The US and Israel are knocking out Ayatollahs as fast as Iran can appoint them. Did they kill the entire 88-member council that appoints the next one? We don’t know which explains why DKI didn’t make changes to the portfolio this week despite high market volatility. Our long-term thesis explaining why we own Bitcoin, gold, silver, and energy is still valid. Oil prices rose, but stayed below $100 indicating oil traders expect a short(ish) controlled war. Korean markets tanked due to low oil reserve levels. Without consistent power, the world’s DRAM makers will stop working leading to a multi-month lack of supply in an already tight market. Can President Trump provide insurance to oil tankers in the Strait of Hormuz? He’s said he’ll try and has the US Navy backing up the talk. OpenAI raises a record amount of capital and reduces capital commitments by almost a trillion dollars. Has anyone figured out that means almost a trillion dollars less in revenue for the big tech firms? Broadcom guides to $100B in AI chip revenue. The market is starting to value custom TPUs vs Nvidia’s stock GPUs. In our educational topic, we explain when you want to see high fixed cost and when you want to see high variable cost. Excited for a description of operating leverage? Then read on:

This week, we’ll address the following topics:

- Everyone has a post-hoc explanation for everything. Is any of it predictive? What are we doing with the portfolio here?

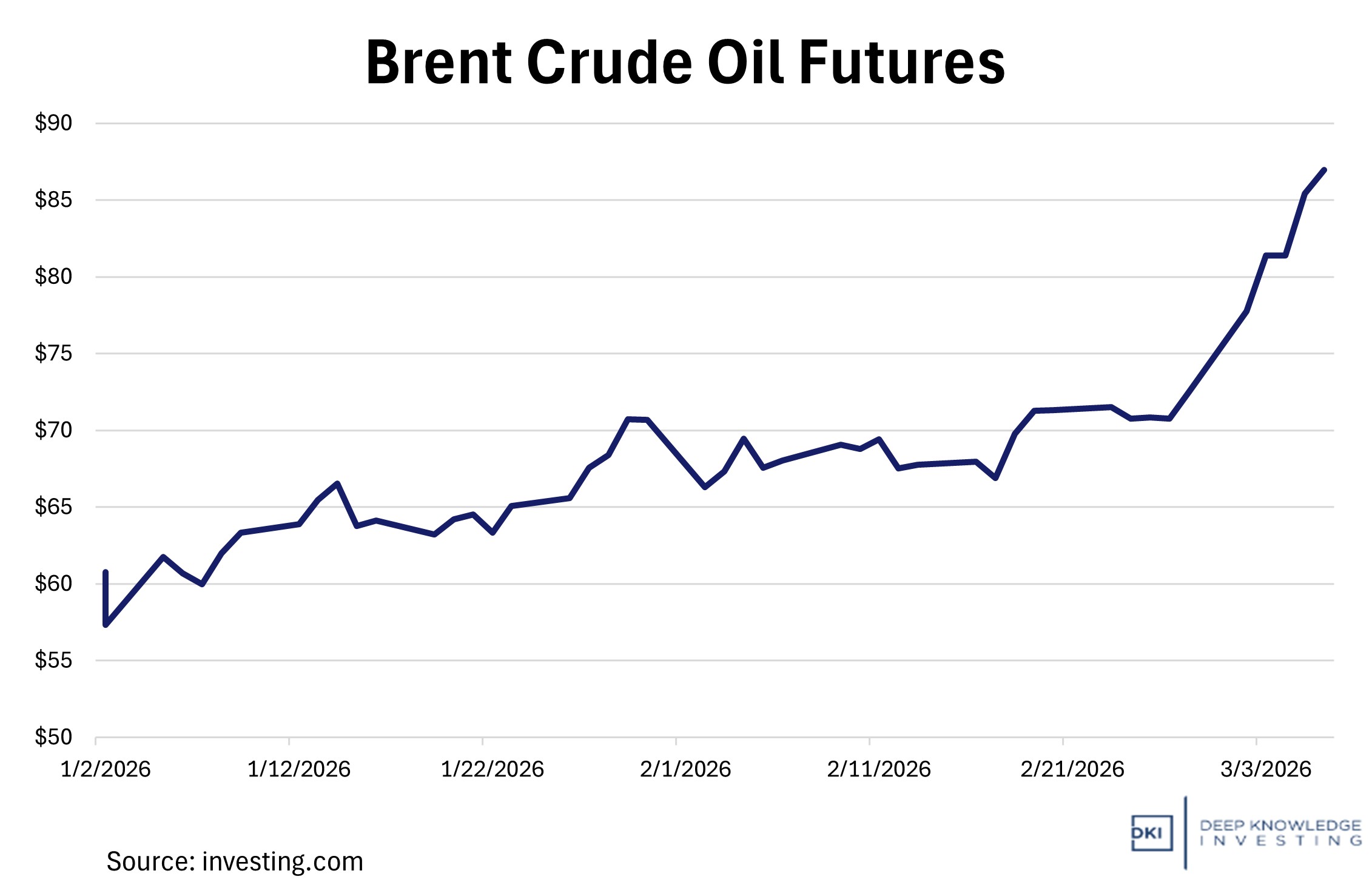

- Oil prices rose by 27% from last Friday to the time of this writing. It could have been much worse. It will be worse if Korea runs out of fuel.

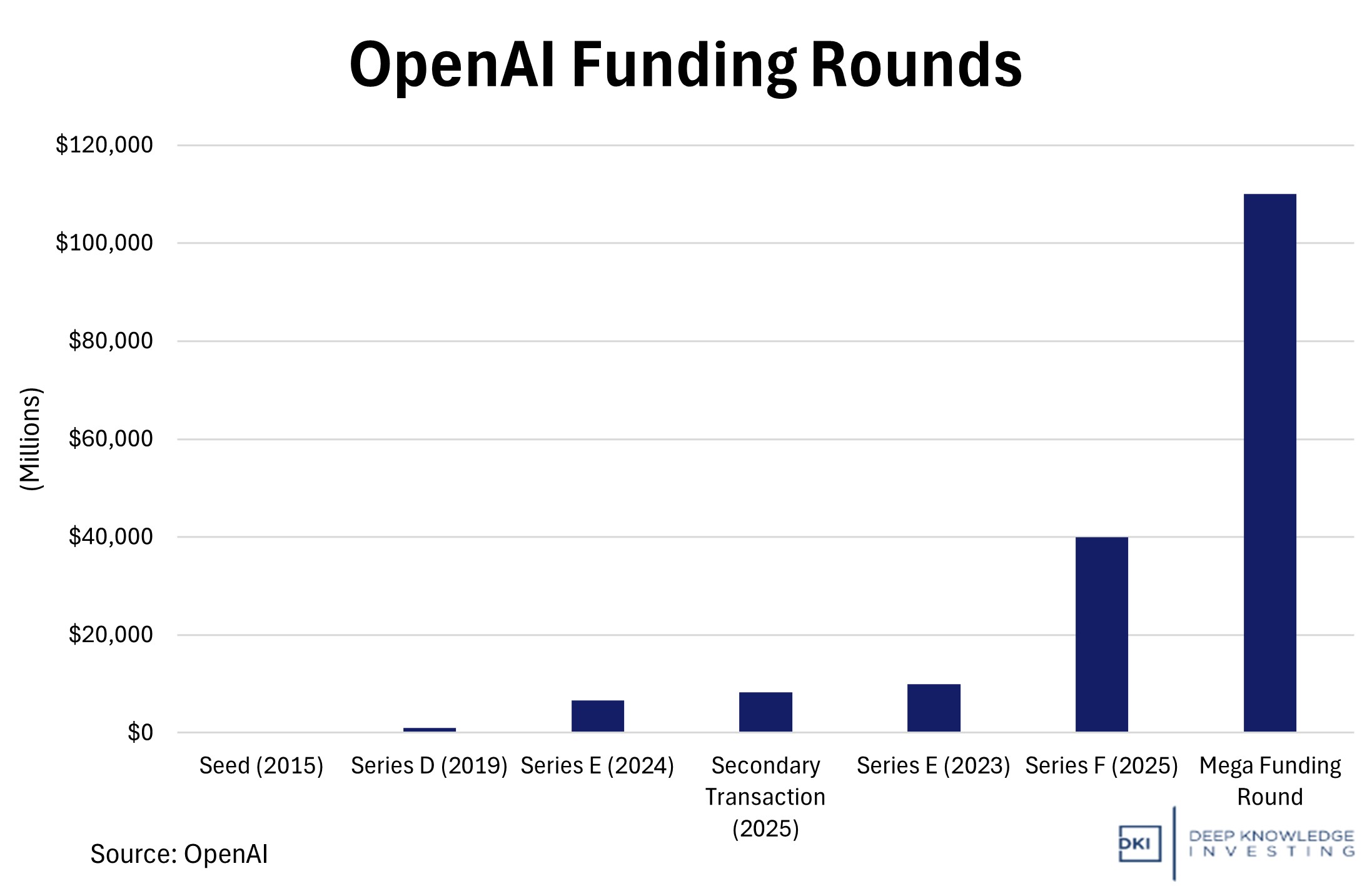

- OpenAI raises a record $110B and cuts its planned spending by $800B. That’s almost a trillion dollars of lost revenue for its business partners. That’s not a positive for future tech stock valuation multiples.

- Broadcom guides to $100B of 2027 AI chip revenue. The company will deliver multiple gigawatts of TPUs (Tensor Processing Units) to hyperscalers who want custom solutions instead of Nvidia GPUs.

- What’s better – high fixed cost or high variable cost. The answer: It depends. We explain in this week’s educational topic.

Cashen Crowe, Samaksh Jain, and Kunal Arora are not in line to be the next Supreme Leader of Iran although it was a good week for Marco Rubio memes. They did their usual excellent job on this week’s 5 Things. Well done, gentlemen!

Ready to find out who the Ayatollah is this week? Let’s dive in:

1) Post-Hoc Analysis:

In my opinion, too much mainstream “analysis” involves fitting an explanation to match yesterday’s events. Early in the week, gold rose sharply leading all of us (including me) to say, “Of course gold rose: It was a flight to safety trade.” When gold fell the following day, we got a lot of additional explanations:

- The dollar was a more liquid flight to safety trade so it strengthened which lowered the dollar price of gold.

- Portfolio managers raising cash to reduce risk tend to sell winners before losers so they don’t have to realize losses. Gold was up 42% in the last 6 months and 75% in the last year so it was early on the chopping block.

- Or my view which is gold was just under $5,200 and up more than 4% in the last month. It’s more than tripled since DKI bought it in 2020 with much of that increase coming in the past year. Short-term volatility is interesting, but not important. The war in Iran is affecting current trading, but not the long-term thesis for the underlying asset.

The above explanations aren’t wrong. They’re just post hoc instead of predictive. (If someone was selling gold on Monday and buying it back at Tuesday’s lows, then I tip my hat to them!) Let’s take another example. $TPL is trading near an all-time high and is up almost 4x DKI’s initial purchase price. It was up on Monday. Of course it was: Oil was up so we’d expect an oil stock to go up. But $TPL was down on Tuesday. That also can be made to make sense. Higher oil prices affect the cost of memory chips made in Korea and the cost of running a datacenter. One exciting part of $TPL’s business model is the plan to put AI datacenters on its land and provide energy and water. Worse datacenter economics mean fewer builders of them will want to pay to be on $TPL’s land. See the point – no matter what happens, there’s an explanation that makes it all seem to make sense.

That’s a lot of vol for the safest of trades – but does the volatility matter?

DKI Takeaway: Here’s what I did with the portfolio: Nothing. That’s for two reasons. First, none of us know what’s actually happening on the ground and half of what we “see” is intended to deceive. Some are claiming the US is losing and that Iran has incredible unlaunched missile capacity (but no explanation for why they’re so reserved and haven’t launched them). Others are showing video of Tel Aviv in shambles…with video that’s from other locations in other years. It’s not clear who’s in charge in Iran, or if anyone is in charge. The building where the council that selects the next Supreme Leader was hit. I’ve seen reports that all 88 members were killed and there’s no one left to vote. I’ve seen other reports that everyone was meeting through remote video, and the building was empty. Do you know what really happened?

More importantly, oil prices rose when Iran threatened to close the Strait of Hormuz and insurance rates skyrocketed. With one social media post, President Trump announced the US would provide reasonably-priced insurance for oil tankers. How can President Trump underwrite this risk and not end up with massive insurance losses for the US and oil tankers at the bottom of the Strait? He’s said the US Navy will escort ships if necessary. That’s a level of insurance no insurance underwriter can match. The key point here is that with one social media post, the President changed the calculation for shipping oil through the lane that carries 20% of the world’s crude (and changed the market for the shipping insurance companies). Will this work or can Iran still stop traffic in the Strait? That’s unclear.

No post hoc analysis here. I don’t know what’s going to happen over the next month let alone the next 24 hours. I do like current DKI exposure featuring dollar alternatives like Bitcoin, gold, and silver, big energy positions in oil and nuclear, and a select number of high-growth stocks. I’m watching current events like all of you are, but don’t want to get whipsawed by trying to trade every intra-day move.

2) Oil Prices Surge on Conflict Disruptions:

Global markets were disrupted this week as crude oil spiked 8% Tuesday and further late in the week in the wake of escalation in Iran. The Islamic Regime claims the Strait of Hormuz is closed to tanker traffic. They threatened to fire on any (non-Chinese) vessel trying to cross. President Trump indicated on social media that the US Navy may provide escorts to oil tankers attempting to go through the area, though some have questions about the Navy’s capacity to do so. Iran also executed attacks on Saudi Arabia’s largest domestic refinery and a US Embassy in Riyadh. This escalation led to other counterattacks between the United States, Israel, and Iran, which sent worries of an extended conflict rippling through markets. Then on Thursday, reports came out that Iran attacked a US oil tanker, pushing prices up further to around $92/barrel on Friday, an increase of 27% in one week. (Different sources question whether the US tanker was hit.)

I’m showing $92 right now, but at some point, the hard-working interns needed to finish the graph! If Korea runs out, it’s going to be a problem.

DKI Takeaway: The Strait of Hormuz oversees the flow of around 20% of the world’s oil. Right now, the markets are pricing in temporary disruption, not an extended closure. This can turn into an emergency in Asia in a matter of days. The Korean stock market was down early in the week due to small reserve levels and the need for energy to keep some of the world’s best semiconductor manufacturers operating. DRAM shortages may get even worse. With US Navy intervention possible, escorts could keep supply going, but Middle Eastern supply tanks are filling fast. Right now, current traffic through the Strait is down over 80% with over 200 oil tankers stranded. Delays of just a few weeks would likely push crude prices above $100/barrel. There’s too much uncertainty about the future of the conflict to make clear judgements on what’s next. For now, the only thing we can expect with confidence is volatility in the markets.

3) OpenAI Receives $100B in Funding from Tech Powerhouse Trio:

Last Friday, OpenAI announced a $110B round of funding, more than doubling the size of last year’s raise, breaking the previous record for a private tech company. $50B came from Amazon, $30B from Nvidia, and another $30B from SoftBank. As part of the deal, the company announced plans to expand its partnerships with Amazon and Nvidia. The agreement with Amazon’s AWS will expand its role as the cloud provider for OpenAI’s new agentic AI service, Frontier. They also secured 3GW of inference capacity and 2 GW of training on Nvidia’s next-gen AI Vera Rubin compute system to help alleviate bottlenecks as demand/usage increases.

It’s a new record, but is it enough?

DKI Takeaway: OpenAI slashed the planned $1.4T in infrastructure commitments to $600B. By our calculations, OpenAI had to raise about $1.5T to meet its commitments. With the reduced commitment and the record capital raise, it still needs to raise another half-trillion dollars to fund planned purchases and operating losses. More importantly, other AI companies like Google and Amazon have profitable businesses to fund AI losses. OpenAI doesn’t. No one in the industry has a business model to earn a return on the now-trillions of dollars of AI and datacenter spending. Finally, the reduction in planned spending by $800B means almost a trillion dollars of reduced revenue for OpenAI’s partners. What happens to the multiple for these tech firms if they face reduced future revenue growth rates? (Note that we’re seeing reports of Nvidia funding datacenter builds for other companies. Are they buying their own revenue? More in next week’s 5 Things.)

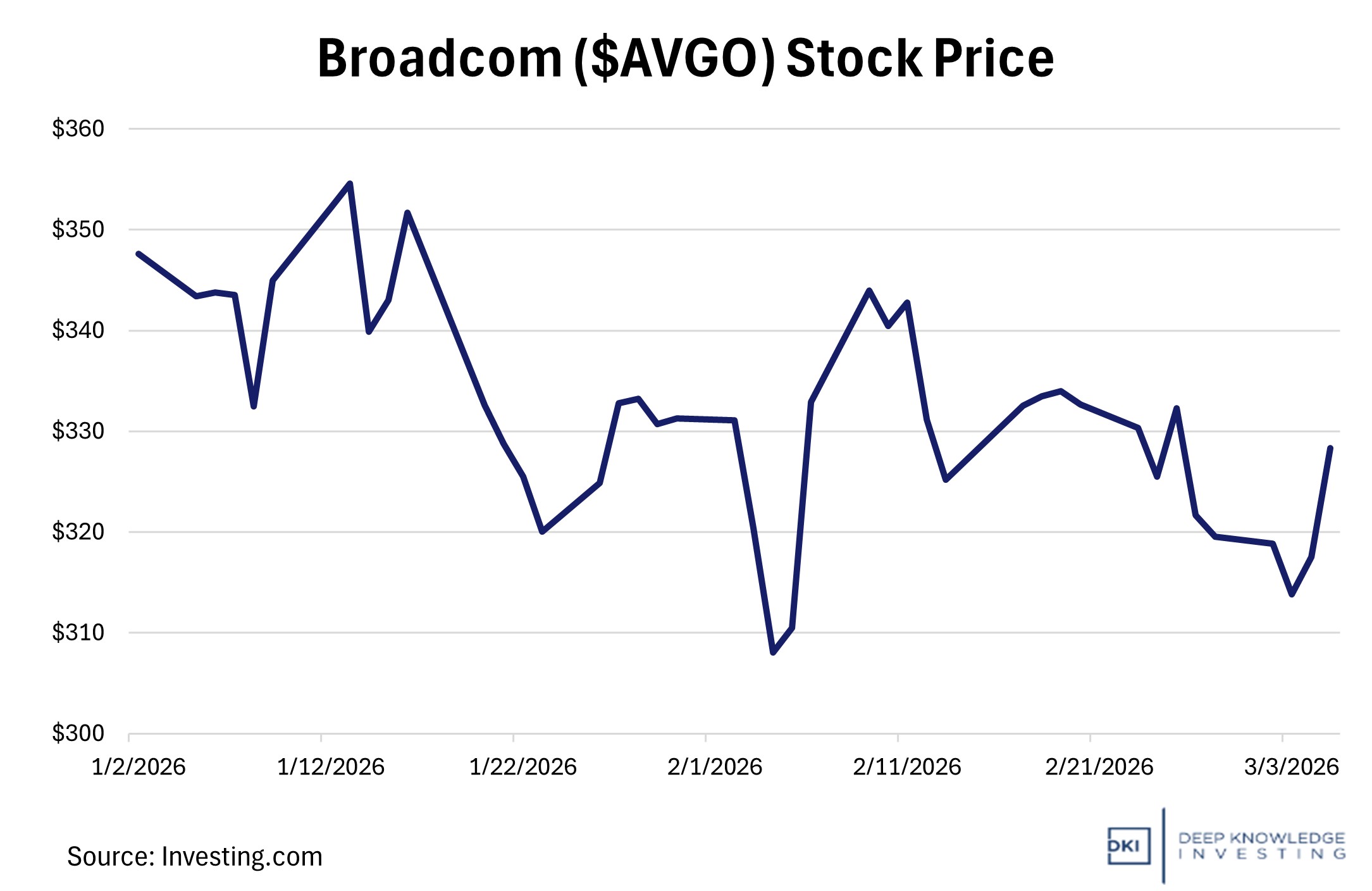

4) Broadcom Forecasts Soaring AI Chip Demand & Huge Orders from Anthropic:

Broadcom announced robust guidance, forecasting that its AI chip revenue will exceed $100 billion in 2027. This signals strong demand for custom-designed processors amid massive industry investment in data-center infrastructure. CEO, Hock Tan, highlighted orders from major cloud and AI firms, including Alphabet, Microsoft, Amazon, Meta, and Anthropic, as the company moves closer to the scale of volume deals associated with Nvidia and AMD. Broadcom expects to deliver 1GW of TPUs (Tensor Processing Units) to Anthropic in 2026, rising to 3GW in 2027. These chips support training and inference workloads reinforcing its role as a key supplier of custom AI accelerators and networking silicon. The company also announced a new $10B share repurchase program and revenue guidance above analyst estimates.

The market liked the guidance, but not enough to make a multi-month high.

DKI Takeaway: Broadcom’s growth validates the idea that the AI ecosystem increasingly favors custom silicon at the expense of traditional GPU suppliers and broadens the competitive landscape in a market dominated by Nvidia. However, the reliance on huge multi-year commitments carries risk. Actual deployment, margins, and execution will determine whether these projections turn into profitable projects, or just reflect backlog optimism. Companies that can deliver sustained supply, design expertise, and integration stand to benefit as AI workloads scale.

5) Educational Topic: Explaining Operating Leverage:

Operating leverage refers to the degree to which a company’s cost structure is composed of fixed costs versus variable costs and how that structure affects operating profit when revenue changes. Companies with high operating leverage typically have a larger proportion of fixed costs like rent, salaries, or manufacturing equipment. Variable costs fluctuate directly with production or sales. Because these fixed costs remain largely constant regardless of output, additional revenue converts to profit in a disproportionately positive way.

When revenue grows, firms with high operating leverage experience faster growth in operating income because most of their incremental sales do not require additional costs. The best example of this would be a software company that incurs that cost of upfront development. However, once the platform is built, additional sales have little cost.

With growing revenue, high fixed cost is better. With shrinking revenue, high variable cost is better.

DKI Takeaway: Operating leverage works in both directions. If revenue declines, companies with high fixed costs cannot easily reduce those expenses. This means that a relatively small decline in sales would lead to a large decline in operating income. Industries with significant capital investment, like manufacturing or airlines, often exhibit this characteristic. During economic downturn, these firms may see margins compress rapidly because fixed costs remain constant when revenue falls.

Information contained in this report is believed by Deep Knowledge Investing (“DKI”) to be accurate and/or derived from sources which it believes to be reliable; however, such information is presented without warranty of any kind, whether express or implied and DKI makes no representation as to the completeness, timeliness or accuracy of the information contained therein or with regard to the results to be obtained from its use. The provision of the information contained in the Services shall not be deemed to obligate DKI to provide updated or similar information in the future except to the extent it may be required to do so.

The information we provide is publicly available; our reports are neither an offer nor a solicitation to buy or sell securities. All expressions of opinion are precisely that and are subject to change. DKI, affiliates of DKI or its principal or others associated with DKI may have, take or sell positions in securities of companies about which we write.

Our opinions are not advice that investment in a company’s securities is suitable for any particular investor. Each investor should consult with and rely on his or its own investigation, due diligence and the recommendations of investment professionals whom the investor has engaged for that purpose.

In no event shall DKI be liable for any costs, liabilities, losses, expenses (including, but not limited to, attorneys’ fees), damages of any kind, including direct, indirect, punitive, incidental, special or consequential damages, or for any trading losses arising from or attributable to the use of this report.