Quick announcement: I’ll be in Siem Reap, Cambodia for the next couple of weeks. While I’m here, I’m open to a small number of in-person conversations. If you’re based locally, or know someone here you think it would be worthwhile for me to meet, feel free to reach out privately at IR@DeepKnowledgeInvesting.com.

Also, I was interviewed this week by Marty Bent of TFTC. Marty is a smart Bitcoiner with a great sense of the regulatory and political environment. The episode is on YouTube.

The CPI comes in below expectations, but shelter continues to rise. Even worse, the Owners’ Equivalent Rent calculation makes that category understated. Retail sales were flat in December leading to worries about GDP growth. I’m more worried about production than consumption. DRAM prices skyrocket which will lead to more expensive consumer electronics. Help will come from Samsung…next year. Paramount continues to try to acquire Warner. I think the offer to pay the breakup fee is a little misleading. If your favorite company splits its stock, can you now buy shares more cheaply than before? We explain in this week’s educational topic.

This week, we’ll address the following topics:

- The CPI comes in lighter than expected. Shelter still the big problem. Market yawns.

- US retail sales were flat in December leading to questions about GDP growth. Am I the only one who thinks it’s weird that we conflate spending with producing?

- DRAM prices rise. Expect higher prices for some consumer electronics. Samsung is sending help…eventually.

- Paramount continues to try to break up the Warner Brothers / Netflix deal and steal WB for itself. I think the breakup fee discussion is misleading.

- Do stock splits mean you can buy your favorite company cheaper? Read on and we’ll explain in this week’s educational topic.

Every week, our young interns impress me. Cashen Crowe needed emergency surgery (he’s fine now) and texted me from his hospital bed that he’d still be able to help with this week’s Five Things. Samaksh Jain simply took over, organized this issue, and delivered his usual excellent work. And new intern, Kunal Arora from Rutgers, joined this week and immediately got to work contributing to this edition. Some people need time to settle in and become productive. Kunal clearly thinks warmups are for amateurs. Nice work by all!

Ready for another week of not caring about the CPI? Let’s dive in:

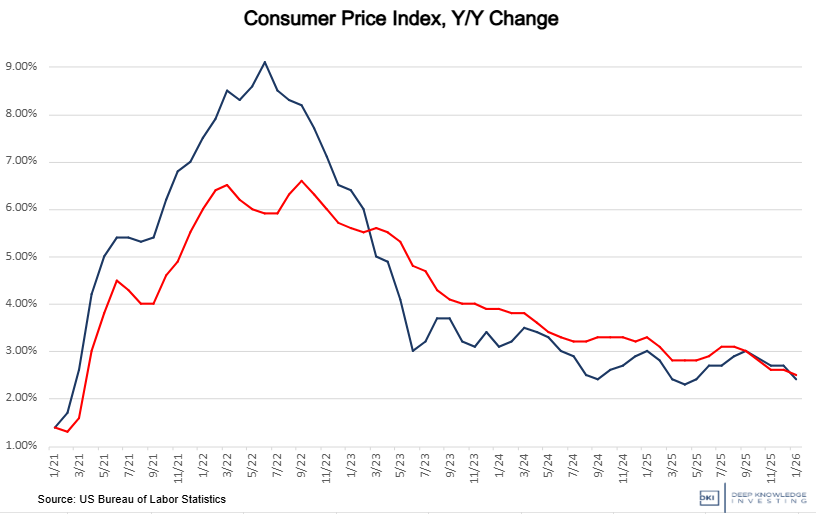

1) CPI Comes in Light – Market is Not Impressed:

We got the January Consumer Price Index (CPI) report which showed an overall increase of 2.4% for the last year. That’s below last month and below the 2.5% expected. The monthly change was 0.2% vs the 0.3% estimate. The Core CPI which excludes food and energy was up 2.5%, consistent with expectations. The Core change was up 0.3% vs last month which annualizes to 3.7% and was consistent with expectation. These numbers remain well above the 2% target and have been so since 2021, but were also down from recent prints. The equity indexes yawned and finished roughly flat. Energy prices provided relief while shelter was (yet again) the main contributor to this month’s increase.

Schrodinger’s inflation. Is the line pointing down, or is it too high?

DKI Takeaway: Despite all the predictions of catastrophe from fiat economists relating to the Trump tariffs, disaster simply hasn’t happened. We were warned the tariffs would lead to massive inflation. That then got altered to a big one-time increase in the price level which would then be stable. Then, there were threats that tariffs would lead to decreased trade and a worldwide recession. None of that has happened. Some fiat economists have reasonably said that it might take a while for the higher tariff prices to work through complicated supply chains, but we’re past the point when this would have happened. If they were more honest, they’d start issuing public mea-culpas. I left this section unchanged from previous months because I’ve yet to see a fiat economist admit their error.

I’m seeing rumors that Kevin Warsh, the nominee to replace Jerome Powell as Chairman of the Federal Reserve, will move the Fed’s inflation target from the current 2% (which is already 2% too high) to 3% (ish). First, it was just two weeks ago that the market panicked because Warsh was supposed to be an ultra-hawk, something DKI disagreed with in writing. Second, that’s no different from the current Fed. We’ve been above target since 2021 and the Fed has already cut 175bp (1.75%). While this month’s CPI was better than recent versions, it’s still too high and the CPI remains understated. I think this is unwise because a continually debased currency has a horrible social and economic impact. Given that this is the direction our government and quasi-governmental agencies are heading, the best thing to do is to prepare your portfolio for continued inflation, something DKI has done.

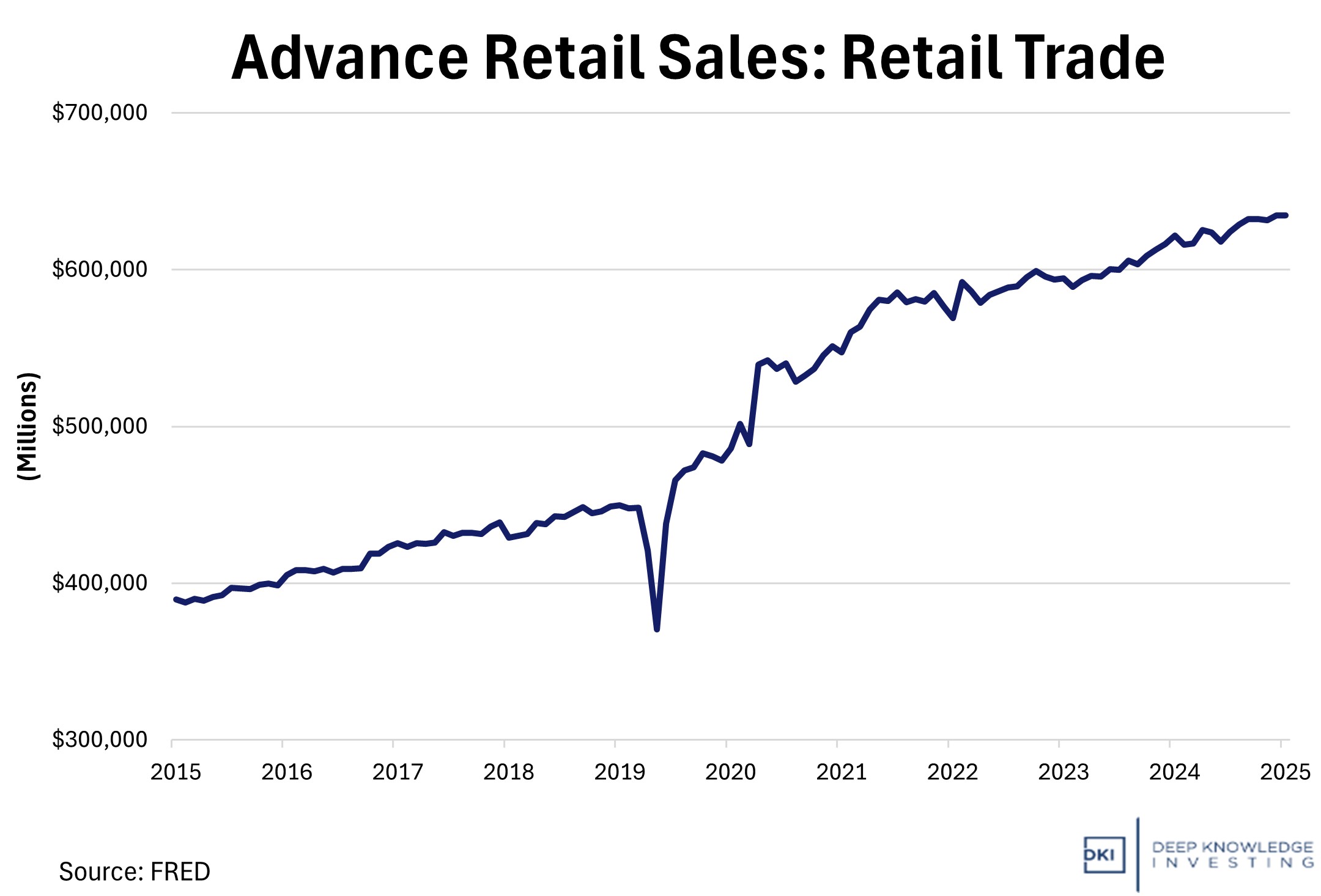

2) US Retail Sales Disappoint in December, Undershooting Expectations:

New data showed that U.S. retail sales were flat in December 2025, an unexpected outcome after a stronger November. This was far short of the 0.4% growth economists had forecast. Total retail and food services receipts remained $735 billion on a seasonally adjusted basis. Core measures, which strip out autos, gasoline, and building, also showed little to no growth. Categories such as furniture, electronics, clothing, and auto sales posted outright declines, while gains were limited to essentials like building materials and food and beverage. The flat result capped a holiday shopping season that failed to deliver the typical year-end boost, and it came alongside revisions to prior months that suggest consumer momentum was weaker than previously thought. Retail sales growth over the full year remained positive but tepid, and several economists pointed to slowing wage growth, low savings, higher prices, and fading consumer confidence as key drivers. Markets reacted to the report with bond yields falling and safe-haven flows gaining. Major equity indexes, especially consumer and financial stocks, moved lower on investor worries that sluggish household spending could weigh on economic growth in early 2026.

While December was flat, the overall trend indicates Americans are still spending.

DKI Takeaway: The flat December retail print underscores a growing reality: the consumer, long the engine of economic growth, is losing steam at the margin. When spending stalls in a month buoyed by holiday purchases, it signals that households are tightening belts amid price pressures, wage gains below real inflation, and economic uncertainty. This isn’t just a December blip; it fits into a pattern of K-shaped consumer behavior, where higher-income households sustain discretionary purchases while the broader base pulls back. For markets, weaker retail activity intensifies debates about the timing of interest-rate cuts, and increases volatility in consumer discretionary and financial names. It also suggests that headline GDP gains, which are heavily influenced by massive AI spending, could mask underlying softness in household spending, discouraging complacency about growth forecasts. I also think there’s something quirky about focusing on consumer spending as economic growth. Real growth comes from saving, investing, and building businesses; not from buying more things.

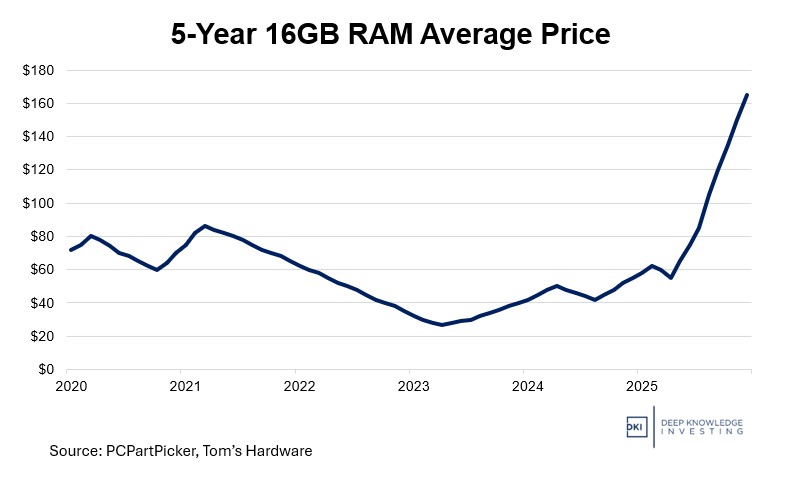

3) The Memory Meltdown:

There’s been a surge in demand for memory (DRAM) that has outpaced supply, with the AI Boom taking the lion’s share of the blame. Some of the biggest companies in the world, like Google, Nvidia, and AMD need immense amounts of DRAM capacity to support the development and implementation of their AI chips. These chips need to store, process, and access billions of parameters and datapoints to create fast responses. The rush of investment from these companies and more has caused DRAM prices to skyrocket. The increasing focus on creating HBM (High Bandwidth Memory) for Nvidia rather than traditional RAM hardware is also contributing to the shortage, as HBM takes up more space resulting in smaller production runs. 16GB of RAM would have cost $60 a year ago. Now, that same RAM costs more than $160. We saw largescale AI development and investment for most of 2025, but the reason prices have spiked in the past two months has to do with inventory reaching critical levels combined with larger orders. In December, Samsung raised their contract prices by another 100%, causing customers to buy more in anticipation of future price hikes intensifying the problem.

Look for higher laptop prices.

DKI Takeaway: Samsung, Micron, and SK Hynix collectively make up over 90% of the global DRAM market, and they’re benefitting from this surge in demand, with their stock prices jumping 201%, 311%, and 331% in the past year. Samsung expects its operating profit to triple for Q4. DRAM is used on some level in every electronic product that exists, meaning higher future consumer prices are on the way. The question is, how much of a margin hit are companies willing to take before they pass on costs to consumers and how quickly can manufacturers increase supply? Samsung has indicated an intention to increase production by 70% with much of that capacity coming on in 2027 and 2028. I’ve been tracking laptop prices and following fantastic deals available during the holidays, prices spiked a couple of weeks ago. There are good deals available on high-end laptops with 32GB memory for Presidents’ Day sales, but these deals are still at higher prices than we saw just last month. Intel is indicating better component availability in 2Q which starts in six weeks, so we’ll be tracking this.

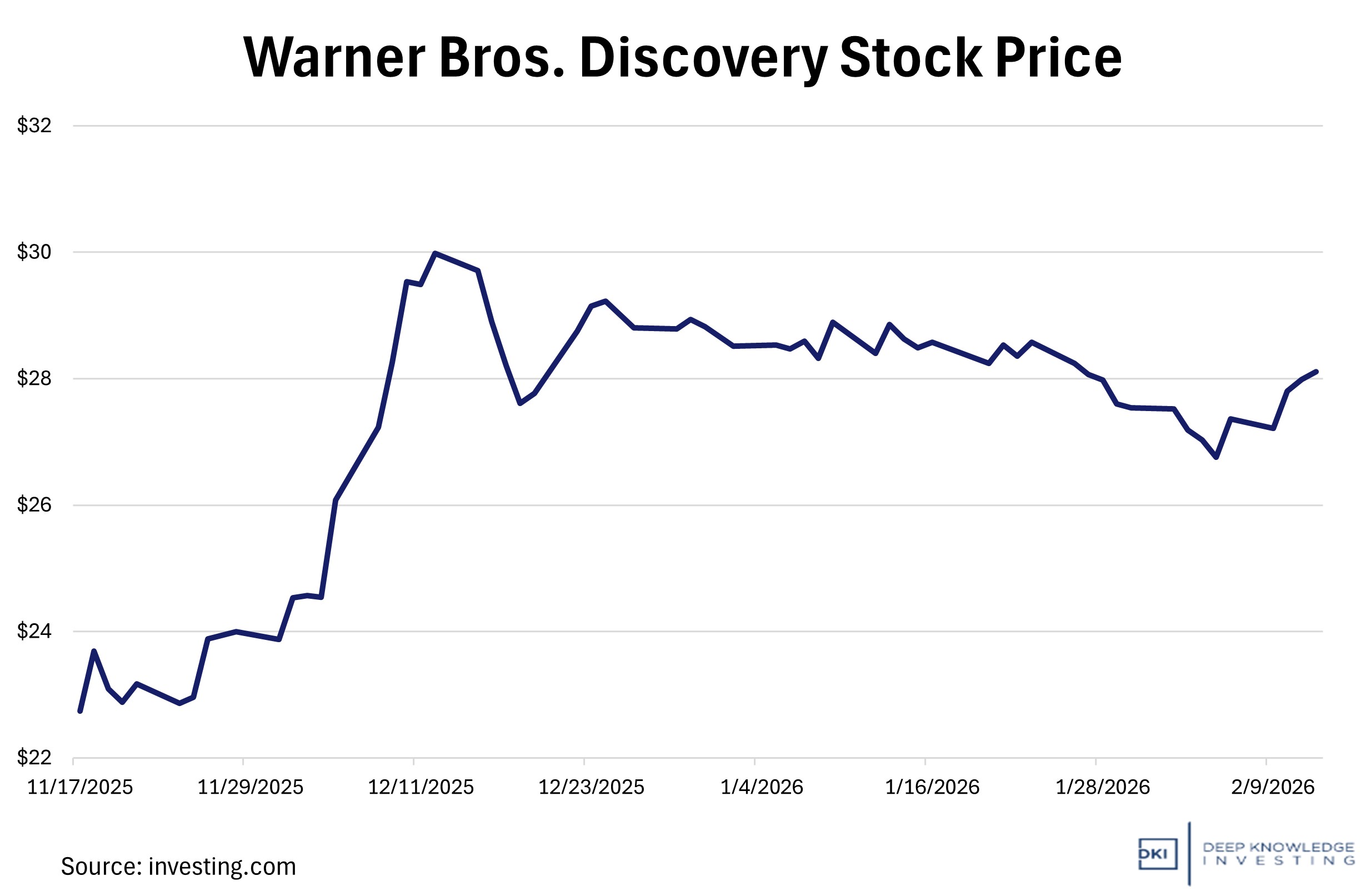

4) Paramount Sweetens Offer in Warner Bros. Takeover Battle:

This week, the bidding battle for Warner Bros. Discovery (WBD) escalated as Paramount Skydance sweetened its $30 per share all-cash offer to counter Netflix’s existing agreement. Paramount added a $0.25-per-share quarterly “ticking fee” (worth roughly $650 million per quarter if the deal extends past 2026) and agreed to cover the $2.8 billion breakup fee Warner would owe Netflix, materially increasing deal certainty and effective value to shareholders. The move is being supported by activist investor Ancora Holdings, which has built a roughly $200 million stake and is publicly opposing the Netflix transaction, arguing it carries greater regulatory and structural risk. While Warner’s board continues to back the Netflix deal, Paramount’s willingness to assume termination risk and Ancora’s pressure have intensified scrutiny ahead of a potential shareholder vote, shifting the focus from headline price to closing certainty and regulatory feasibility.

That’s a big arbitrage spread for a competitive deal.

DKI Takeaway: There’s some sleight of hand happening in the deal terms. Netflix is offering $27.75 in cash for some assets with Warner Brothers’ shareholders getting the remaining assets in a spinout. Paramount is offering $30 cash for all company assets. It’s a cleaner transaction. Which deal is better depends on your view of the assets Netflix isn’t buying. The breakup fee issue is misleading. Offering to pay the $2.8B termination fee to Netflix protects Warner Brothers’ shareholders against the highly unlikely event of both deals falling through and paying two breakup fees. However, if Paramount completes the deal, the economic result of paying the breakup fee is irrelevant. Either way, Paramount would pay $30 in cash. If Warner Brothers pays the breakup fee, Paramount acquires a company with $2.8B less in cash (or additional debt). If Paramount pays the breakup fee, they buy a company with a better balance sheet and then forward the exact same $2.8B to Netflix. I’m a little surprised the arbitrage spread is about 6%. That’s large for a competitive bidding situation and indicates the market thinks the Netflix deal will get done and that the spinout assets have little value.

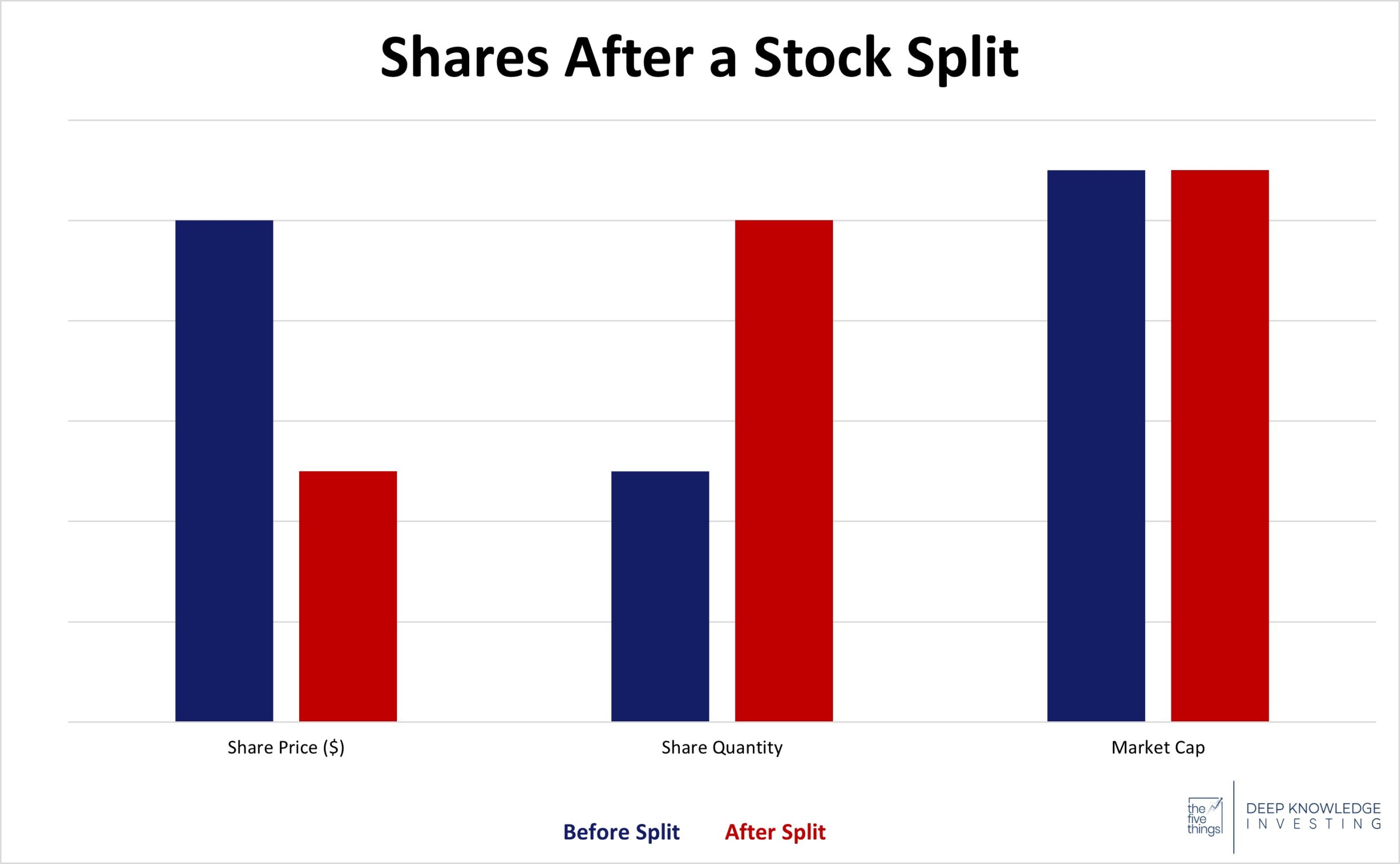

5) Educational Topic: Stock Splits:

A stock split is when a company divides its existing shares into new ones. This increases its total outstanding shares while leaving the market cap unchanged. It’s like if you were to cut 10 slices of cake into 20. You have more slices, but still the same amount of cake in total. Since each share is now represents a smaller percentage of the company, it now costs less to buy an individual share. Companies tend to do this when their stock price becomes expensive enabling smaller investors to buy shares. Nvidia did a 10-1 split in 2024 after trading above $1,200, and more recently, Netflix did the same in November after trading above $1,000. Existing investors will have the same amount of equity in the company. It’s just expressed in different terms.

Cut as many slices as you want, but the pizza is the same size.

DKI Takeaway: While stock splits can make companies seem to be available at cheap prices, it’s important to remember that it doesn’t actually change anything about the prospects of investment. If a stock was overvalued before, splitting doesn’t change that. Your investment calculation regarding a stock’s valuation and prospects would remain unchanged. Some of the newer brokerage firms now offer the ability to buy fractional shares which if universally adopted, would mean stock splits would no longer be relevant.

Information contained in this report, and in each of its reports, is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied. DKI makes no representation as to the completeness, timeliness, accuracy or soundness of the information and opinions contained therein or regarding any results that may be obtained from their use. The information and opinions contained in this report and in each of our reports and all other DKI Services shall not obligate DKI to provide updated or similar information in the future, except to the extent it is required by law to do so.

The information we provide in this and in each of our reports, is publicly available. This report and each of our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion in this and in each of our reports are precisely that. Our opinions are subject to change, which DKI may not convey. DKI, affiliates of DKI or its principal or others associated with DKI may have, taken or sold, or may in the future take or sell positions in securities of companies about which we write, without disclosing any such transactions.

None of the information we provide or the opinions we express, including those in this report, or in any of our reports, are advice of any kind, including, without limitation, advice that investment in a company’s securities is prudent or suitable for any investor. In making any investment decision, each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable, based on this or any of its reports, or on any information or opinions DKI expresses or provides for any losses or damages of any kind or nature including, without limitation, costs, liabilities, trading losses, expenses (including, without limitation, attorneys’ fees), direct, indirect, punitive, incidental, special or consequential damages.