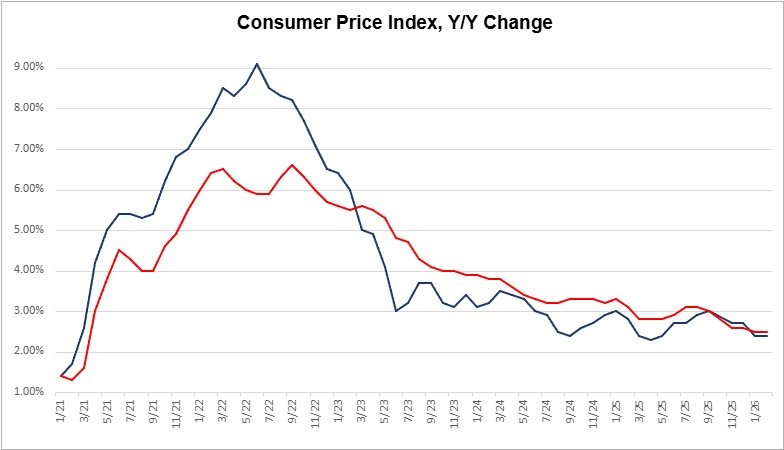

- The CPI was flat with last month and has been too high for half a decade. It will be up on higher energy prices next month. Is there anything the Fed can or will do?

- Oil prices have had 20% – 30% intraday moves based on press releases, social media posts, and rumors (some true). We explain the situation and provide a link for how I’m thinking about investing in volatile markets.

- Blackrock leads a group to acquire power producer, AES. Some public electric generators can no longer fund enough growth to meet AI requirements.

- Crude oil is worthless until it gets to a refinery. The US is going to build its first new refinery in half a century.

- Ever wonder what a margin call is and why it’s potentially so dangerous? We explain in this week’s educational topic.

A round of applause for DKI’s star interns, Cashen Crowe, Samaksh Jain, and Kunal Arora who all made meaningful contributions to this week’s 5 Things. Much of what you’re about to read reflects their careful analysis.

Ready for a week of mines in the water? We’re not, but let’s dive in anyway:

1) CPI:

This week, we got the January Consumer Price Index (CPI) report which showed an overall increase of 2.4% for the last year. That’s flat compared to last month and consistent with expectations. The monthly change was 0.3% also consistent with the estimate. The Core CPI which excludes food and energy was up 2.5%, flat with January and consistent with expectations. The Core change was up 0.2% vs last month and also in line with estimates. (It was a good month for the forecasters.) These numbers remain well above the 2% target and have been so since 2021, but were also down from 4Q ‘25 prints. Yet again, shelter (housing) was the biggest reason for the increase.

Schrodinger’s inflation. Is the line pointing down, or is it too high?

DKI Takeaway: We’re going to see an increase in inflation (at least for March) due to higher energy prices. Regardless of that, the CPI remains too high and is consistently understated. While I think the Fed and the White House would like to see a cut in the fed funds rate, expect them to pause at the current level. (A higher PCE almost guarantees this outcome.) I continue to believe that the primary cause of inflation is Congressional overspending and there’s nothing the Fed can do to change that. Expect continued debasement of the dollar. While some think we’ll have AI-related deflation, that hasn’t happened yet. If it were to happen, expect massive government spending programs and a restart of the Fed money-printer. At $38T in on-balance sheet debt, Washington DC isn’t going to stomach deflation that makes the outstanding debt more valuable. If you want more detail, check out DKI’s full analysis (not paywalled).

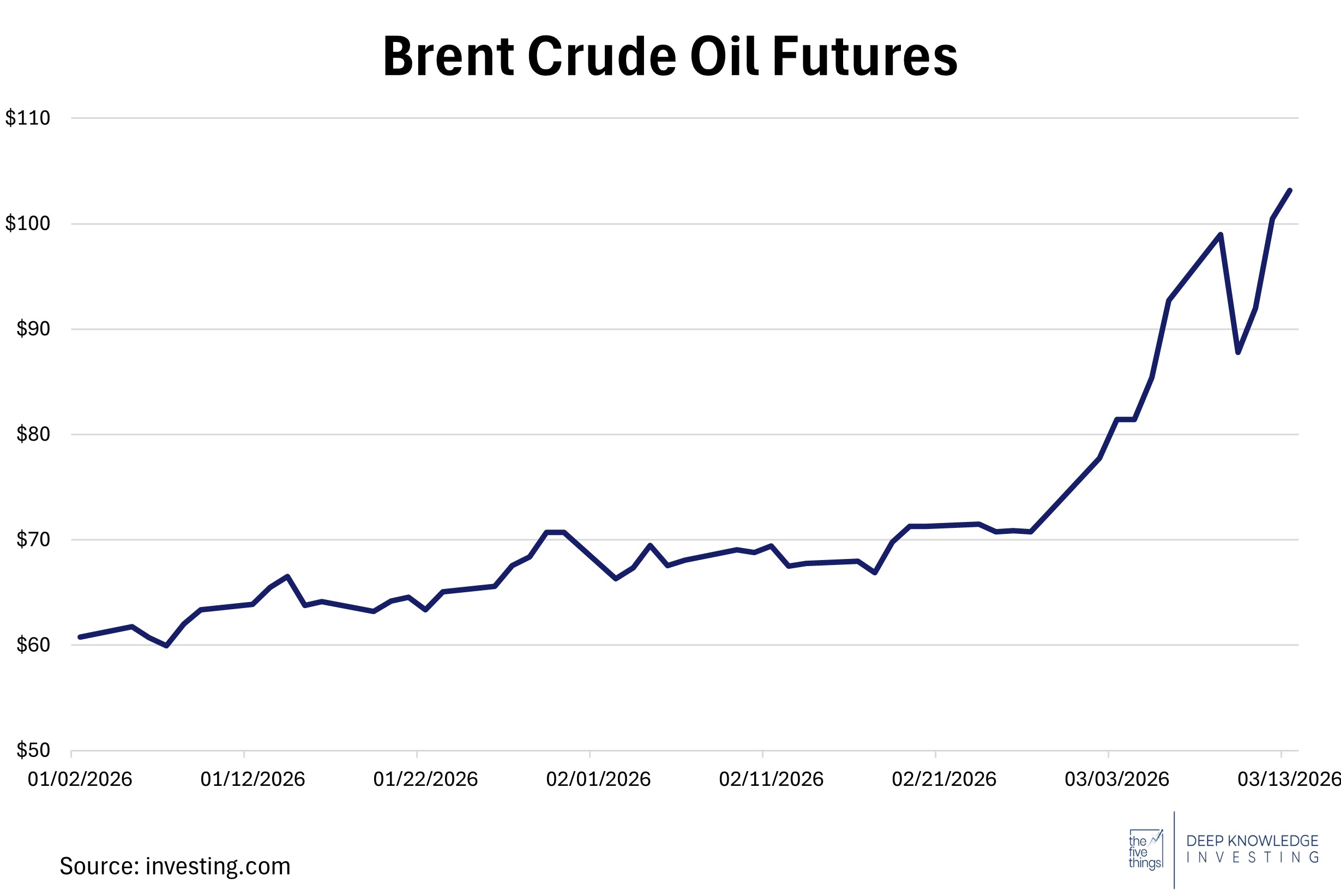

2) Oil Sees Extreme Fluctuations Amid Global Tensions:

Over the past week, global energy markets have experienced some of the most extreme fluctuations in recent history. Prices surged from around $90 to an overnight peak of close to $120 per barrel on Monday, triggered by a near-total closure of the Strait of Hormuz caused by stories of ships on fire and mines in the Strait. Prices then fell into the $80s after President Trump claimed the conflict was nearing an end, said the US would waive oil-related sanctions on Russia, and the G7 said there would be a release of reserves. Later in the week, Brent spiked back above $100 due to new reports of mines in the Strait as well as damage and shutdowns at some oil-producing facilities.

This is calm compared to the intra-day charts.

DKI Takeaway: The problem with releasing reserves is the market understands it’s a temporary measure. This is complicated by the fact that US reserves are lower than usual due to the prior White House depleting them to lower gas prices ahead of the election. I don’t think it matters much whether ships in the Strait have been hit or whether Iran has placed mines. Right now, captains are worried they can’t get through the Strait safely, so there’s almost no traffic. Most of them won’t move until they know it’s safe, and as of now, the insurance market isn’t fully functioning. The volatility in the oil market is at historic highs and has had 20% – 30% intraday moves based on unpredictable press releases or social media posts. It’s hard to navigate markets like this. Check out this week’s post “Finance and our Feelings” about avoiding bad decisions.

3) BlackRock Leads Consortium to Take AES Private:

A consortium led by BlackRock’s Global Infrastructure Partners and EQT reached an agreement to acquire AES Corporation, a leading US electricity supplier, in a transaction valued at $33.4 billion. The deal is structured as an $15/share all-cash offer representing a total equity value of $10.7 billion. The remainder is assumed debt. While the offer provides a 40% premium over AES’s share price from July 2025 (when news of the deal first leaked), it sits below the $17+ level the stock reached in February 2026. The deal, which includes co-underwriting from CalPERS and the Qatar Investment Authority, is expected to close in late 2026 or early 2027, pending regulatory and shareholder approval.

Shareholders had hoped for more.

DKI Takeaway: Shareholders had hoped for a better price. Following the $15/share announcement, the stock fell 17%. The deal gives AES access to the capital it needs to expand capacity and meet surging electricity demand. Without it, the company would have had to issue large amounts of equity and/or stop distributing dividends. Now, private ownership will allow the company to focus on meeting its goals without worrying about investor concerns every quarter. The fact that a company of this size can no longer self-fund growth to meet surging electricity demand reflects a shift in the energy sector. AI infrastructure is driving capex requirements that are outpacing the financing capacity of utilities, forcing them into the arms of private equity, a trend we expect to see continue.

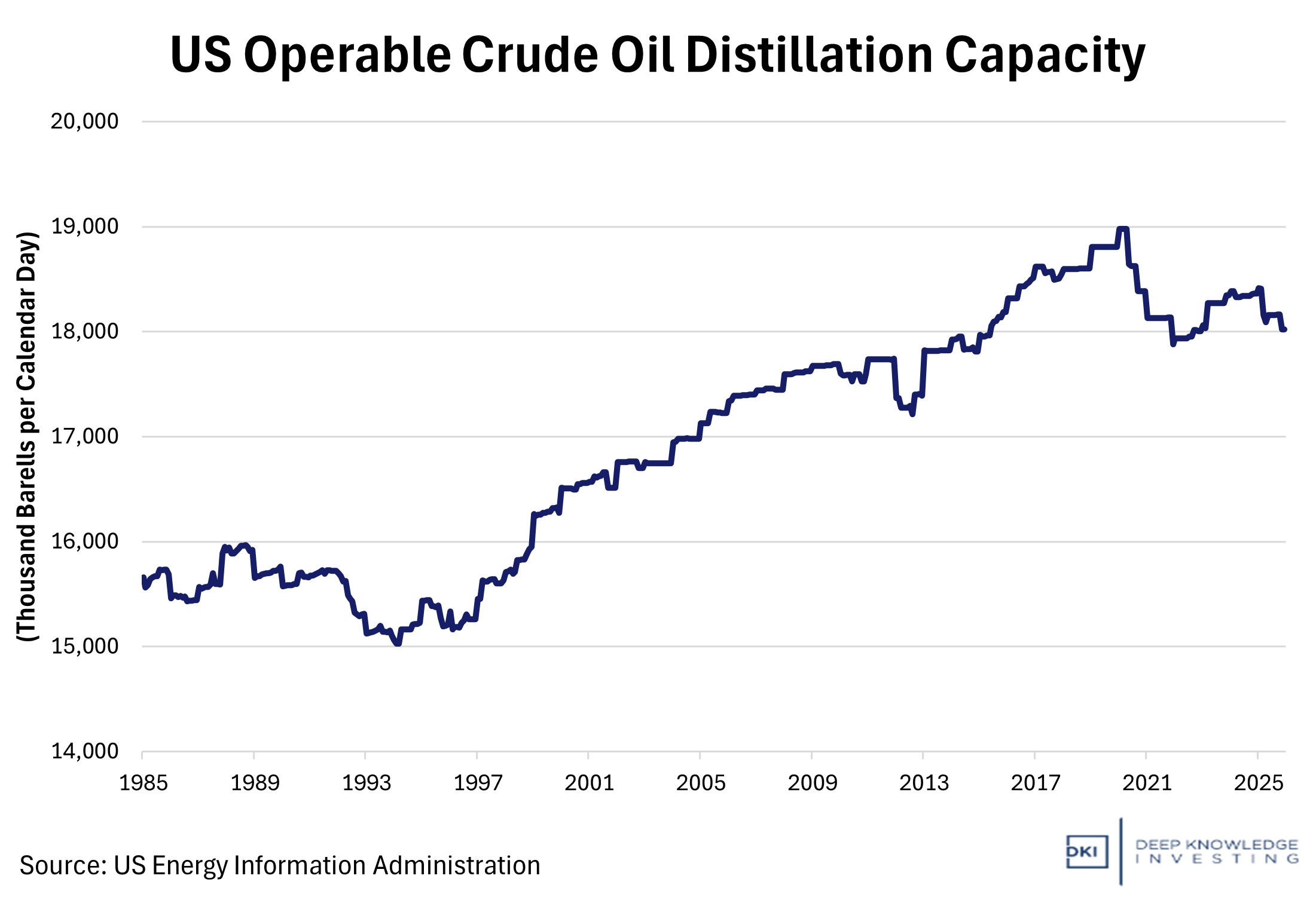

4) US Plans First New Oil Refinery in 50 Years Amid Iran Conflict:

President Trump announced that the United States will build its first new oil refinery in 50 years in Brownsville, Texas, with backing from Reliance Industries. The refinery is expected to process 168,000 barrels of crude per day and will be designed to handle light shale oil, which many existing Gulf Coast refineries are not optimized to refine. The US military has avoided targeting Iran’s oil infrastructure to prevent additional shocks to the global energy supply. 20% of global oil supply flows through the Strait of Hormuz, although the ability of Middle Eastern oil producers to re-route crude is greater than expected. The refinery announcement reflects a shift toward expanding domestic capacity after decades in which the U.S. industry focused on upgrading existing facilities rather than building new ones. We’re hoping the regulatory and permitting process succeeds.

We’d like to see that capacity increase.

DKI Takeaway: This highlights an overlooked constraint in the global energy system: refining capacity over crude supply. Over the past several decades, the US increased oil production through shale drilling but added little refining infrastructure, leaving the system dependent on aging plants optimized for different crude types. A refinery built for light shale oil could improve domestic fuel processing and strengthen US export capacity for the Latin American markets. The decision to avoid bombing Iranian oil infrastructure reinforces this dynamic. Destroying supply assets would risk a major oil price spike and amplified global inflation shock. There’s an old expression noting that crude oil is worthless until it gets to a refinery. For years, US efforts have focused on increasing oil production. The government is starting to respond to the need for additional refining capacity.

5) Educational Topic: Explaining Margin Calls:

A margin call occurs when an investor who has borrowed money to purchase securities has the collateral in his brokerage account fall below a minimum threshold. When investors buy stocks on margin, they are using borrowed money to increase their exposure. Because part of the investment is financed with borrowed funds, brokers require investors to maintain a minimum level of equity in the account at all times, called the maintenance margin. If the value of the securities in the account declines, the investor’s equity shrinks. Once it falls below a maintenance requirement, the broker issues a margin call.

Leverage increases returns; both positive and negative.

DKI Takeaway: Once the broker issues a margin call, the investor can either add additional capital to the account, or sell positions to reduce exposure and raise cash. If the investor fails to respond quickly, the brokerage has the authority to sell assets at its discretion. Margin calls can be responsible for large short squeezes because they force an investor to cover short positions at the worst possible time. The key point is once a margin call is issued, investors no longer have the ability to wait for potential better future prices; and instead, have to reduce exposure immediately. In the recent GameStop short squeeze, large hedge funds had to cover their short positions at prices far above where the stock was just weeks or even days later. The losses, which were amplified by leverage, ended several businesses.

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.