Overview:

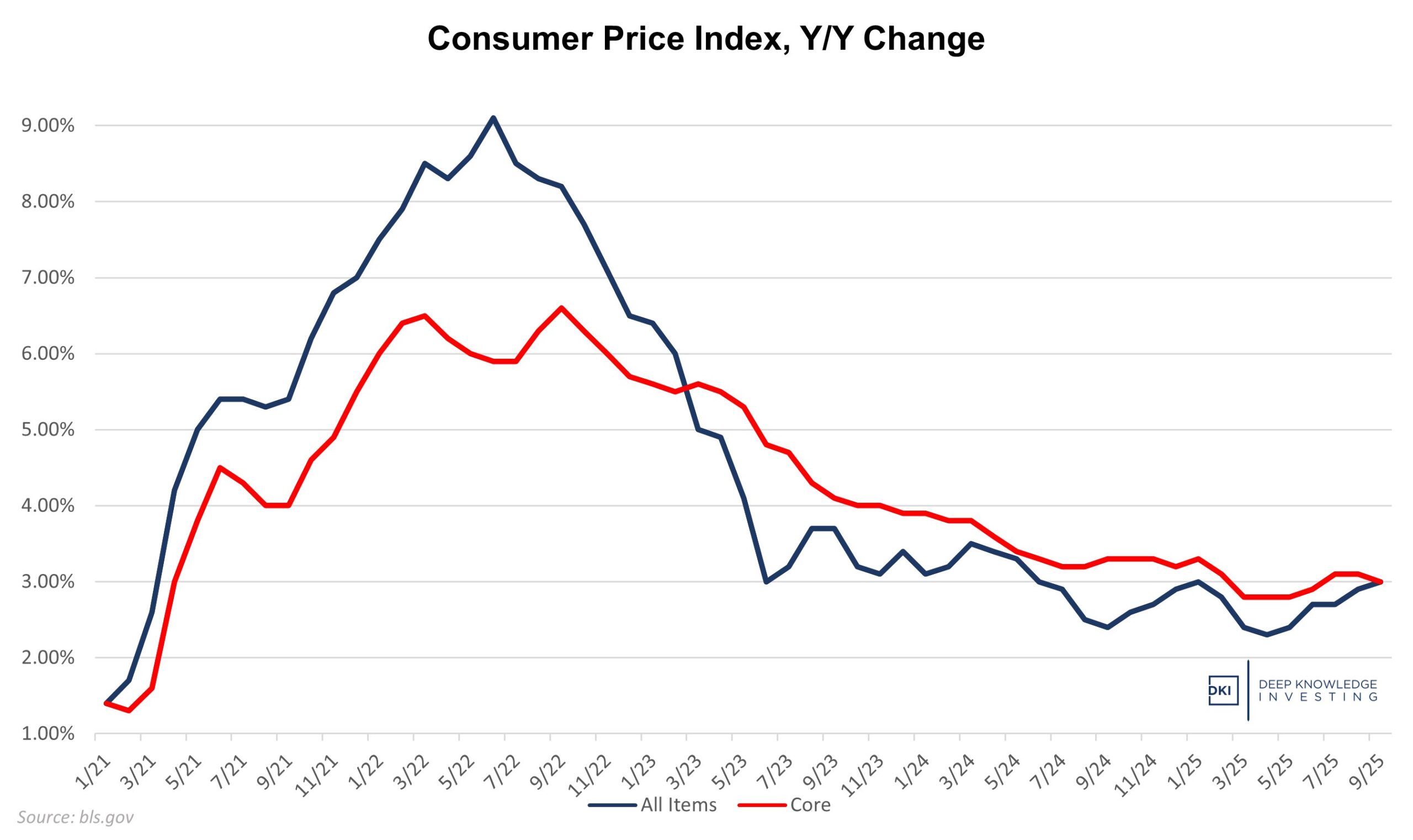

Today, we got the September Consumer Price Index (CPI) report which showed an overall increase of 3.0% for the last year and up 0.3% for the month (annualizes to 3.7%). The annual number is up 0.1% from August and 0.1% below expectations. The monthly is up 0.3% and 0.1% below expectations. The Core CPI which excludes food and energy was up 3.0% vs last year and up 0.2% for the month. These were both 0.1% below expectations. The Core number was 0.1% below last month signaling disinflation (although still too-high inflation). Let’s go through the details:

All-items up 0.1%. Core down 0.1%. Both below expectations.

Still below 2%. The Fed is not as “restrictive” as many claim.

Food:

Food inflation came in at 3.1%, roughly consistent with last month and well above the recent 1% -2% numbers that I thought were understated. Food at home was up 2.7%, consistent with last month. Food away from home is now up 3.7%, slightly below last month. The monthly increase was 0.2% from last month with the longer-term trend up as well.

We continue to note that both the rate of increase and price levels for food purchases are creating problems in many homes. Simply stated, even if food prices stop rising, the current level remains too high for many families. Using buy now pay later for groceries has become common. This category continues to create stress for consumers.

Energy:

Energy was up a big 1.5% vs last month largely due to improved global growth expectations and geopolitical stress. Gasoline was down 0.5% vs last year, fulfilling one of President Trump’s big campaign promises, but the monthly increase was 4.1% and took over the title of biggest contributor to the CPI increase from perpetual leader, shelter. Fuel oil was up 4.1% partly reflecting efforts from the White House to further limit supply from Russia partly by pressuring India. India is resisting that pressure and is drifting closer towards Russia and China, an outcome the White House can’t be happy to see.

Vehicles:

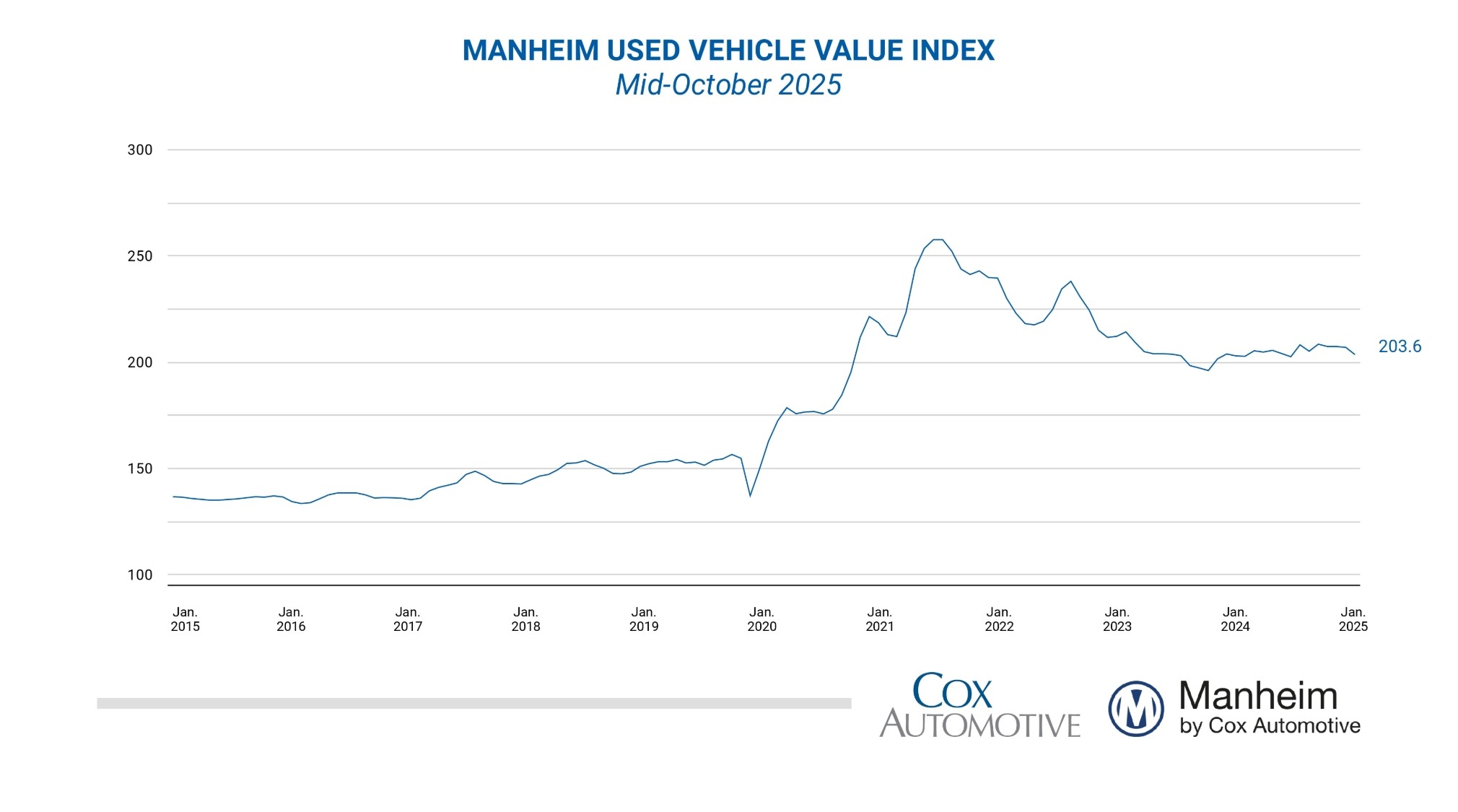

New vehicle pricing was up 0.2% for the month and up only 0.8% y/y. The monthly changes there have been very small for almost all of 2025. Used vehicle pricing was up a big 5.1% and down 0.4% vs last month. The trend here has been inconsistent. After years of volatility, car prices have reached a more stable plateau (although one well above the pre-Covid levels). There’s also a substitution effect. As new cars become increasingly unaffordable, that increases demand and pricing for used cars. I’m reading stories of new car lots that are having difficulty moving high-priced inventory and increasing numbers of consumers falling behind on expensive car loans.

That plateau is looking permanent.

Services:

Services prices were up 3.5%, almost the same as last five months (the definition of “sticky”). Much of the increase has been caused by higher wages. The labor picture is difficult to analyze right now because the data being provided is inaccurate. (I’m newly amused by the analysts who complained the data was bad and now complain that due to the government shutdown, they’re not getting employment “data”.) The same people whose work resulted in revisions of 258k, 818k, 832k, and 911k jobs are saying that President Trump replacing the head of the agency will lead to a loss of integrity and trust. No – the bad data has led to a loss of integrity and trust. Replacing the people involved is a step in the right direction.

It’s also worth noting that recent decreases in jobs have been partially caused by decreases in government positions. While DOGE wasn’t able to do everything they wanted to do, any shift from the government to the productive private sector is welcome. The government shutdown may accelerate this trend depending on the outcome of a few lawsuits.

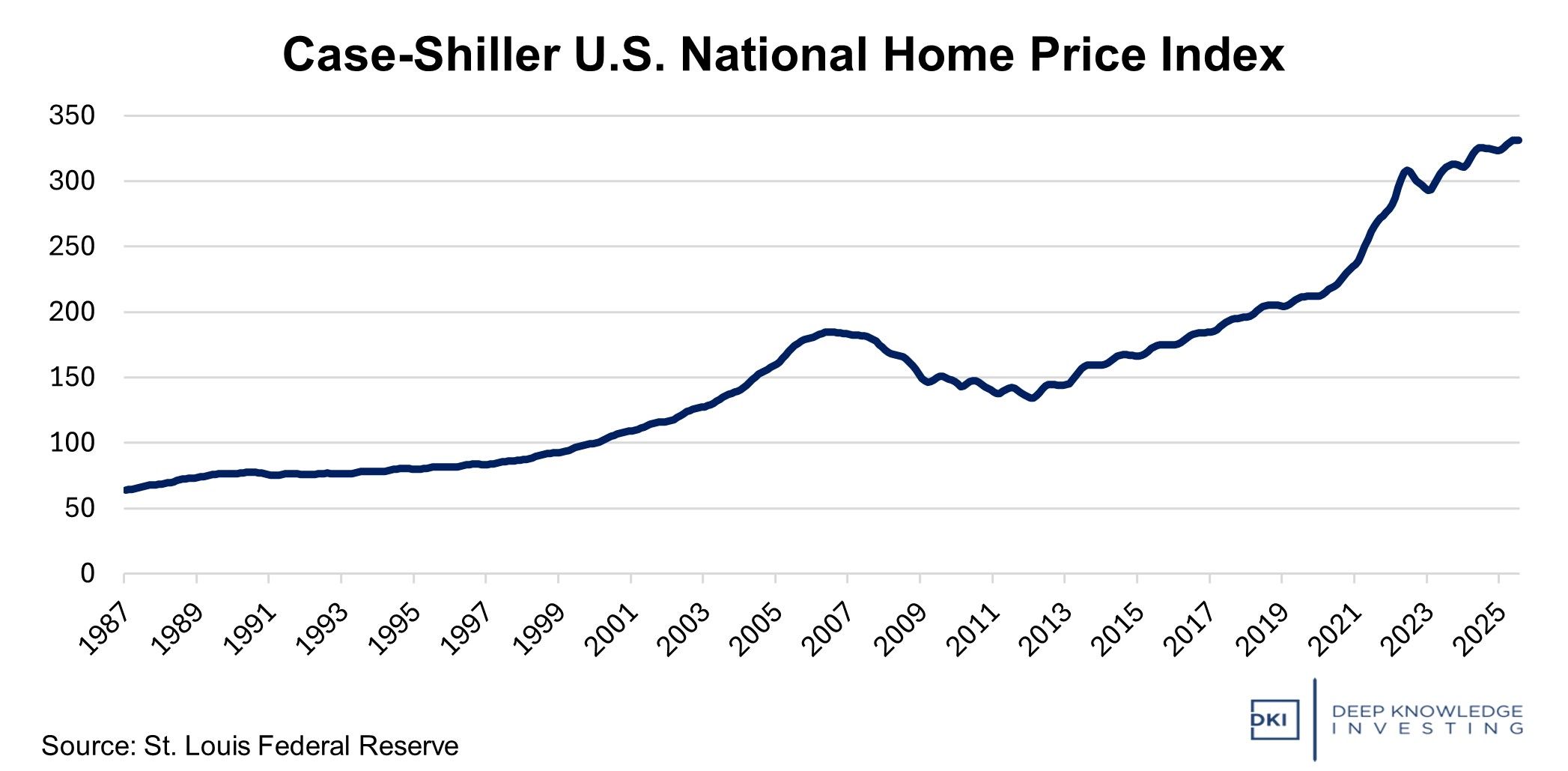

Shelter (a fancy word for housing) costs were up 3.6% which was consistent with last month and for the first time in years was no longer the largest factor in the all-items monthly increase. I’m seeing reports of weakness in several large local housing markets, but the overall trend has been continued increases in shelter prices. Worth noting: Because it takes a few months for housing sales to move from contract to completion, this data tends to lag by a comparable time period. As the data from these weaker markets slowly make their way into the Owners Equivalent Rent (OER) calculation, the primary reason for CPI increases will turn negative.

Still up but replaced by gasoline as the primary reason for the CPI increase.

Conclusion:

Despite all the predictions of catastrophe from fiat economists relating to the Trump tariffs, disaster simply hasn’t happened. We were warned the tariffs would lead to massive inflation. That then got altered to a big one-time increase in the price level which would then be stable. Then, there were threats that tariffs would lead to decreased trade and a worldwide recession. None of that has happened. Some fiat economists have reasonably said that it might take a while for the higher tariff prices to work through complicated supply chains, but if we don’t see that in the October report, the honest ones should start admitting error.

In my opinion, the CPI and the Core CPI are still too high, but the lagging OER metric means that current CPI levels may be lower than reported. (I know – I’ve been one of the people telling you the CPI was overstated for years. Housing costs may be swinging that pendulum slowly in the other direction now.)

DKI has been tracking planned investment in US manufacturing since “liberation day” and the numbers are staggering. Even if foreign goods become more expensive, increased domestic supply will help. The current 40-50 year trend of outsourcing is unsustainable and has led to a national security problem where China can influence US foreign policy by withholding rare earth elements necessary for production of autos, technology, and weapons.

I have a long macro update think-piece that’s been released. In that piece, I make predictions for both long-term and short-term inflation. The DKI portfolio is well-positioned for long-term inflation, and owning Bitcoin and gold is the easiest way to profit from the continued debasement of the money supply (which will continue with or without tariffs). These are two of my largest positions and both have produced meaningful portfolio profits. Recent short-term volatility grabs headlines, but is unimportant.

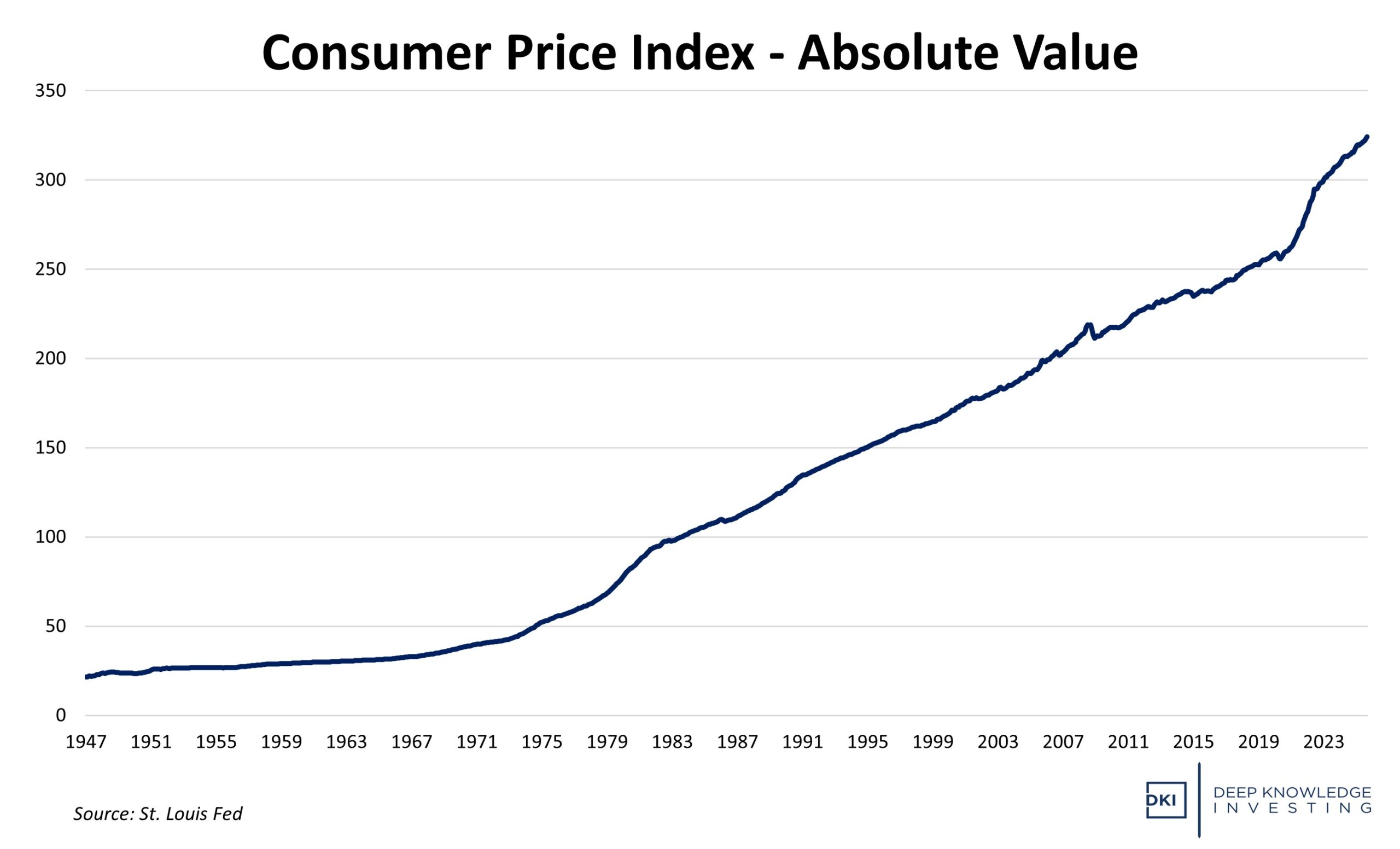

Washington DC has tried to get people focused on disinflation (a reduction in the rate of inflation). This chart shows why most Americans are experiencing more financial distress.

We continue to see signs of increasing consumer credit stress. As buy now pay later loans are being reported to credit scoring agencies, many Americans are seeing their FICO scores fall. Credit card and auto loan delinquencies are increasing. Those with student loans are now again responsible for making payments and leading to further decreases in credit quality for millions. We’ve seen reports from those with student loans complaining that they now have to reduce discretionary spending because the multi-year break from payment requirements has expired. It’s interesting that so many chose to spend this temporary break from payment requirements rather than save or invest the money. Our culture needs to have a change in our relationship with spending and debt. That change should start in Congress. (This section is unchanged from last month because these kinds of slow-moving, but important trends rarely change from month-to-month. We don’t have a “new” economy every four weeks.)

The Fed will lower rates at the next meeting and as I write this, expectations for more rate cuts are indicated in pre-market trading. The one thing our government doesn’t want to acknowledge is without making difficult choices regarding spending tradeoffs (something that isn’t going to happen), they’re going to continue overspending. No matter what the Fed does, we’ll see higher long-term inflation. An accommodating Federal Reserve can only accelerate the trend. To that end, they’re ending quantitative tightening. As you invest, try thinking about inflation as the loss of purchasing power of your dollar. And if you’re planning for retirement, think about whether your dollars will buy as much as you’re accustomed just a few years in the future. The Fed has quietly changed the 2% inflation target to a 3% – 4% range. Start incorporating a higher inflation rate into your long-term planning.

IR@DeepKnowledgeInvesting.com if you have any questions.

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.