It was a big week for the tech industry. Nvidia and Meta signed a deal for GPUs and CPUs that caused (valid) concerns about Intel and AMD. Google is making a bid for a share of the AI chip business with its TPUs. And if the future trend for compute goes from training to inference, then expect Intel and AMD to take some share back from Nvidia. This is fascinating and a trend leading me to do weekly research calls. Then, we got news that Abu Dhabi’s sovereign wealth fund has committed to spending $100B on AI infrastructure with OpenAI and Anthropic. Despite no one having a business model to earn a return on these massive investments, companies and countries are afraid to stop spending and potentially miss out on the next big move in technology. Japan promised to invest over half a trillion dollars in the US and is leading off with $36B in much-needed energy infrastructure. The deal could also create better energy security for Japan. Kraft Heinz upset Warren Buffet with plans to split into two companies. It’s now reversed those plans and will try to improve margins as a consolidated company. In our educational topic, we explain the difference between investment grade bonds and high yield. More importantly, we explain why it’s important to do your own work instead of trusting the ratings agencies.

This week, we’ll address the following topics:

- Nvidia and Meta sign a deal for GPUs, CPUs, and networking. What’s that mean for AI spending?

- The Abu Dhabi sovereign wealth fund commits to spending $100B on AI infrastructure with OpenAI and Anthropic.

- Japan promised $550B of investment in the US and is starting with $36B of energy infrastructure spending, something that should help both countries.

- Nvidia and Meta announce a deal that causes concern that Intel and AMD could lose share. But Nvidia is investing in Intel and developing chips with them. The next move in AI could see compute share move from Nvidia to Intel and AMD.

- Kraft Heinz upset Warren Buffet by planning a split of its assets. The new CEO thinks he can improve margins and pricing without the split.

- Ever wonder what the difference is between an investment grade bonds and high yield? We explain and add a warning about why you shouldn’t trust the rating agencies.

DKI’s interns do their usual excellent job. Cashen is healthy again and back organizing the 5 Things. Despite Rutgers’ midterms this week, Samaksh and Kunal deliver thoughtful analysis. These three students have been responsible for selecting the topics, doing initial analysis and writing, and producing the Five Things graphs. Please extend them a mental round of applause as you read this week’s edition.

Ready for a week of more CPU and GPU news? Let’s dive in:

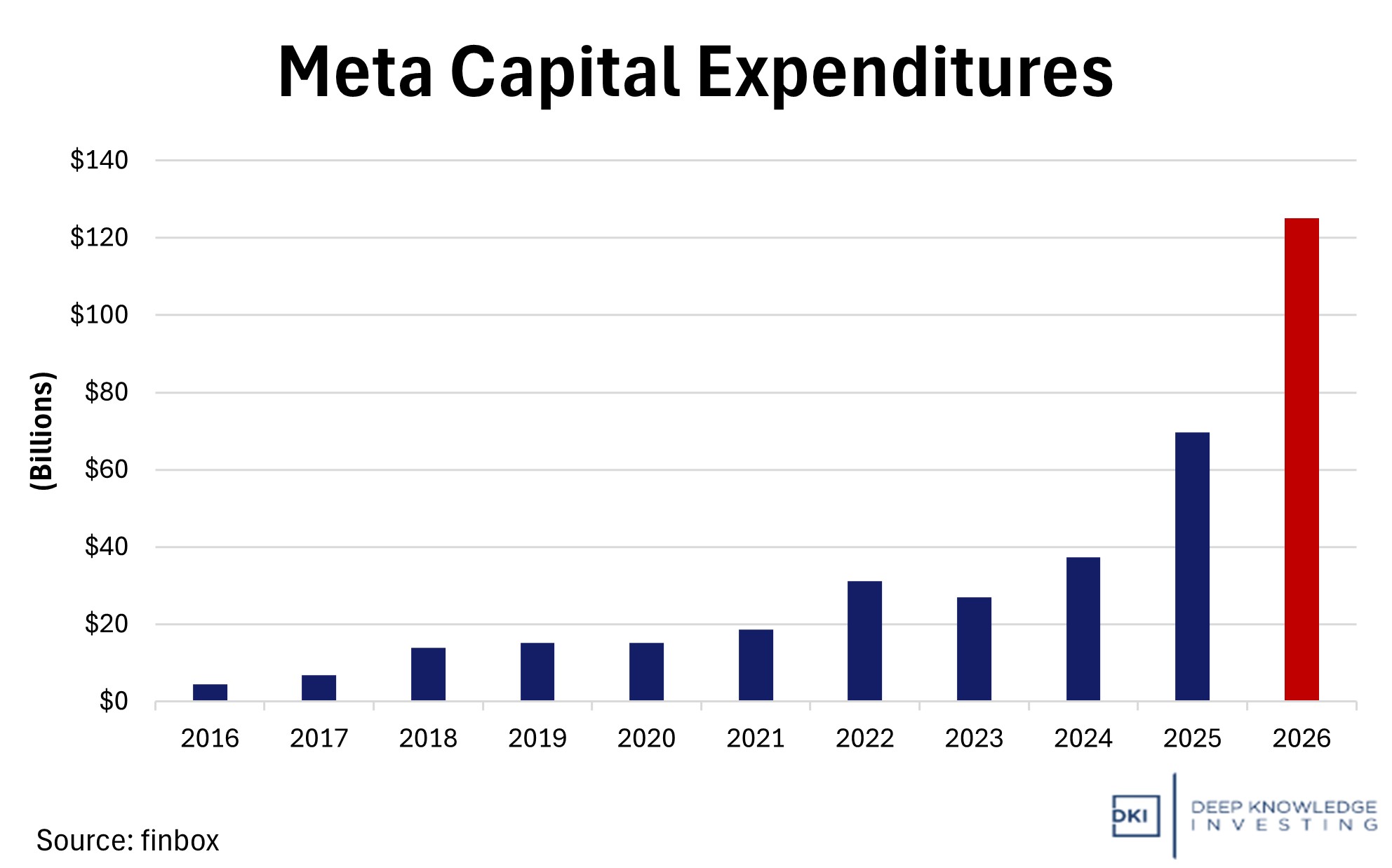

1) Nvidia and Meta Expand Multi-Year AI Infrastructure Partnership:

Nvidia and Meta Platforms announced an expanded partnership last week in which Nvidia will supply Meta with millions of AI chips, including its current Blackwell GPUs and future-generation Rubin GPUs alongside central processors and high-speed networking hardware. The deal is designed to supply Meta’s hyperscale AI data centers, supporting both training and inference workloads. Neither company disclosed the full financial terms, but analysts estimate the engagement could be valued in the tens of billions of dollars as Meta executes massive build-outs of new data centers. Meta’s continued investment in Nvidia hardware occurs even as it develops in-house AI silicon and explores other options with Google’s TPUs indicating a desire to maintain multiple suppliers.

If they don’t keep spending, the value of prior spending will become zero.

DKI Takeaway: This expanded deal underscores Nvidia’s strategic dominance in AI infrastructure, even in an era of increasing chip alternatives and in-house development efforts. For Meta, locking in a multiyear supply of Blackwell and Rubin accelerators, with CPUs and networking, de-risks one of the biggest bottlenecks in scaling AI: reliable, high-performance hardware. Nvidia remains the default backbone for advanced AI workloads for now. (More on that later in this week’s 5 Things.) Long-term risk remains in customer dependence and compute diversification. Any shift by hyperscalers toward alternatives like Google TPUs or successful internal chip programs is a threat to the GPU market leader. For investors, this deal is a signal that AI infrastructure spending is not slowing, and that integration of hardware, networking, and secure processing will matter as much as raw model capability.

2) Abu Dhabi’s Ambitious $100B AI Bet with OpenAI and Anthropic:

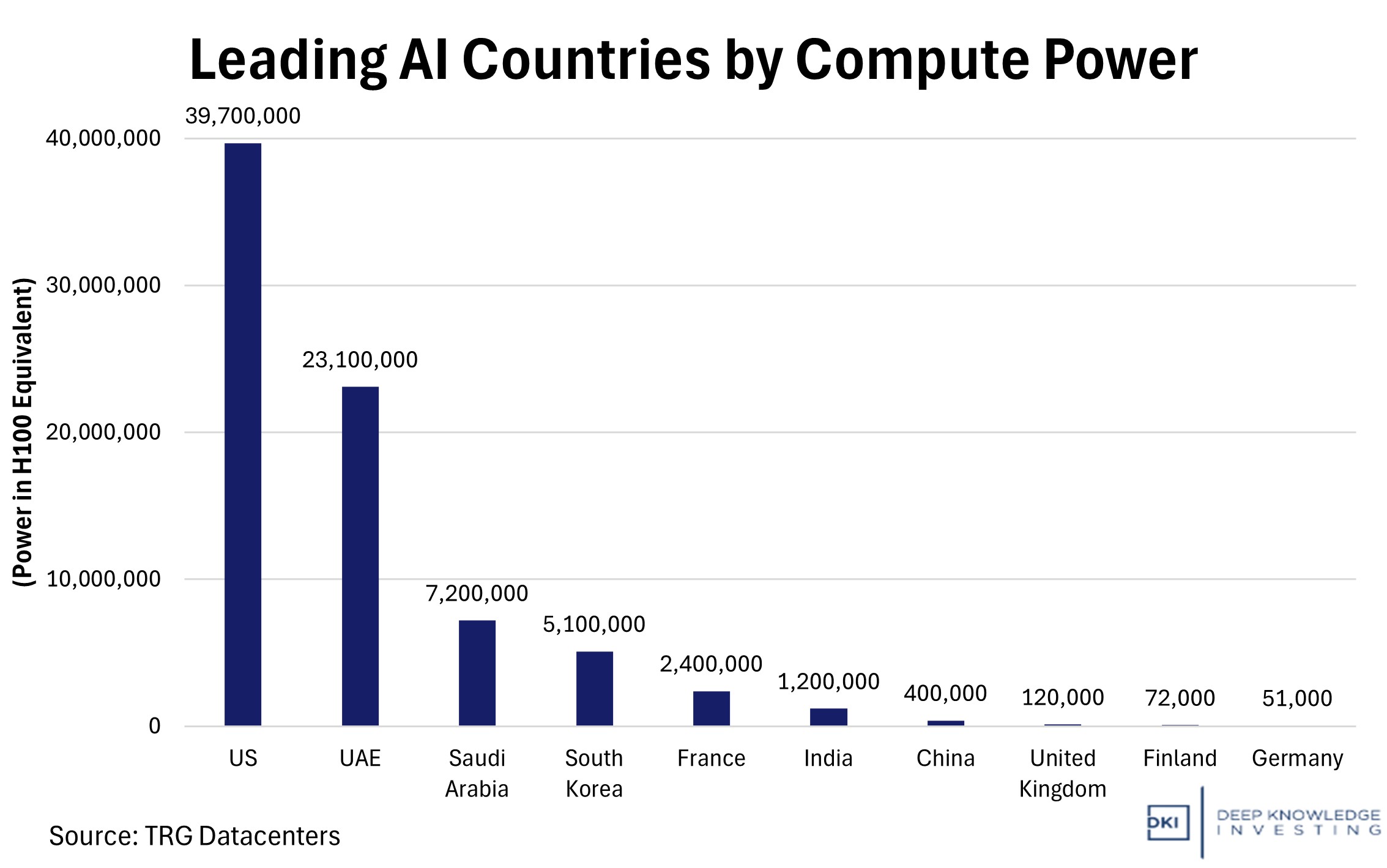

Abu Dhabi is rapidly positioning itself as a major global AI player through an investment strategy centered on its state-backed investment vehicle, MGX. MGX is targeting more than $100 billion in assets under management and plans to spend up to $10 billion annually on strategic AI investments and infrastructure. The company has taken stakes in both Anthropic’s recent $30 billion Series G funding round, which valued the Claude developer at about $380 billion, and is in talks to back OpenAI’s large funding efforts. It also participated in joint ventures and infrastructure projects tied to U.S. computing capacity. These moves signal Abu Dhabi’s intent to bridge capital, technology, and infrastructure by linking sovereign wealth with cutting-edge AI development.

Did anyone expect the UAE to be that big and China to be that small?

DKI Takeaway: By aligning with the dominant U.S. AI companies rather than building indigenous models from scratch, MGX is importing technological leadership while exporting capital, creating a powerful hybrid model of influence and potential return. AI is no longer solely a Silicon Valley story. Second, the scale and coordination of these deals underscore how AI is evolving into a geo-strategic asset class, where national wealth funds, private capital, and tech incumbents co-invest at unprecedented scale. The size of these commitments raises questions about valuation discipline and execution risk. Even with strong strategic alignment, Abu Dhabi will need measurable returns to justify this commitment.

3) Japan to Invest in U.S. Energy and Industrial Projects Totaling $36B:

Japan announced a $36 billion investment in the US representing the first part of a much larger $550 billion commitment. That investment was in exchange for the US lowering tariffs on Japanese imports to 15%. The deal covers three specific projects: a $33 billion natural gas power plant in Portsmouth, Ohio, a $2.1 billion investment in the Texas GulfLink deepwater crude oil export terminal, and a $600 million synthetic diamond grit manufacturing facility in Georgia. The Ohio gas plant would operate at 9.2 gigawatts of capacity, making it the largest gas-fired power generation facility in the world and equivalent in output to nine nuclear plants at full capacity. Under the financial structure, Japan will receive 50% of cash flows until it recoups its principal, after which it will receive a perpetual 10% return.

Japanese capital matters to the US. Now add in the carry trade.

DKI Takeaway: After nearly a year of constant criticism from fiat economists, President Trump’s tariff threats are leading to real infrastructure gains. By threatening higher tariffs on Japanese exports, he’s secured for the US billions of dollars of energy infrastructure spending, something that’s crucial for US economic growth and lower consumer utility bills. The deal has upside for Japan as well. The country is a large energy importer as they have no natural gas or oil production. They’re obvious buyers for natural gas out of Portsmouth and crude out of the GulfLink terminal, locking them into a long-term relationship with the US beyond this investment. From Japan’s perspective, this would help to ease their reliance upon the Middle East, which currently accounts for over 90% of its crude. Shifting supply to an ally like the US would help Japan reduce political risk. On Friday, the US Supreme Court struck down some of the President’s claimed tariff authority. How that will affect previously-agreed investment deals is not clear at this time.

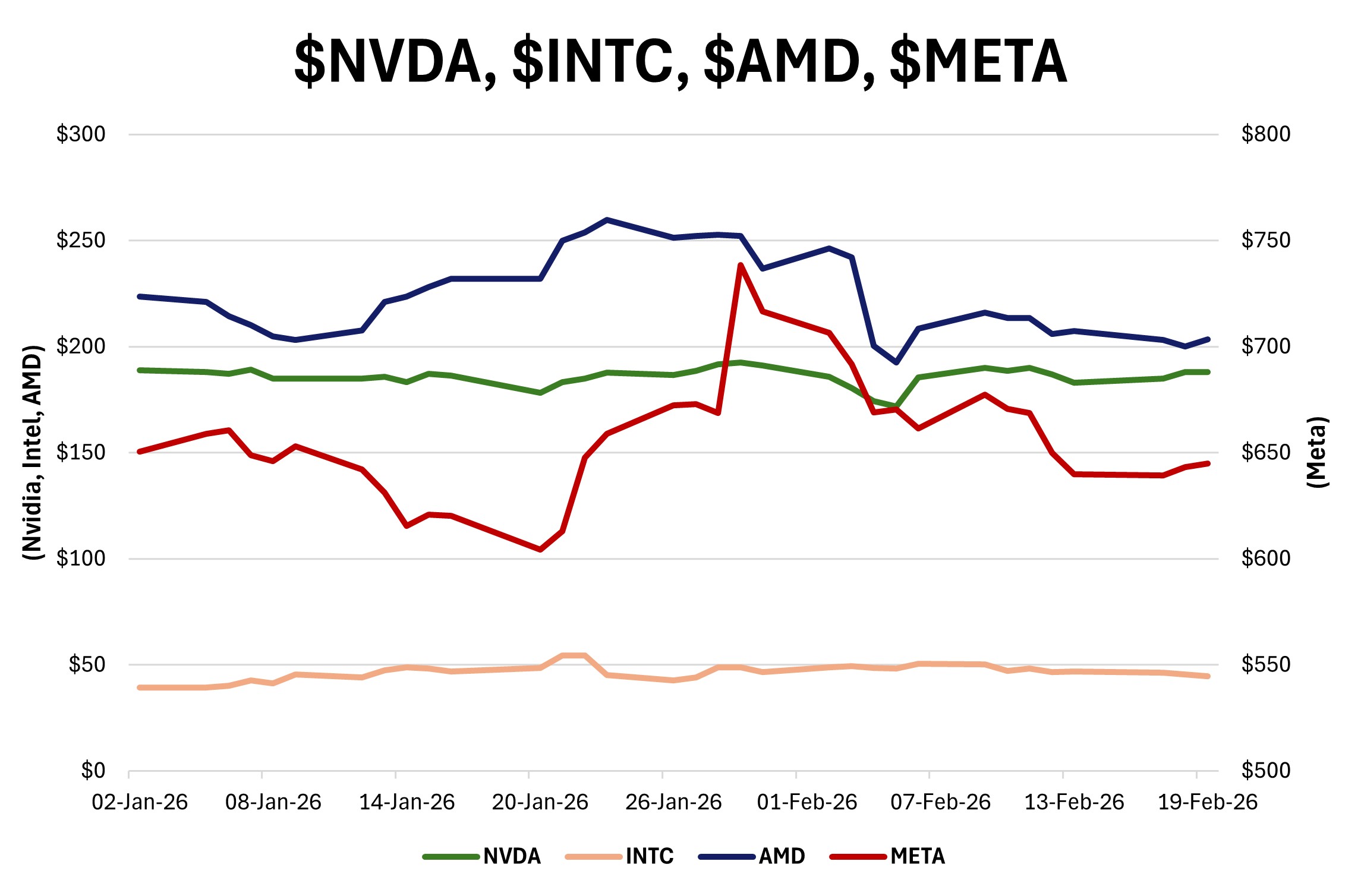

4) NVDA, META, INTC and AMD; A Deal with Widespread Implications:

Last week, Nvidia $NVDA announced it would develop chips for Meta $META datacenters based on $ARM technology. Some analysts think this is a threat to Intel $INTC and $AMD. That concern is valid. Intel and AMD produce chips based on the x86 architecture. ARM technology is more mobile-optimized and tends to have a lower power draw. The downside to the ARM processors is compatibility with existing applications. Nvidia and Meta are making a bet that the newly developed processors can handle an AI workload and will have reduced power requirements; something Meta wants for its datacenters. In recent years, Intel has made huge improvements in this area with its Core Ultra chips that have a combination of E Cores and P Cores to ensure a high power draw only when necessary. Complicating the analysis, we note that Nvidia just invested $5B in Intel and sold its ARM stock. Nvidia is also working with Intel to develop combined CPU/GPU chips.

Wall Street’s response to the deal was muted.

DKI Takeaway: I’ve been doing extensive research calls in the semiconductor industry and have been talking to people who have worked in the field (including at Intel) every week. Many of them believe that the AI business will move from training to inference. In training, Nvidia has a massive lead and even if someone were to develop chips as good as the Nvidia ones, they won’t have the native CUDA instruction set that has embedded Nvidia in everyone’s datacenters. However, if the market shifts to inference, Nvidia no longer has a lead. In addition, in inference, much of the workload will shift back to CPUs from GPUs. So, while some are (reasonably) concerned that x86 could lose share to ARM, it’s also possible that in the future, Nvidia GPUs could lose share to x86 CPUs. If this topic is as interesting to you as it is to me, check out our (non-paywalled) piece with more details on the deal.

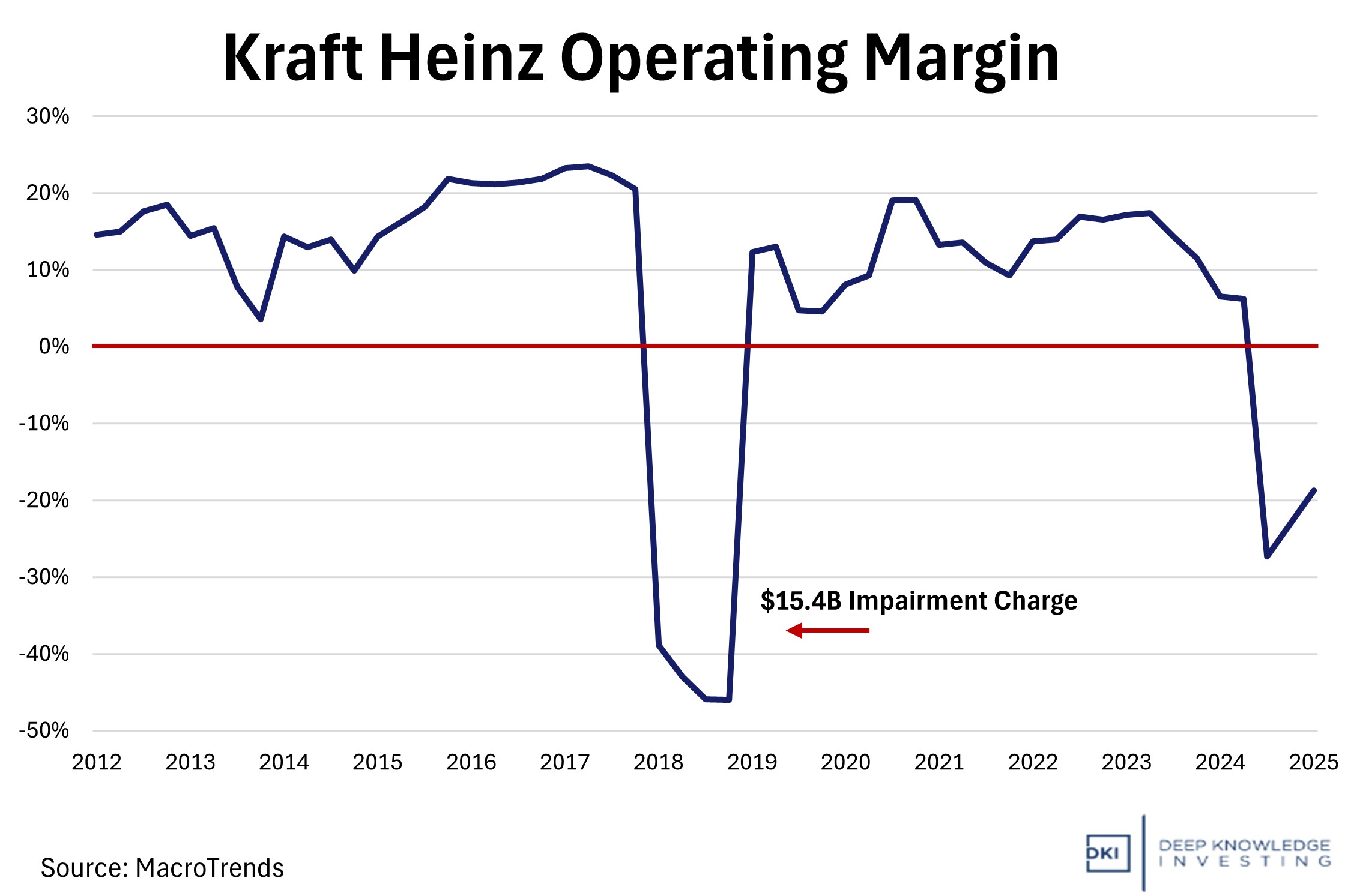

5) Kraft Heinz Puts a Halt to its Planned Breakup:

Kraft Heinz halted its planned breakup into two independent companies. The split was announced in September, 2025 after years of weak growth and underperformance almost a decade after a 2015 merger that created the combined food giant. The breakup was intended to separate its growth brands from its traditional grocery and staple products in order to simplify the business and unlock value. The newly appointed CEO, Steve Cahillane, decided to pause the separation indefinitely; suggesting that the more pressing issues lie in operational performance which was weakening demand and consumer responses to price hikes. He argued that these challenges are “fixable and within control.” Kraft Heinz is now reallocating resources toward revitalizing its core business as management unveiled a $600 million investment program aimed at marketing, product development, and pricing strategy.

Lots of room for improvement.

DKI Takeaway: Rather than splitting, Kraft Heinz positioned itself for a restructuring attempt. The focus shifts to execution risk related to whether pricing and marketing investment can stabilize volumes and margins. The move also reflects a broader market theme; that operational discipline can create growth that restructuring sometimes can’t.

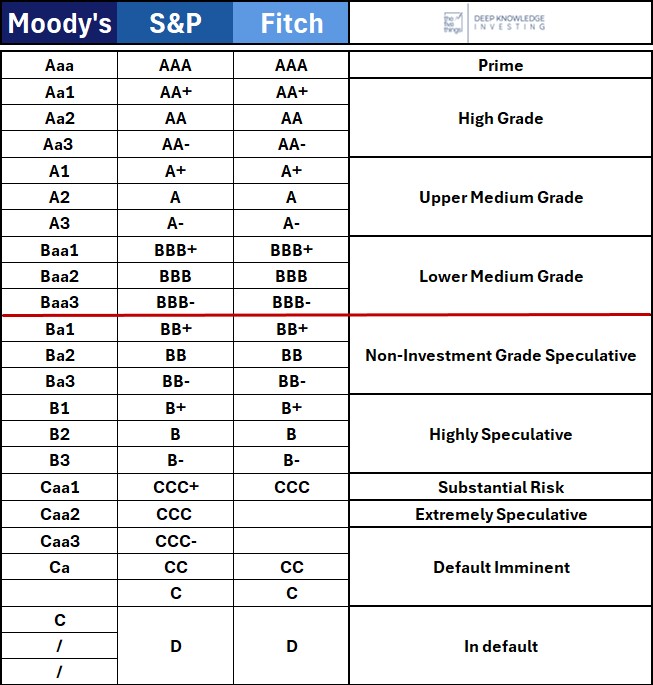

6) Educational Topic: Investment-Grade vs. High-Yield Debt:

Investment grade and high yield debt are two broad categories of bonds that differ according to the credit rating of the borrower. Investment grade bonds are issued by companies or governments considered financially stable and at low risk of default. They carry credit ratings of BBB or higher from agencies like S&P and Moody’s. A bond issued by Apple or the US Treasury would sit comfortably in this category. Because they are seen as safer, these bonds offer lower interest rates. This is also why we call the US 10-Year Treasury Yield the “risk free rate”, since it’s the interest offered on a safe investment.

High yield bonds, sometime known as junk bonds, are issued by borrowers with weaker credit profiles, rated BB or below, and carry a higher risk of default. Think of companies with high/unsustainable levels of debt, startups, etc. To compensate investors for taking that additional risk, these bonds offer higher interest rates. The tradeoff is straightforward: investment grade offers stability and lower returns, while high yield offers higher potential returns in exchange for greater risk.

The ratings agencies are paid by the companies they evaluate.

DKI Takeaway: In general, the tradeoff between risk and return holds in the bond market. However, we’d like to point out that the rating agencies are paid by the companies they evaluate. The conflict of interest is clear and hasn’t been addressed since the 2008 financial crisis. If you’re going to commit capital, we strongly recommend not relying on the ratings agencies, and instead, taking a look at what you think the cash flow of the underlying company will be over the life of the bond.

Information contained in this report, and in each of its reports, is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied. DKI makes no representation as to the completeness, timeliness, accuracy or soundness of the information and opinions contained therein or regarding any results that may be obtained from their use. The information and opinions contained in this report and in each of our reports and all other DKI Services shall not obligate DKI to provide updated or similar information in the future, except to the extent it is required by law to do so.

The information we provide in this and in each of our reports, is publicly available. This report and each of our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion in this and in each of our reports are precisely that. Our opinions are subject to change, which DKI may not convey. DKI, affiliates of DKI or its principal or others associated with DKI may have, taken or sold, or may in the future take or sell positions in securities of companies about which we write, without disclosing any such transactions.

None of the information we provide or the opinions we express, including those in this report, or in any of our reports, are advice of any kind, including, without limitation, advice that investment in a company’s securities is prudent or suitable for any investor. In making any investment decision, each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable, based on this or any of its reports, or on any information or opinions DKI expresses or provides for any losses or damages of any kind or nature including, without limitation, costs, liabilities, trading losses, expenses (including, without limitation, attorneys’ fees), direct, indirect, punitive, incidental, special or consequential damages.