As a reminder, I’m using the new shorter format here. I think the previous 9-10 page commentary was helpful when I started writing it every month, but is no longer serving us well. The CPI report does matter, but it’s not driving markets like it did in ’22, ’23, and ’24. In addition, the economy doesn’t change completely from month to month so much of my commentary would get copied and pasted from the previous month. That meant DKI readers were getting 9 pages of content with approximately 3 pages of new analysis and 6 pages of carryover from previous months. I’m going to shift this to a shorter bullet point format in an effort to give you a better signal to noise ratio. The goal is to reduce your reading time while limiting commentary to whatever is new/different/important. Feedback from readers has been positive so I’m keeping this format for now.

CPI of 3.5% was far below expectations of 3.8% and a big decrease vs last month’s 4.2%. The monthly change of -0.4% is the biggest decline in years and was much better than estimates of -0.1%. (Annualizes to 4.9%.)

Core CPI of 2.6% was below estimates of 2.8% below last month’s 2.9%. The monthly change of 0.0% was better than estimates of 0.2% and last month’s 0.2%. The huge difference this month between CPI and Core is due to energy which was not a surprise.

Food was up 3.0% and a more reasonable 0.2% for the month. I’ve been saying forever that this category has been understated and we’re seeing increases. Note that some fertilizer isn’t coming through the Strait of Hormuz and food depends on fuel for tractors and transportation. This is a geopolitical and energy-related increase. I’m still seeing constant posts from waiters that if you don’t want to tip 25% – 30%, you don’t deserve to eat out. Food at home remains much cheaper than eating at a restaurant so between inflation and escalating tipping demands, it will be interesting to see if people start to eat at home more often.

Energy up 15.7% but down 5.7% vs last month. Gas up 26.7% but down 9.7% vs last month. Fuel oil up 42.9% but down 9.2% vs last month. This is (again) the whole CPI report here. Decreases in energy costs vs last month are the reason for the lower-than-expected June CPI. We know the reason. I have said all along that I don’t expect a quick solution to the situation in Iran. I believe the key issue is that there isn’t overlap between acceptable end conditions for the Iranian Mullahs and President Trump making any ceasefire temporary. This was a point I made on June 25th in a (non-paywalled) article titled “A Personal Note” and reiterated a week later in another article titled “Are Oil Prices Really that High”. Please feel free to check those out alongside this week’s announcement from President Trump that the ceasefire is over and declaring the official resumption of hostilities. As before, DKI owns assets that benefit from inflation and we have a substantial energy portfolio.

New vehicle prices were flat for the month and up just 0.5% vs last year. Used vehicle prices were down 0.2% vs last month and down 1.8% vs last year. That’s a plus although it could indicate that consumers are tapped out and holding off on buying a new (used) car.

Shelter (housing) up 3.3% and up 0.1% for the month. This remains a high and increasing category accounting for much of the CPI increase both this month and for the past half decade.

The market was down early on weak results from IBM, but rose rapidly on today’s lower-than-expected CPI numbers. Multiple people who I respect are saying the Federal Reserve will cut rates soon. I don’t agree with that. While it can be appealing to look at the Core number when energy prices are this volatile, even that 2.6% is too high and above the official Fed target. I tend not to focus on Core because energy and food are real costs for Americans. The employment situation remains good. The economy hasn’t gone into recession as the fiat economists who incorrectly said tariffs would lead to doom claimed. I think today’s cooler CPI report means the Fed won’t hike as many expected following the conclusion of the most recent meeting. However, with a still-high CPI and higher oil prices concurrent with the resumption of the war, it’s hard to see them cutting at the next meeting.

I also think it’s worthwhile to take a look at how the press distorts reporting on these issues. This sentence was in a morning email sent from Barron’s, “The core personal consumption expenditures rate was rising before the oil shock, from 3% in December to 3.4% in May, driven by tariffs, energy prices, and AI infrastructure demand.” The tariffs never led to a big increase in goods inflation that was threatened by economists. The war in Iran did lead to higher energy prices although not nearly as high as most thought (again, check out “Are Oil Prices Really that High”). I also concede that AI infrastructure demand has led to higher consumer goods pricing, something DKI has benefitted from by buying Intel last October.

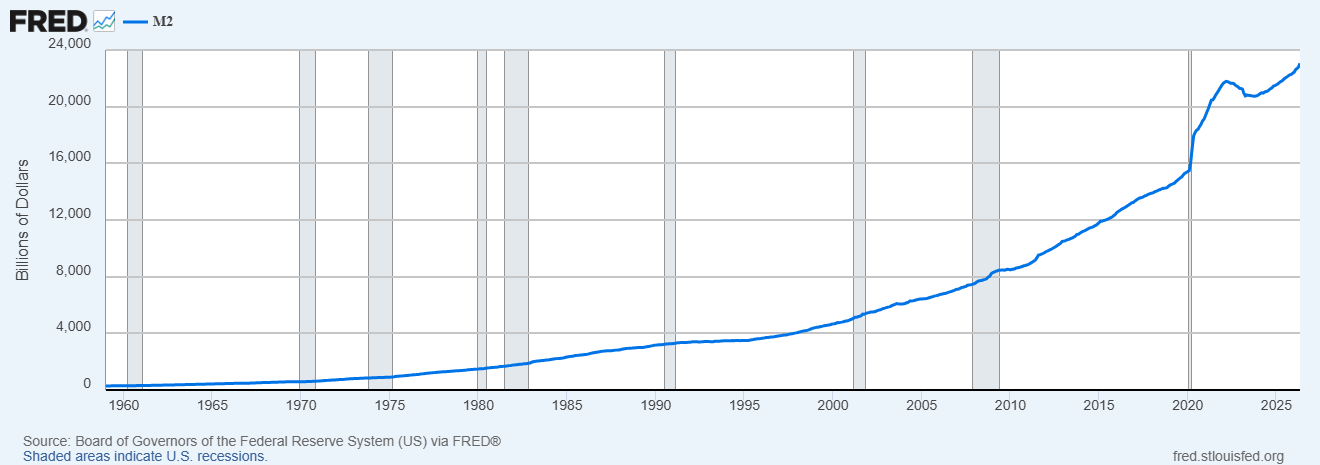

If I agree with most of Barron’s facts, why do I disagree with the conclusion? Check out the graph below. That’s the increase in the US money supply. It’s up 5.6% vs last year. As usual, either most people in the press and in Congress don’t understand economics or they’ve chosen to run interference in order to protect ever-increasing government spending while blaming everything else. The fact that price inflation is below 4% (below 3% for Core) is a gift right now. Most of the finance world is focused on the Fed, but they can’t control increases in spending. Long-term inflation will increase with the debasement of the currency. That’s why the reductions in the fed funds rate over the past couple of years haven’t resulted in a reduction in the 10-year Treasury yield.

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.