The Fed cuts by 25bp as expected with more Fed Governors dissenting. At this point, nothing the Fed is going to do actually affects the rate at which businesses and homebuyers borrow. However, a restart of QE (however you want to define the term) means they’re committed to more inflation. The DKI portfolio is prepared for this. (Hint – own hard to replicate assets.) Netflix is in a bidding war for Warner Bros. Discovery. There are huge antitrust implications. Oracle beats EPS estimates, but the market isn’t happy with cap-x plans. Of greater importance, where is OpenAI going to get the $300B that makes up almost 60% of the Oracle backlog? SpaceX is going public with a huge valuation. The expensive Mars efforts get the headlines, but satellite delivery and worldwide telecom/internet are real businesses with incredible capabilities. Will Elon Musk become the world’s first trillionaire? Finally, in our educational topic, we describe the process of pricing IPOs (Initial Public Offering). Ever wonder how that happens? Do investment banks have a plan or just a Ouiji Board? We explain.

This week, we’ll address the following topics:

- The Fed cuts 25bp. It won’t affect the bond market. The Fed has lost control. QE has restarted. Do you own enough inflation protection?

- Netflix ($NFLX) comes to an agreement to buy the studio and streaming assets of Warner Bros. Discovery ($WBD) for $83B. Paramount ($PSKY) launches a larger hostile bid. Antitrust regulators should be watching closely.

- Oracle ($ORCL) beats EPS estimates, but the market doesn’t like the increase in cap-x required to build out AI infrastructure. The bigger issue is OpenAI is $300B of the $500B+ revenue backlog. OpenAI doesn’t have $300B.

- SpaceX is preparing for an IPO. Going to Mars will be expensive, but the company already has multiple revenue-producing business lines and incredible capabilities.

- Ever wonder how initial public offerings get priced? We explain in this week’s educational topic.

1) Fed Meeting:

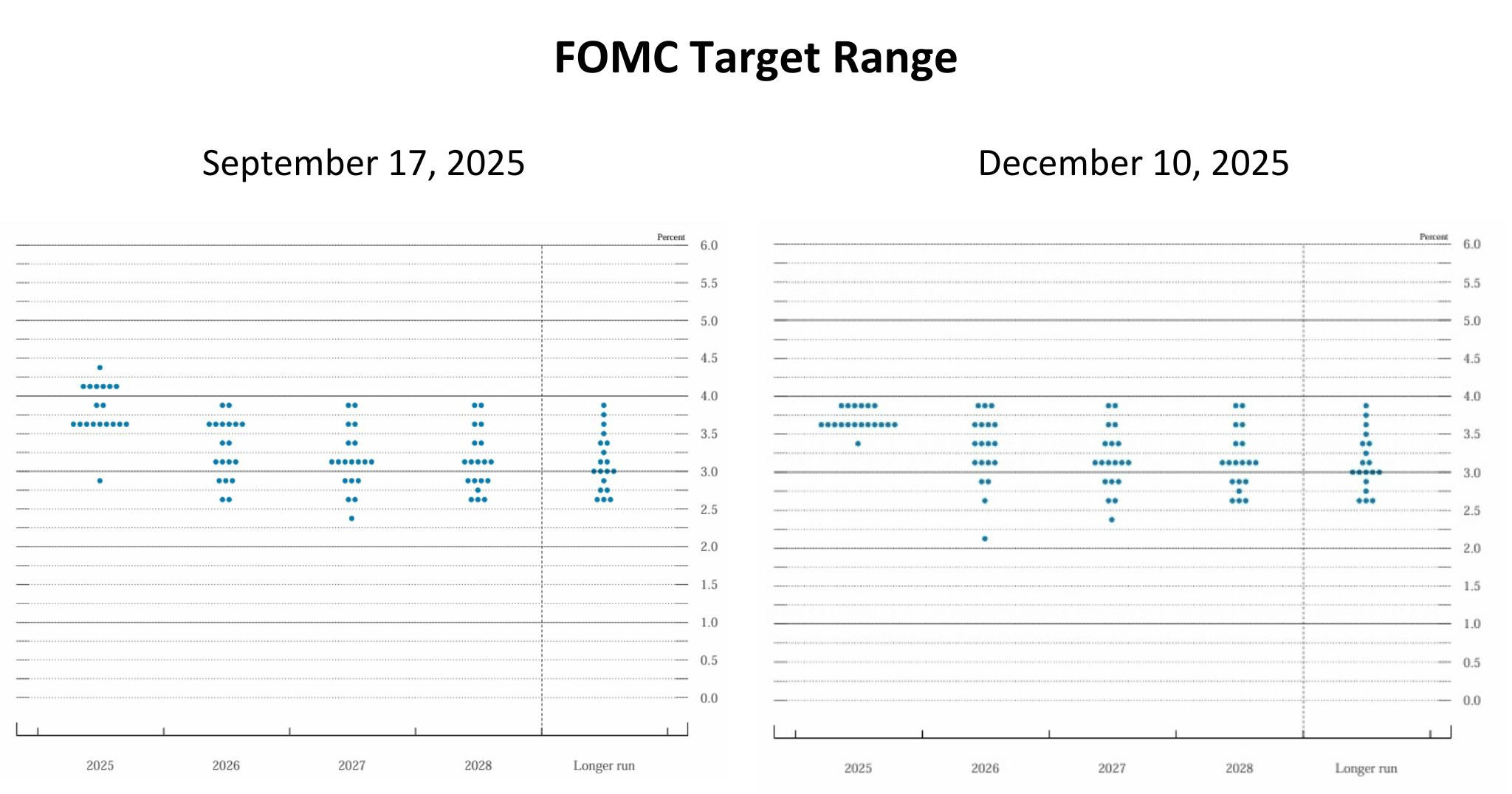

The Federal Reserve concluded its last meeting of 2025 and as expected, lowered the fed funds rate by 25bp (.25%). In an increasingly more common event, there was dissent. For years, any Fed Governor dissenting was unusual. Any arguments were held behind closed doors while the committee presented a unified face to the public. The vote had three dissents, something that hasn’t happened since 2019. One Governor (Miran) wanted a 50bp cut while two (Goolsbee and Schmid) wanted no change.

This was one of the four meetings each year where the Fed provides the “dot plot”. That’s the graph where each Fed Governor indicates where they expect the fed funds rate to be for each of the following few years. While there was some movement within the graph, the averages remained unchanged.

The press release indicated the reason for the 25bp cut was the committee thought there was more risk to employment than there was to inflation. Based on the employment numbers that have been announced recently (which tend to be highly-inaccurate), it looks like the employment market is in decent shape. Conditions have declined from the post-Covid period when companies were desperate to hire, but they’re still good unless you’re a recent college graduate. On the other hand, inflation has remained well-above the 2% target for years and based on the CPI, has been increasing in recent readings. As I’ve noted in previous posts, the Fed continues to pay lip-service to the 2% target, but has effectively moved the real target to something in the 3% – 4% range.

The biggest news was in the implementation note where the Fed indicated they would “Increase the System Open Market Account holdings of securities through purchases of Treasury bills and, if needed, other Treasury securities…”. Quantitative Easing is back and the money-printer is restarting. I think this is all a mistake, but I don’t have a vote. The right move here is to own hard assets that are difficult to duplicate while Congress and the Fed continue to debase the dollar and crush its purchasing power.

Any changes were not meaningful – except restarting QE.

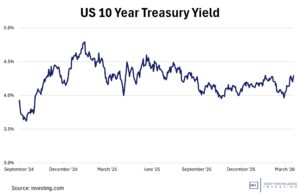

DKI Takeaway: I don’t think any of this matters. Earlier The Wall Street Journal wrote that the Fed has cut 1.75% (175bp) since the start of this cycle in September, 2024, and “somehow” the yield on the 10-year Treasury has increased. It’s not “somehow”. The bond market is pricing in higher projected long-term inflation.

The Fed has completely lost control of the situation. In general, corporations borrow based on the 5-year Treasury and mortgages get set based on the yield on the 10-year. The Fed can cut all they want, but the bond market isn’t buying at those prices. In a related move, President Trump is going to appoint a new Fed Chair soon who will be even more dovish than the too-dovish Powell. Rates will continue to fall, but the fed funds rate is the overnight rate. The bond market sets the price on the rest of the yield curve. The President is now traveling around the country to try to convince people that inflation is no longer a problem. President Trump doesn’t have any more control over the situation than Chairman Powell does.

There is only one fix for the situation and that’s a massive cut to Congressional spending (not rate cuts and QE). This is never going to happen. My conclusions:

– Ignore anything Chairman Powell said in his press conference.

– Ignore anything President Trump says about inflation.

– Congressional overspending will continue.

– Under the coming guidance of a new Chairman, the Fed will continue to cut the fed funds rate and continue QE.

– Prepare for higher long-term inflation. The DKI portfolio is more optimized for this outcome than anything else right now.

Note: There is currently a debate on Fin-X regarding whether the Fed buying more bonds is technically quantitative easing or not. I agree with Lyn Alden on this one that regardless of the label, it constitutes money-printing. The end result is the same.

2) Netflix’s Warner Bros Deal Sparks Hostile Rival Bid:

Netflix agreed to an $83B acquisition of the studio and streaming assets of Warner Bros. Discovery, kicking off one of Hollywood’s most contentious media fights in years. Netflix agreed to pay roughly $27.75 per Warner Bros. Discovery share in cash and stock while Paramount Skydance launched a hostile $30-per-share ($108 billion) all-cash bid directly to Warner shareholders. Paramount argued that its offer surpasses Netflix’s in value and regulatory clarity. The contest has attracted sovereign wealth backing and intensified competition for global content rights and distribution. Meanwhile, the Trump administration has publicly weighed in, expressing concern that the Netflix deal could pose antitrust challenges given the combined market share of Netflix, HBO Max, and Warner.

It costs a lot to make content. It costs a lot to buy content in a bidding war.

DKI Takeaway: This multi-front battle illustrates that mega-deals in dominant digital and media categories are no longer just commercial decisions; they are policy flashpoints. Netflix’s bid would create an industry giant with an unprecedented content arsenal, but Paramount’s hostile counteroffer and the likely regulatory response underscores widespread concern that concentration at the top of the streaming stack can threaten competition. Regulatory risk is now a required concern for blockbuster media M&A, and market share. Should regulators insist on significant divestitures or conditions, it could reshape not just this transaction but the broader consolidation playbook for legacy and streaming media. Some believe that if Netflix completes the acquisition as planned, it would end the movie theater business. I’m skeptical, but the analysis is worth reading. $AMC has been a meme stock favorite and could be facing a problem.

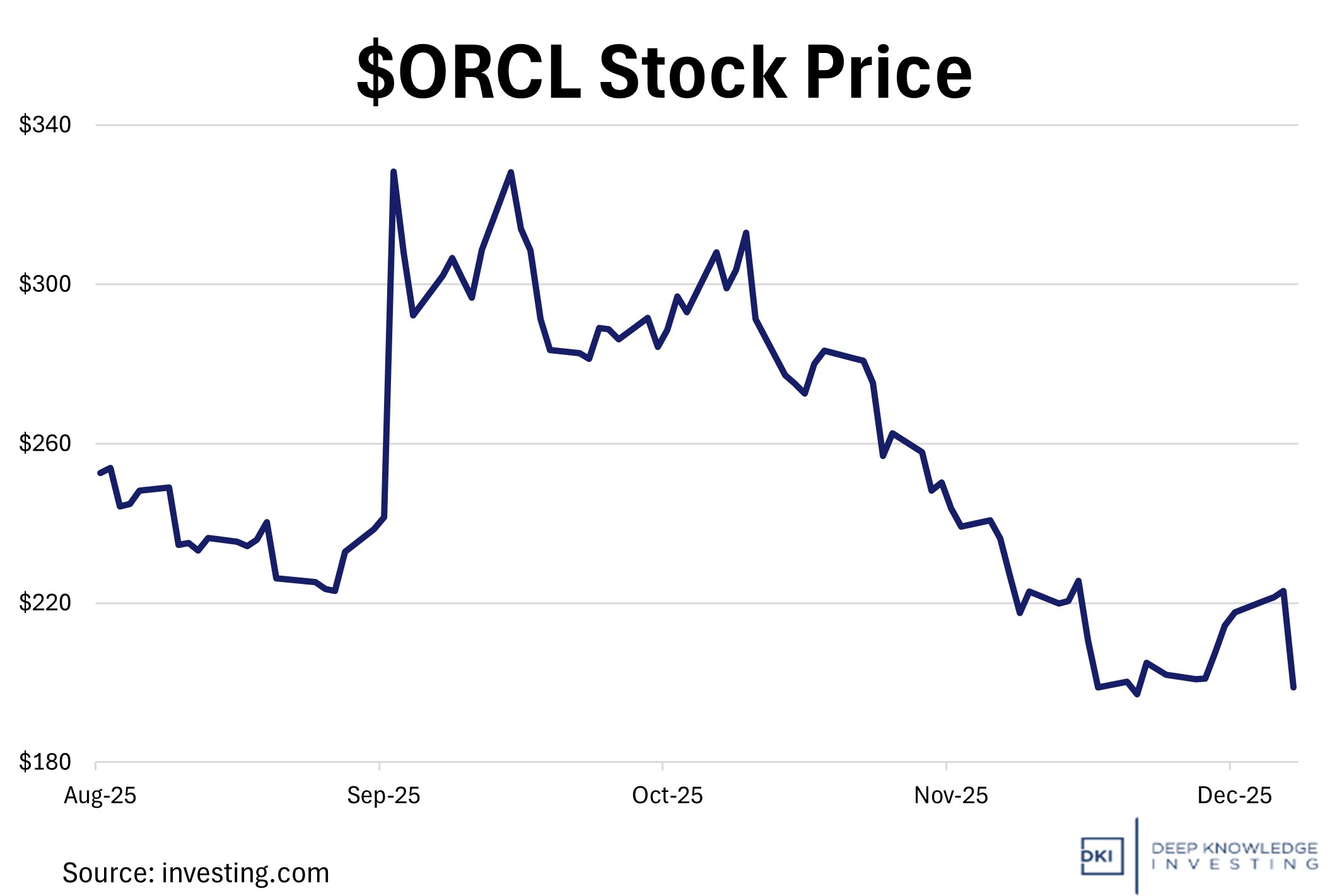

3) The Problem with Oracle’s Backlog:

Oracle ($ORCL) revealed a record $523 billion backlog of cloud contracts fueled mostly by AI infrastructure deals. While this massive pipeline of revenue displays the huge demand for Oracle’s services, the company is spending a fortune on building the necessary infrastructure. New multi-year cloud commitments from OpenAI, Nvidia ($NVDA), and Meta ($META) have largely been driving this backlog. As we covered in September, the massive OpenAI commitment led to a one-day 36% surge in Oracle’s stock price. However, with revenue growth coming in below expectations and management reducing guidance, investors are expressing concerns. Of greater concern, Oracle’s capex has exploded to meet demand, reaching roughly $12B last quarter. The company has taken on roughly $100B in debt to finance the expansion.

Investors were not happy about the details of this week’s earnings announcement.

DKI Takeaway: Oracle has an incredible half a trillion dollars of revenue backlog. The (potential) issue is that about $300B of it comes from OpenAI. OpenAI is the maker of ChatGPT and it expects to burn more than $100B in cash in the next few years. It also doesn’t have $300B. So, for Oracle to turn its backlog into actual revenue, someone needs to look past OpenAI’s massive cash burn and lack of a proven business model, and provide them with something close to half a trillion dollars in cash. As DKI reported in multiple recent editions of The Five Things, there is a lot of overlap in agreements and arrangements among the big AI companies. If OpenAI falls short, it would be devastating to Oracle, would reduce the revenue growth at Nvidia, and require a big write-off at Microsoft. Over the next two weeks, when you look at the 2026 and 2027 analyst forecasts for the S&P 500, see if any of them include this possible scenario.

4) SpaceX’s Potential 2026 IPO:

Elon Musk’s SpaceX is planning an IPO in 2026, which would give public investors the first chance to own a stake after years of private growth. Estimates of the expected size are roughly $1.0 – 1.5T, ranking among the largest IPOs ever. Starlink is now one of the biggest revenue drivers, and plans to extend service to cell phones could soon rival large telecommunication companies. SpaceX has goals spanning from worldwide broadband to interplanetary travel, explaining the need to raise such a large amount of capital.

Worldwide internet plus they can catch a rocket with chopsticks.

DKI Takeaway: An initial market cap of over $1T means very high growth expectations. Ambitious projects, like plans to colonize Mars, will require heavy spending and years to pay off. This could be another test of shareholder patience. Still, SpaceX can be a global telecommunications and high-speed internet competitor today and the company is already a leader in the satellite delivery business. Their rocket technology is industry-leading; especially the ability to reuse rockets. The IPO could make Elon Musk the world’s first trillionaire. Never bet against the man who can catch a reusable rocket with chopsticks.

5) Educational Topic: How IPO Pricing Works:

When a company goes public through an initial public offering (IPO), many ask how the share price is set. IPO prices are a result of careful analysis, investor demand assessment, and negotiation. A company looking to go public will hire one or more investment banks as underwriters who will evaluate the company’s finances and market potential to propose an initial price range for the offering. The banks typically work on “book-building” as part of a roadshow (a series of presentations to institutional investors) to gauge the amount of interest in stock. Investors then submit bids indicating how many shares they would buy and at what price. IPO pricing is ultimately driven by market-based discovery with the goal of setting a price that meets both investor demand and company fundraising objectives.

It’s simply a private evaluation of supply and demand.

DKI Takeaway: Market conditions and company-specific factors play a large role as well. The strength of a company’s financials and growth, as well as market conditions and industry sentiment all influence IPO pricing. A declining market can negatively affect IPO pricing or even cause the offering to be delayed. The price needs to be attractive enough to ensure the offer sells out smoothly leaving initial investors with expectations of profit, but not so low that the company doesn’t raise much less money than they could have.

Information contained in this report, and in each of its reports, is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied. DKI makes no representation as to the completeness, timeliness, accuracy or soundness of the information and opinions contained therein or regarding any results that may be obtained from their use. The information and opinions contained in this report and in each of our reports and all other DKI Services shall not obligate DKI to provide updated or similar information in the future, except to the extent it is required by law to do so.

The information we provide in this and in each of our reports, is publicly available. This report and each of our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion in this and in each of our reports are precisely that. Our opinions are subject to change, which DKI may not convey. DKI, affiliates of DKI or its principal or others associated with DKI may have, taken or sold, or may in the future take or sell positions in securities of companies about which we write, without disclosing any such transactions.

None of the information we provide or the opinions we express, including those in this report, or in any of our reports, are advice of any kind, including, without limitation, advice that investment in a company’s securities is prudent or suitable for any investor. In making any investment decision, each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable, based on this or any of its reports, or on any information or opinions DKI expresses or provides for any losses or damages of any kind or nature including, without limitation, costs, liabilities, trading losses, expenses (including, without limitation, attorneys’ fees), direct, indirect, punitive, incidental, special or consequential damages.